er reviewing Shulman's quantitative analysis of the November variences, prepare a memorandum addressed to Roper explainning the following: a. The casue of the revenue mix varience. b. The implication of the revenue mix varience. c. The cause of the revenue timing difference. d. The significance of the revenue timing difference. e. The primary cause of the unfavorable total expense varience. f. How the favorable food price variance was determined. g. The impact of the promotion timing difference on future revenues and expenses. h. Whether the course development varience has an unfavorable impact on the company.

Master Budget

A master budget can be defined as an estimation of the revenue earned or expenses incurred over a specified period of time in the future and it is generally prepared on a periodic basis which can be either monthly, quarterly, half-yearly, or annually. It helps a business, an organization, or even an individual to manage the money effectively. A budget also helps in monitoring the performance of the people in the organization and helps in better decision-making.

Sales Budget and Selling

A budget is a financial plan designed by an undertaking for a definite period in future which acts as a major contributor towards enhancing the financial success of the business undertaking. The budget generally takes into account both current and future income and expenses.

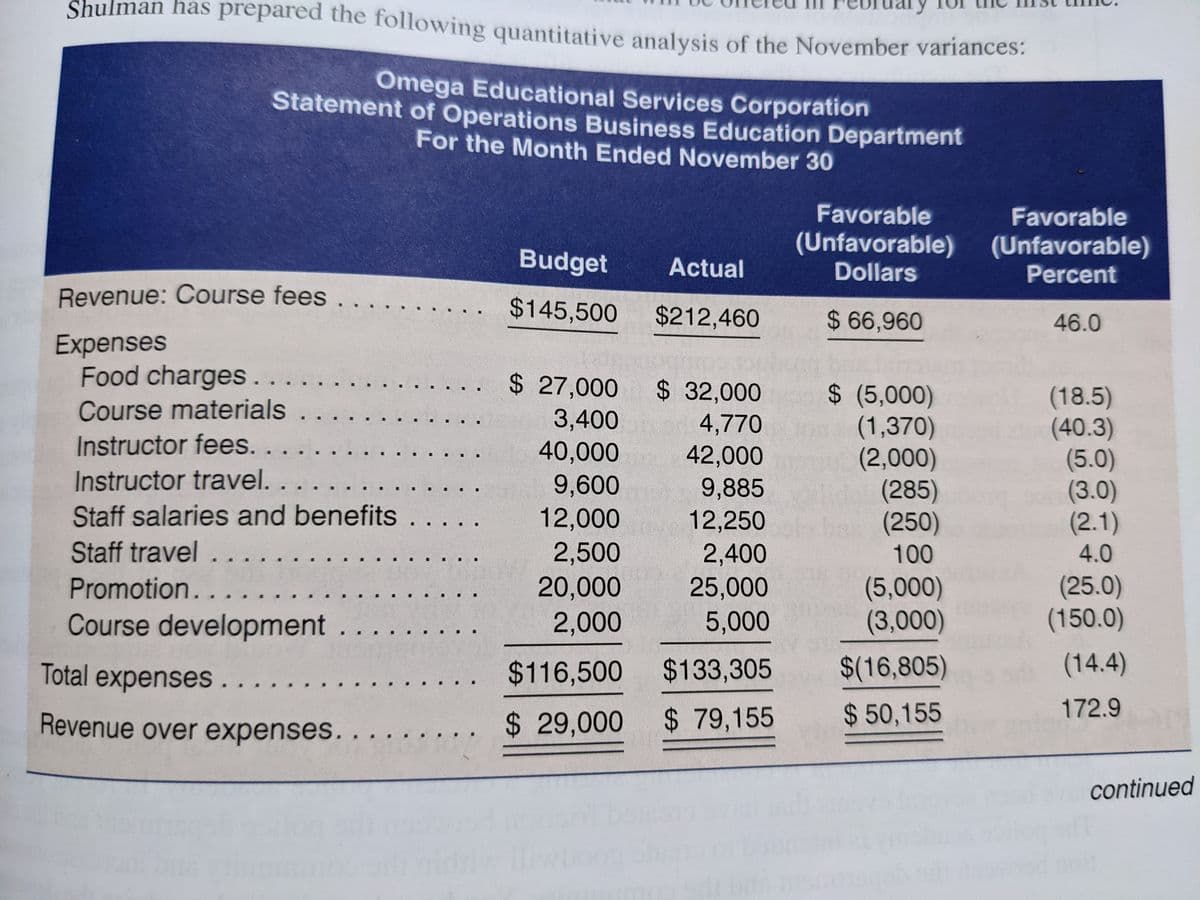

Comprehensive; analysis cost control The financial results for the Business Education Department of Omega Educational Services Corporation for November are presented in the schedule at the end of this problem. Caroline Roper, president of Omega Educational Services, is pleased with the final results but has observed that the revenue and most of the costs and expenses of this department exceeded the budgeted amounts. Bret Shulman, vice president of the Business Education Department, has been requested to provide an explanation for any amount that exceeded the budget by 5 percent or more.

