Case 12-7 Accounting for Income Taxes: Different Approaches Mark or Make is a bourbon distillery. Sales have been steady for the past three years, and operating costs have remained unchanged. On January 1, 2019, Mark or Make took advantage of a special deal to prepay its rent for three years at a substantial savings. The amount of the prepayment was $60,000. The income statement items (excluding the rent) are shown here. 2019 2020 2021 Gross profit on sales 350,000 349,000 351,000 Operating expense 210,000 210,000 210,000 Assume that the rental is deducted on the corporate tax purposes in 2019 and that there are no other temporary differences between taxable income and pretax accounting income. In addition, there are no permanent differences between taxable income and pretax accounting income. The corporate tax rate for all three years is 30%. Required: a. Construct income statements for 2019, 2020, and 2021 under the following approaches to interperiod income tax allocation: i. No allocation ii. Comprehensive allocation b. Do you believe that no allocation distorts Mark or Make's net income? Explain. c. For years 2019 and 2020, Mark or Make reported net income applying the concept of comprehensive interperiod income tax allocation. During 2020, Congress passed a new tax law that will increase the corporate tax rate from 30 to 33%. Reconstruct the income statements for 2020 and 2019 under the following assumptions: i. Mark or Make uses the deferred method to account for interperiod income tax allocation. ii. Mark or Make uses the asset-liability approach to account for interperiod income tax allocation.

Case 12-7 Accounting for Income Taxes: Different Approaches Mark or Make is a bourbon distillery. Sales have been steady for the past three years, and operating costs have remained unchanged. On January 1, 2019, Mark or Make took advantage of a special deal to prepay its rent for three years at a substantial savings. The amount of the prepayment was $60,000. The income statement items (excluding the rent) are shown here. 2019 2020 2021 Gross profit on sales 350,000 349,000 351,000 Operating expense 210,000 210,000 210,000 Assume that the rental is deducted on the corporate tax purposes in 2019 and that there are no other temporary differences between taxable income and pretax accounting income. In addition, there are no permanent differences between taxable income and pretax accounting income. The corporate tax rate for all three years is 30%. Required: a. Construct income statements for 2019, 2020, and 2021 under the following approaches to interperiod income tax allocation: i. No allocation ii. Comprehensive allocation b. Do you believe that no allocation distorts Mark or Make's net income? Explain. c. For years 2019 and 2020, Mark or Make reported net income applying the concept of comprehensive interperiod income tax allocation. During 2020, Congress passed a new tax law that will increase the corporate tax rate from 30 to 33%. Reconstruct the income statements for 2020 and 2019 under the following assumptions: i. Mark or Make uses the deferred method to account for interperiod income tax allocation. ii. Mark or Make uses the asset-liability approach to account for interperiod income tax allocation.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter9: Current Liabilities And Contingent Obligations

Section: Chapter Questions

Problem 10P: Bonus Obligation and Income Tax Expense James Kimberley, president of National Motors, receives a...

Related questions

Question

Answer only C.thanks in advance

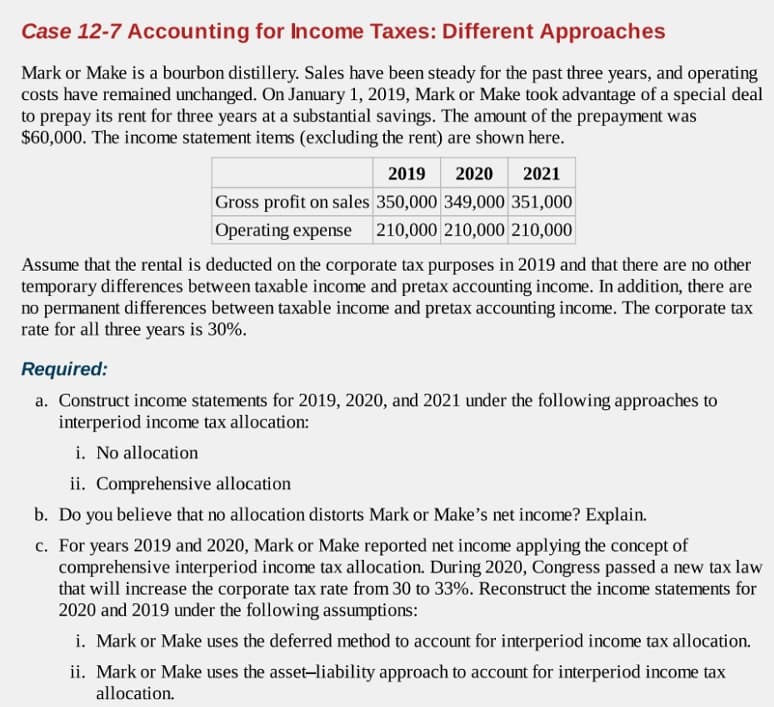

Transcribed Image Text:Case 12-7 Accounting for Income Taxes: Different Approaches

Mark or Make is a bourbon distillery. Sales have been steady for the past three years, and operating

costs have remained unchanged. On January 1, 2019, Mark or Make took advantage of a special deal

to prepay its rent for three years at a substantial savings. The amount of the prepayment was

$60,000. The income statement items (excluding the rent) are shown here.

2019

2020

2021

Gross profit on sales 350,000 349,000 351,000

Operating expense 210,000 210,000 210,000

Assume that the rental is deducted on the corporate tax purposes in 2019 and that there are no other

temporary differences between taxable income and pretax accounting income. In addition, there are

no permanent differences between taxable income and pretax accounting income. The corporate tax

rate for all three years is 30%.

Required:

a. Construct income statements for 2019, 2020, and 2021 under the following approaches to

interperiod income tax allocation:

i. No allocation

ii. Comprehensive allocation

b. Do you believe that no allocation distorts Mark or Make’s net income? Explain.

c. For years 2019 and 2020, Mark or Make reported net income applying the concept of

comprehensive interperiod income tax allocation. During 2020, Congress passed a new tax law

that will increase the corporate tax rate from 30 to 33%. Reconstruct the income statements for

2020 and 2019 under the following assumptions:

i. Mark or Make uses the deferred method to account for interperiod income tax allocation.

ii. Mark or Make uses the asset-liability approach to account for interperiod income tax

allocation.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning