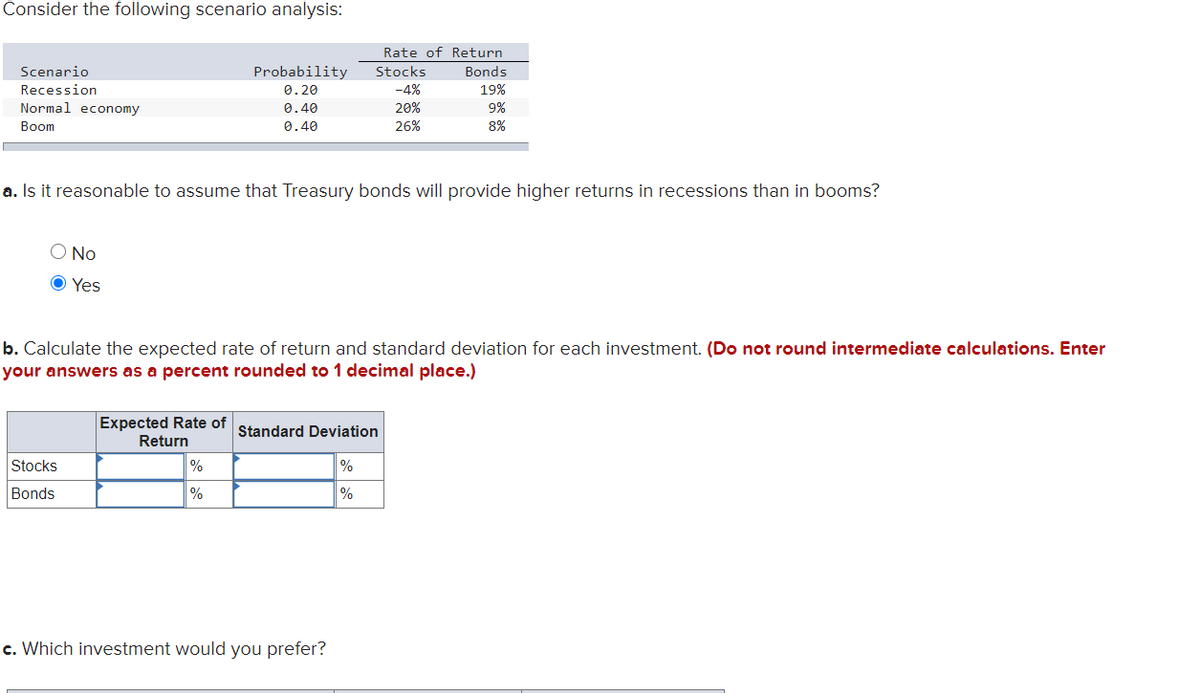

Consider the following scenario analysis: Rate of Return Bonds 19% 9% Scenario Probability Stocks Recession 0.20 -4% Normal economy 0.40 20% Boom 0.40 26% 8% a. Is it reasonable to assume that Treasury bonds will provide higher returns in recessions than in booms? O No O Yes b. Calculate the expected rate of return and standard deviation for each investment. (Do not round intermediate calculations. Enter your answers as a percent rounded to 1 decimal place.)

Risk and return

Before understanding the concept of Risk and Return in Financial Management, understanding the two-concept Risk and return individually is necessary.

Capital Asset Pricing Model

Capital asset pricing model, also known as CAPM, shows the relationship between the expected return of the investment and the market at risk. This concept is basically used particularly in the case of stocks or shares. It is also used across finance for pricing assets that have higher risk identity and for evaluating the expected returns for the assets given the risk of those assets and also the cost of capital.

expected rate of return for stocks = 0.20 * (-0.04) +0.40 *(0.20) +0.40 * (0.26)

= -0.008 +0.08 +0.104

= 0.176

= 17.6%

expected rate of return for bonds = 0.20 *(0.19) +0.40 * (0.09) +0.40 * (0.08)

= 0.038 +0.036 +0.032

= 0.106

= 10.6%

Trending now

This is a popular solution!

Step by step

Solved in 2 steps