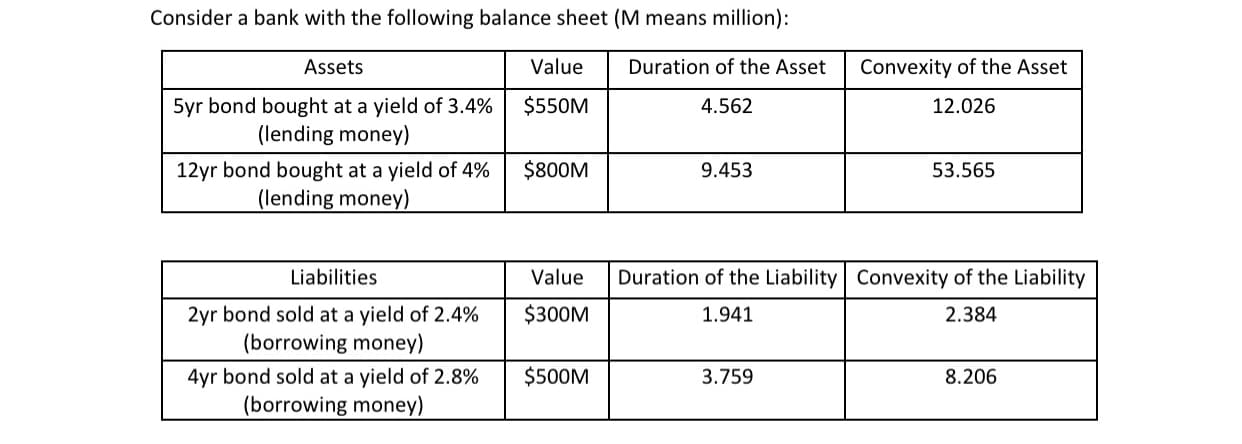

Consider a bank with the following balance sheet (M means million): Assets Value Duration of the Asset Convexity of the Asset $550M 5yr bond bought at a yield of 3.4% (lending money) 4.562 12.026 12yr bond bought at a yield of 4% $800M 9.453 53.565 (lending money) Liabilities Value Duration of the Liability Convexity of the Liability $300M 2yr bond sold at a yield of 2.4% (borrowing money) 1.941 2.384 $500M 4yr bond sold at a yield of 2.8% (borrowing money) 3.759 8.206

Consider a bank with the following balance sheet (M means million): Assets Value Duration of the Asset Convexity of the Asset $550M 5yr bond bought at a yield of 3.4% (lending money) 4.562 12.026 12yr bond bought at a yield of 4% $800M 9.453 53.565 (lending money) Liabilities Value Duration of the Liability Convexity of the Liability $300M 2yr bond sold at a yield of 2.4% (borrowing money) 1.941 2.384 $500M 4yr bond sold at a yield of 2.8% (borrowing money) 3.759 8.206

Chapter3: Evaluation Of Financial Performance

Section: Chapter Questions

Problem 8P

Related questions

Question

If the interest rates go up by 1%, using the duration and convexity rule to determine the net worth of the bank and the equity to asset ratio

Transcribed Image Text:Consider a bank with the following balance sheet (M means million):

Assets

Value

Duration of the Asset

Convexity of the Asset

$550M

5yr bond bought at a yield of 3.4%

(lending money)

4.562

12.026

12yr bond bought at a yield of 4%

$800M

9.453

53.565

(lending money)

Liabilities

Value

Duration of the Liability Convexity of the Liability

$300M

2yr bond sold at a yield of 2.4%

(borrowing money)

1.941

2.384

$500M

4yr bond sold at a yield of 2.8%

(borrowing money)

3.759

8.206

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT