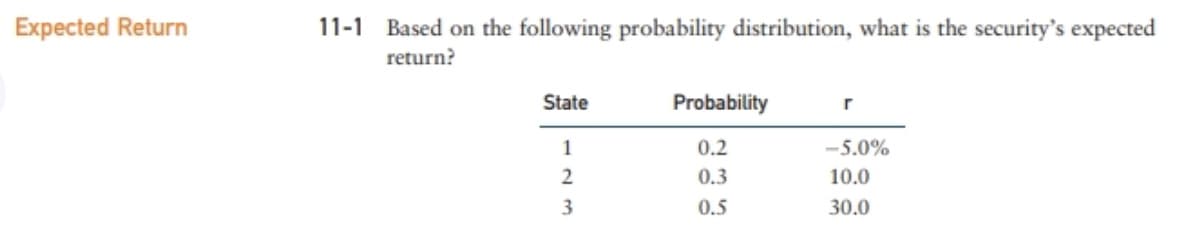

Based on the following probability distribution, what is the security's expected Expected Return 11-1 return? Probability State -5.0% 0.2 0.3 10.0 3 30.0 0.5

Q: Using the following data: Scenario Probability return K1 return K2 0.2 -10% 5% W2 0.4 0% 30% W3 0.4…

A: Excel Spreadsheet: Excel Workings:

Q: An investment has a 20% chance of producing a 25% return, a 60%chance of producing a 10% return, and…

A: Computation:

Q: Expected Return 11-1 Based on the following probability distribution, what is the security's…

A: Expected Return is the return which an investor expect to be earned from the investment made in…

Q: 1. A security has an expected rate of return of 0.11 and has a beta (B) of 1.5. The risk-free rate…

A: 1) Expected return = 11% Beta = 1.5 Risk free rate (Rf) = 5% Market return (Rm) = 9%

Q: The risk-free rate is 4%, and the expected rate of return on the market portfolio is 9%. Calculate…

A: In the given problem we require to calculate the required rate of return on a security from the…

Q: 4. Given the probability and returns associated with each state, what is the expected return? What…

A: Calculations of expected return and standard deviation: Excel workings:

Q: Based on the following probability distribution, what is the security’s expected return? State…

A: Calculate the expected return as follows: Expected return = Sum of product of (Probability *…

Q: Based on the following table, compute the reward-to-risk ratio for security Pearl if the risk-free…

A: Security Beta Expected return Pearl 0.9 17% Emerald 1.2 17%

Q: Asset A has an expected return of 22.8% and a beta of 1.8. The expected market return is 14%. What…

A: The risk free rate can be calculated as per the capital asset pricing model.

Q: Suppose a security follows a geometric Brownian motion with interest rate r=0.01, volatility…

A: The formula I have for simlating the prices have mu and sigma, but no r (Interest rate). Please…

Q: An investment has the following possible returns: Return: 13%; Probability: 40% Return: 8%;…

A: The expected return is the minimum required rate of return which an investor required from the…

Q: What is the Variance of returns for Security XYZ? (no rounding off until the final answer, final…

A: Information OUTCOME PROBABILITY EXPECTED RETURN A 20% 20% B 80% 25%

Q: Calculate the coefficient of variation for each security Explain why the standard deviation and…

A: Coefficient of variation of Security A: Standard deviation/ Mean(or Expected return ) = 0.20 /…

Q: Electric fund had expected return of 15% and standard deviation for this return is 26%. Beta and…

A: Expected return (Re) = 15% Risk free rate (Rf) = 4% Standard deviation (SD) = 26%

Q: The Manhawkin Fund has an expected return of 17% and a standard deviation return of 33%. The risk…

A: Sharpe ratio is one of the financial metric which is used to analyze the performance of various…

Q: Security A has an expected rate of return of 0.10 and a beta of 1.3. The market expected rate of…

A: Given details are : Expected rate of return of security A = 0.10 Beta = 1.3 Expected market return =…

Q: If the market portfolio has a required return of 0.12 and a standard deviation of 0.40, and the…

A: Security market line (SML): The security market line (SML) is the graphic depiction of the Capital…

Q: Assume the risk free rate is 3.9% and the expected return on the market is 13%. Based on the CAPM,…

A: Given details are : Risk free rate (Rf) = 3.9% Expected market return (Rm) = 13% Beta = 1.25 From…

Q: Based on the following probability distribution, what is the security's expected return? State…

A: Formula: Expected return = Specific probability * Specific return or pay off

Q: "A security with normally distributed returns has an annual expected return of 15% and standard…

A: Given: Annual expected return μ=15% Population standard deviation σ=9%

Q: Suppose there are two stocks, one with expected return of 14% with a beta of 1 and the other with…

A: The expected rate of return is the return that an investor expects the company to generate out of…

Q: An optimal risk portfolio’s expected return is 14%, standard deviation is 22%. If risk-free rate is…

A: The tradeoff between the return and risk of the portfolio is measured by the slope of CAL(Capital…

Q: Given the following probability distributions, what are the expected returns for the Market and for…

A: State Pr i rM rJ 1 0.3 −10% 40% 2 0.4 10 −20 3 0.3 30 30

Q: The following numbers were randomly generated from a standard normal distribution: -0.25 0.3…

A: The formula for simulated price,S based on the initial closing price of S0 will be given by the…

Q: Suppose the market premium is 12%, market volatility is 20% and the risk-free rate is 6%. Suppose…

A: Expected return E(R) = rf + beta*Risk/market premium Where rf is risk free rate.

Q: Security A has the following probability distribution of returns: Scenario Probability Return 1]…

A: The variance of security is a measurement of the dispersion of returns from the average return of…

Q: 6-3. (Expected rate of return and risk) Louis Vuitton SE is evaluating a security. Calculate the…

A: 1 Expected Return = Σ (Return i x Probability i) Given Probability Return .2 7% .25 10%…

Q: Assume that the average variance of return for an individual security is 50 and that the average…

A: Average variance of individual security is 50 Average covariance is 10

Q: Using the table below, calculate the Sharpe ratio of a portfolio with 80% allocated to security A…

A: Sharpe ratio - is defined as the portfolio risk premium divided by the portfolio risk. Sharpe ratio…

Q: 3. Security A has the following probability distribution of returns: Scenario Probability Return 0.1…

A: Calculation: Formula snip:

Q: rate of return on security X with a beta of 1.25 is equal to:

A: The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and…

Q: You compute the optimal risky portfolio to have the expected return of 12% and standard deviation of…

A: Expected return E(r) = 12% Risk free rate (Rf) = 4% Standard Deviation (SD) = 20% Risk Aversion (A)…

Q: Given an optimal risky portfolio with expected return of 12%, standard deviation of 23%, and a risk…

A: An ideal portfolio is one that minimizes risk for a given level of return or maximizes return for a…

Q: Given the following probability distribution, compute for Outcome Probability Expected Return 20%…

A: As information expected return is as follows: Probability Return Expected return A B C=A*B…

Q: 4 A progect has 11:1. and the manket Risk pre mium is 6 0*, a beta of 1'03, the risk free nate is…

A: The beta coefficient shows the systematic risk of the assets. The beta factor shows the systematic…

Q: Stock A and B have the following probability distributions of expected future returns: Probability…

A: Answer: Expected rate of return for stock A is 15%. Standard deviation of stock B is 24%.

Q: Using 625 trading days of data, you estimated the daily log return follows a normal distribution…

A: “Hi, as per our policy we will answer the first three parts of the question. Kindly repost the…

Q: The risk-free rate is 10% and expected rate of return is 18%. The beta is 12 and standard deviation…

A: Sharpe ratio refers to the financial indicator of the performance of the fund (or security) in terms…

Q: and the market risk premium (kM - KRF) is 2%. OShow your solutions and explain your answe Expected…

A: In this we need to calculate the required rate of return and compare with expected return on stock.

Q: Suppose the market premium is 12%, market volatility is 20% and the risk-free rate is 6%. Suppose a…

A: Market risk premium (Mp) = 0.12 or 12% Risk free rate (Rf) = 0.06 or 6% Beta (b) = 0.8 Expected…

Q: Expected return of the X security is 12% and its standard deviation is 20%. Expected return of the Y…

A: Given information : Return X security 12% Return Y security 15% Standard deviation X security…

Q: Given the following probability distribution of returns: Probability Return 0.1 -15.0%…

A: Probability Return 0.1 -15.00% 0.25 0.00% 0.3 8.50% 0.25 12.00% 0.1 32.00%

Q: If the risk-free rate is 7.0%, the market risk premium is 11.0%, and the expected return on Security…

A: Beta is the value used to denote riskiness of a security with the market level of returns. It is…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images

- Security A has an expected return of 7%, a standard deviation of returns of 35%, a correlation coefficient with the market of −0.3, and a beta coefficient of −1.5. Security B has an expected return of 12%, a standard deviation of returns of 10%, a correlation with the market of 0.7, and a beta coefficient of 1.0. Which security is riskier? Why?Based on the following probability distribution, what is the security’s expected return? State Probability r 1 0.2 –5.0% 2 0.4 10.0 3 0.4 30.0Given the following probability distributions, what are the expected returns for the Market and for Security J? Statei Pr i rM rJ 1 0.3 −10% 40% 2 0.4 10 −20 3 0.3 30 30 Group of answer choices 10.0%; 11.3% 9.5%; 13.0% 10.0%; 9.5% 10.0%; 13.0% 13.0%; 10.0%

- Given the following probability distributions, what are the expected returns for the Market and for Security J? Statei Pr i rM rJ 1 0.3 −10% 40% 2 0.4 10 −20 3 0.3 30 30Security A has the following probability distribution of returns:Scenario Probability Return1] 0.1 15%2] 0.8 25%3] 0.1 35%What is the variance for Security A?A 0.002B 0.020C 0.200D 0.300Given the following probability distribution, what is the standard deviation of returns for Security J? (Expresss your answer in percentage, but do not include the percent sign, %, i.e., 4.65) State Pi rJ 1 0.2 6 % 2 0.6 11 3 0.2 17

- Based on the following table, compute the reward-to-risk ratio for security Pearl if the risk-free rate is 5%. Security Beta Expected Return (%) Pearl 0.9 17 Emerald 1.2 20What is the Variance of returns for Security XYZ? (no rounding off until the final answer, final answer at 5 decimal places “X.XXXXX”) the following probability distribution for security XYZ is determined: OUTCOME PROBABILITY EXPECTED RETURN A 20% 20% B 80% 25%Expected return of the X security is 12% and its standard deviation is 20%. Expected return of the Y security is 15% and its standard deviation is 27%. If, the correlation coefficient of the two securities is 0.7; then, what is the covariance between these two securities? A) 0.038B) 0.070C) 0.018D) 0.013E) 0.054

- Given the following probability distribution of returns: Probability Return 0.1 -15.0% 0.25 0.0% 0.3 8.5% 0.25 12.0% 0.1 32.0% what is the expected return?Which of the two securities are the best? By using probability estimates, below is the computation of ff. statistics: Statistic Security A Security B Expected return Standard deviation 12% 20% 8% 10% Requirement Calculate the coefficient of variation for each security Explain why the standard deviation and coefficient of variation give different ranking of risk. Which method is superior and why?Security X has expected return of 14% and standard deviation of 22%. Security Y has expected return of 16% and standard deviation of 28%. If the two securities have a correlation coefficient of 0.8, what is their covariance? 0.049 0.038 0.018 0.013