Shulman has accumulated the following facts to assist in his analysis of the November results:

-The budget for the clalndar year was finalized in December of the preceding year, and at that time, a full program of business education courses was scheduled to be held in St. Louis during the first week of November. The schedule allowed eight courses to be run on each of the five days during the week. The budget assumed that there would be 425 participants in the program and 1,000 participant days for the week.

-Omega Educational Services charges a flat fee of $150 per day of course instruction, so the fee for a three-day course is $450. Omega grants a 10 percent discount to persons who subscribe to its publications. The 10 percent discount is also granted to second and subsequent registrants for the same course from the same organization. However, only one discount per registration is allowed.

Historically, 70 percent of the participant day registrations are at the full fee of $150 per day, and 30 percent of the participant day registrations recieved the discount fee of $135 per day. These percentages were used in developing the November budget revenue.

-The following estimates were used to develop the budgeted figures for course-related expenses:

Food charges per participant day (lunch/coffee breaks) = $27

Course materials per participant = $8

Instructor fee per day = $1,000

-A total of 530 individuals participated in the St. Louis courses in November, accounting for 1,280 participant days. This number included 20 persons who took a new, two-day course on pension accounting that was not on the original schedule; thus, on two days, nine courses were offered, and an additional instructor was hired to cover the new course. The breakdown of the course registrations follows.

Full fee registration = 704

Discounted fees

Current periodical subscribers = 128

New periodical subscribers = 128

Second registration from the same organization = 320

Total perticipant day registrations = 1,280

A combined promotional mailing was used to advertise St. Louis program and a program in Boston that was scheduled for December. The incremental costs of the combined promotion were $5,000, but none of the promotional expenses ($20,000) budgeted for the Boston program in December will have to be incurred. This earlier-than-normal promotion for the Boston program has resulted in early registration fees collected in November as follows (in terms of participant days):

Full fee registrations = 140

Discounted registrations = 60

Total perticipant day registrations = 200

-Omega Educational Services includes $2,000 in each monthly budget for the purpose of updating courses or adding new ones. The additional amount spent on course development during November was for an unscheduled course that will be offered in Fubruary for the first time.

Shulman has prepared the following quantitative analysis of the November variences: (See Attatchment)

After reviewing Shulman's quantitative analysis of the November variences, prepare a memorandum addressed to Roper explainning the following:

a. The casue of the revenue mix varience.

b. The implication of the revenue mix varience.

c. The cause of the revenue timing difference.

d. The significance of the revenue timing difference.

e. The primary cause of the unfavorable total expense varience.

f. How the favorable food price variance was determined.

g. The impact of the promotion timing difference on future revenues and expenses.

h. Whether the course development varience has an unfavorable impact on the company.

![continued from previous page

Omega Educational Services Corporation

Analysis of November Variances

$145,500

Budgeted revenue

Variances

Quantity variance [(1,280 - 1,000) x $145.50]. . . .

Mix variance [($143.25- $145.50) × 1,280]. . . .

Timing difference ($145.50 × 200) .

$40,740 F

2,880 U

29,100 F

66,960 F

Actual revenue..

$212,460

Budgeted expenses

Quantity variances

Food charges [(1,000 – 1,280) × $27] . . . .

Course materials [(425 – 530) × $8].

Instructor fees (2 x $1,000).

$116,500

$ 7,560 U

840 U

2,000 U

10,400 U

Price variances

Food charges [($27 – $25) × 1,280]. .

Course materials [($8 – $9) × 530].

$ 2,560 F

530 U

2,030 F

Timing differences

Promotion....

..... $ 5,000 U

Course development

3,000 U

8,000 U

Variances not analyzed (5% or less)

Instructor travel. ...

Staff salaries and benefits .

285 U

Staff travel..

250 U

100 F

435 U

Actual expenses..

$133,305

After reviewing Sbulman

%24](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2Fe050d04e-66d9-449d-927d-fb56c8a981a9%2F2eca1127-4f3a-4914-89af-c07640490621%2Fs63hyc_processed.jpeg&w=3840&q=75)

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images