14. The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month. Bodie, Z., Kane, A. & Marcus, A.J. (2013). Investments (10th ed.). © McGraw-Hill Education Page 1 of 5 Beta R-square Standard Deviation of Residuals .75 .65 .06 (i.e., 6% monthly) a. If he holds a $2 million portfolio of Waterworks stock, and wishes to hedge market exposure for the next month using 1-month maturity S&P 500 futures contracts, how many contracts should he enter? Should he buy or sell contracts? The S&P 500 currently is at 1,000 and the contract multiplier is $250. b. What is the standard deviation of the monthly return of the hedged portfolio? c. Assuming that monthly returns are approximately normally distributed, what is the probability that this market-neutral strategy will lose money over the next month? Assume the risk-free rate is .5% per month.

14. The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month. Bodie, Z., Kane, A. & Marcus, A.J. (2013). Investments (10th ed.). © McGraw-Hill Education Page 1 of 5 Beta R-square Standard Deviation of Residuals .75 .65 .06 (i.e., 6% monthly) a. If he holds a $2 million portfolio of Waterworks stock, and wishes to hedge market exposure for the next month using 1-month maturity S&P 500 futures contracts, how many contracts should he enter? Should he buy or sell contracts? The S&P 500 currently is at 1,000 and the contract multiplier is $250. b. What is the standard deviation of the monthly return of the hedged portfolio? c. Assuming that monthly returns are approximately normally distributed, what is the probability that this market-neutral strategy will lose money over the next month? Assume the risk-free rate is .5% per month.

Chapter8: Risk And Rates Of Return

Section: Chapter Questions

Problem 18PROB

Related questions

Question

Please assist with Question 14 a - c

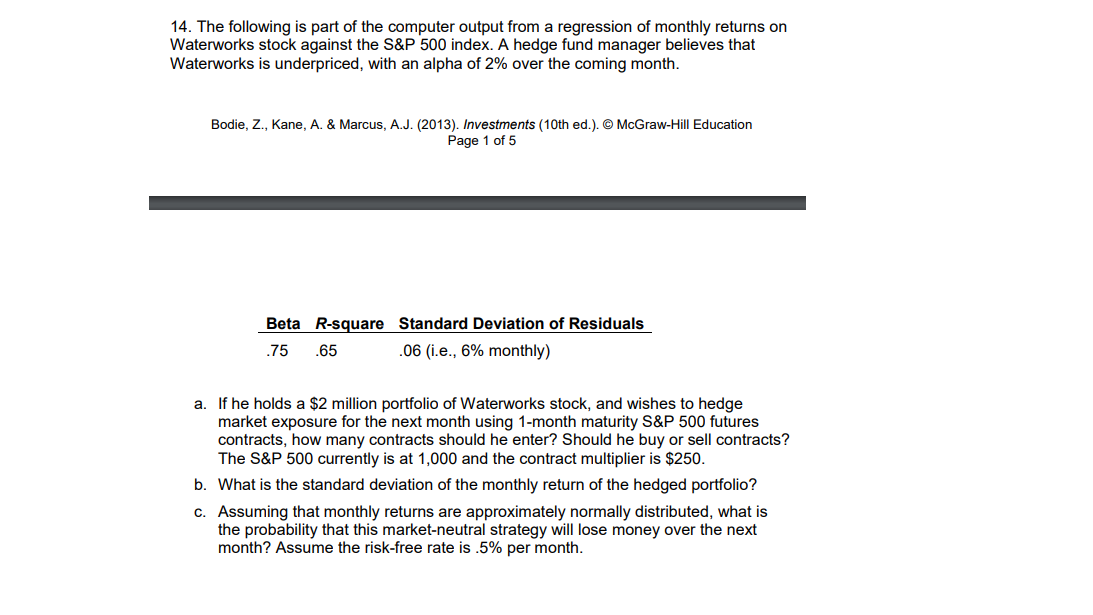

Transcribed Image Text:14. The following is part of the computer output from a regression of monthly returns on

Waterworks stock against the S&P 500 index. A hedge fund manager believes that

Waterworks is underpriced, with an alpha of 2% over the coming month.

Bodie, Z., Kane, A. & Marcus, A.J. (2013). Investments (10th ed.). © McGraw-Hill Education

Page 1 of 5

Beta R-square Standard Deviation of Residuals

.75 .65

.06 (i.e., 6% monthly)

a. If he holds a $2 million portfolio of Waterworks stock, and wishes to hedge

market exposure for the next month using 1-month maturity S&P 500 futures

contracts, how many contracts should he enter? Should he buy or sell contracts?

The S&P 500 currently is at 1,000 and the contract multiplier is $250.

b. What is the standard deviation of the monthly return of the hedged portfolio?

c. Assuming that monthly returns are approximately normally distributed, what is

the probability that this market-neutral strategy will lose money over the next

month? Assume the risk-free rate is .5% per month.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT