Cordova manufactures three types of stained glass window, cleverly named Products A, B, and C. Information about these products follows: Product A Product B Product C Sales price Variable costs per unit Fixed costs per unit Required number of labor hours $39.00 $49.00 $79.00 20.75 21.00 40.75 7.00 7.00 7.00 1.25 2.00 2.50 Cordova currently is limited to 45,000 labor hours per month Required: Assuming an infinite demand for each of Cordova's products, determine contribution margin per direct labor hour. (Round your answers to 2 decimal places.) Contribution Margin Product A CM per DL hour Product B CM per DL hour Product C CM per DL hour

Cordova manufactures three types of stained glass window, cleverly named Products A, B, and C. Information about these products follows: Product A Product B Product C Sales price Variable costs per unit Fixed costs per unit Required number of labor hours $39.00 $49.00 $79.00 20.75 21.00 40.75 7.00 7.00 7.00 1.25 2.00 2.50 Cordova currently is limited to 45,000 labor hours per month Required: Assuming an infinite demand for each of Cordova's products, determine contribution margin per direct labor hour. (Round your answers to 2 decimal places.) Contribution Margin Product A CM per DL hour Product B CM per DL hour Product C CM per DL hour

Chapter6: Activity-based, Variable, And Absorption Costing

Section: Chapter Questions

Problem 9PB: Caseys Kitchens makes two types of food smokers: Gas and Electric. The company expects to...

Related questions

Question

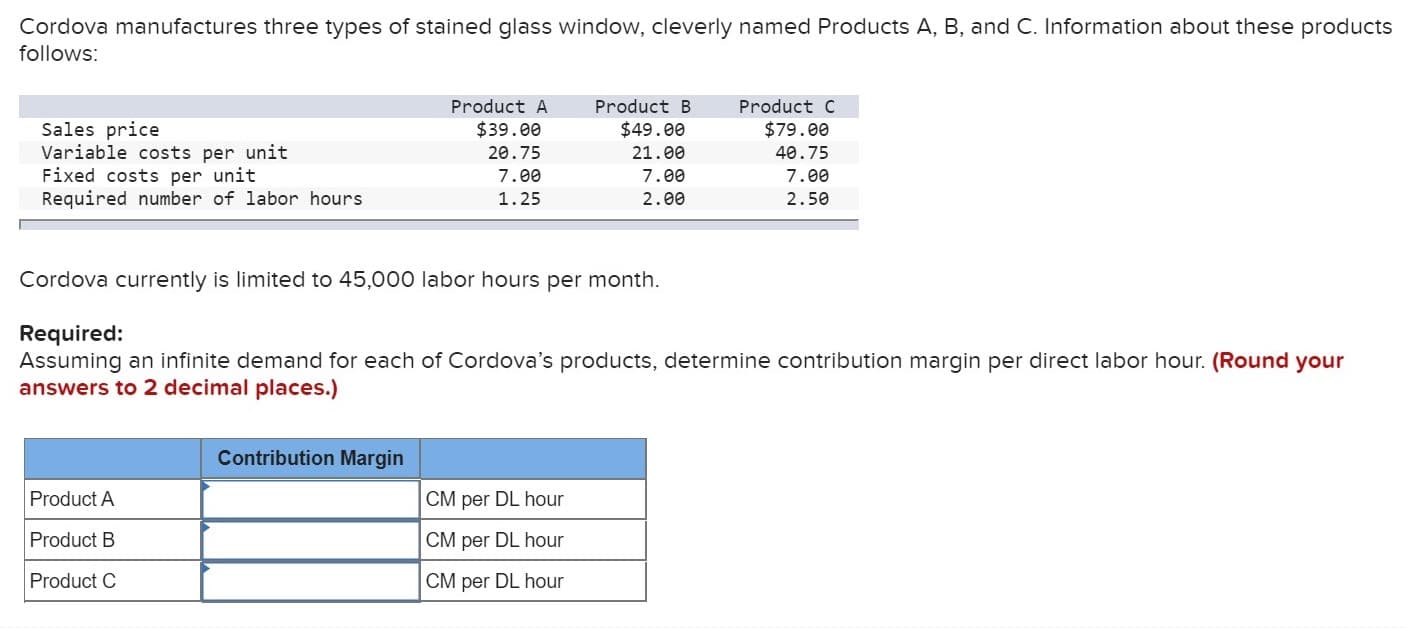

Transcribed Image Text:Cordova manufactures three types of stained glass window, cleverly named Products A, B, and C. Information about these products

follows:

Product A

Product B

Product C

Sales price

Variable costs per unit

Fixed costs per unit

Required number of labor hours

$39.00

$49.00

$79.00

20.75

21.00

40.75

7.00

7.00

7.00

1.25

2.00

2.50

Cordova currently is limited to 45,000 labor hours per month

Required:

Assuming an infinite demand for each of Cordova's products, determine contribution margin per direct labor hour. (Round your

answers to 2 decimal places.)

Contribution Margin

Product A

CM per DL hour

Product B

CM per DL hour

Product C

CM per DL hour

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 4 images

Recommended textbooks for you

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Essentials of Business Analytics (MindTap Course …

Statistics

ISBN:

9781305627734

Author:

Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning