5. You are evaluating the performance of two portfolio managers, and you have gathered annual return data for the past decade: Manager X Return (%) Manager Y Return (%) Year -6.5 -1.5 -1.5 -3.5 -1.5 3 -1.5 4 -1.0 3.5 0.0 4.5 4.5 6.5 6.5 7.5 8.5 8.5 13.5 12.5 10 17.5 13.5 a. For each manager, calculate (1) the average annual return, (2) the standard deviation of returns, and (3) the semi-deviation of returns. b. Assuming that the average annual risk-free rate during the 10-year sample period was 1.5 percent, calculate the Sharpe ratio for each portfolio. Based on these computations, which manager appears to have performed the best? c. Calculate the Sortino ratio for each portfolio, using the average risk-free rate as the minimum acceptable return threshold. Based on these computations, which manager appears to have performed the best? d. When would you expect the Sharpe and Sortino measures to provide (1) the same per- formance ranking or (2) different performance rankings? Explain.

5. You are evaluating the performance of two portfolio managers, and you have gathered annual return data for the past decade: Manager X Return (%) Manager Y Return (%) Year -6.5 -1.5 -1.5 -3.5 -1.5 3 -1.5 4 -1.0 3.5 0.0 4.5 4.5 6.5 6.5 7.5 8.5 8.5 13.5 12.5 10 17.5 13.5 a. For each manager, calculate (1) the average annual return, (2) the standard deviation of returns, and (3) the semi-deviation of returns. b. Assuming that the average annual risk-free rate during the 10-year sample period was 1.5 percent, calculate the Sharpe ratio for each portfolio. Based on these computations, which manager appears to have performed the best? c. Calculate the Sortino ratio for each portfolio, using the average risk-free rate as the minimum acceptable return threshold. Based on these computations, which manager appears to have performed the best? d. When would you expect the Sharpe and Sortino measures to provide (1) the same per- formance ranking or (2) different performance rankings? Explain.

Essentials of Business Analytics (MindTap Course List)

2nd Edition

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Chapter15: Decision Analysis

Section: Chapter Questions

Problem 4P: Investment advisors estimated the stock market returns for four market segments: computers,...

Related questions

Question

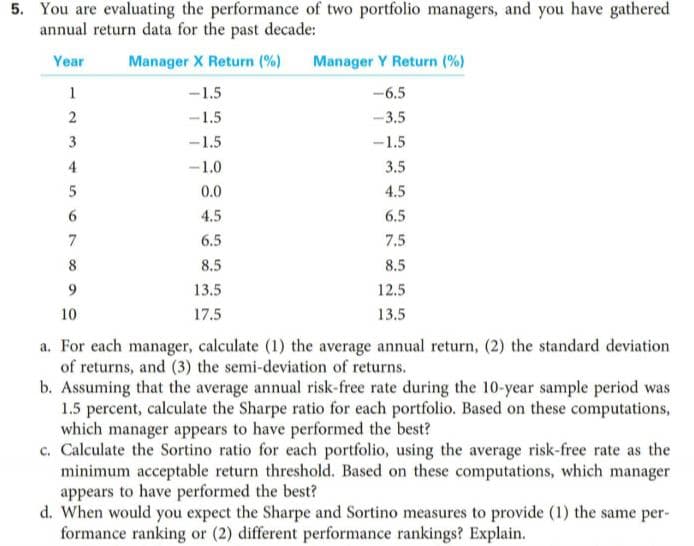

Transcribed Image Text:5. You are evaluating the performance of two portfolio managers, and you have gathered

annual return data for the past decade:

Manager X Return (%)

Manager Y Return (%)

Year

-6.5

-1.5

-1.5

-3.5

-1.5

3

-1.5

4

-1.0

3.5

0.0

4.5

4.5

6.5

6.5

7.5

8.5

8.5

13.5

12.5

10

17.5

13.5

a. For each manager, calculate (1) the average annual return, (2) the standard deviation

of returns, and (3) the semi-deviation of returns.

b. Assuming that the average annual risk-free rate during the 10-year sample period was

1.5 percent, calculate the Sharpe ratio for each portfolio. Based on these computations,

which manager appears to have performed the best?

c. Calculate the Sortino ratio for each portfolio, using the average risk-free rate as the

minimum acceptable return threshold. Based on these computations, which manager

appears to have performed the best?

d. When would you expect the Sharpe and Sortino measures to provide (1) the same per-

formance ranking or (2) different performance rankings? Explain.

Expert Solution

Trending now

This is a popular solution!

Step by step

Solved in 9 steps with 7 images

Recommended textbooks for you

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning