From page 9-3 of the VLN, what are the cash flows from a bond that must be present valued back to today? Group of answer choices A. The face amount only B. The interest payments only C. The issue price only D. The face amount and interest payments

From page 9-3 of the VLN, what are the cash flows from a bond that must be present valued back to today? Group of answer choices A. The face amount only B. The interest payments only C. The issue price only D. The face amount and interest payments

Financial Accounting: The Impact on Decision Makers

10th Edition

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Gary A. Porter, Curtis L. Norton

Chapter10: Long-term Liabilities

Section: Chapter Questions

Problem 10.1KTQ

Related questions

Question

From page 9-3 of the VLN, what are the cash flows from a bond that must be present valued back to today?

Group of answer choices

A. The face amount only

B. The interest payments only

C. The issue price only

D. The face amount and interest payments

![Bonds can be issued (sold) for more or less than their face value.

Sells at Face Amount (100%):

Bond Premium (>100%):

Bond Discount (<100%):

Determining the Issue Price of a Bond

1. Identify the two cash flows provided by the bond (Face value-a single sum AND Interest

payments [face x stated rate or if semiannual then face x % stated rate]-an annuity).

2. Compare the market rate with the stated rate to determine if bond will sell at face, premium or

discount. If at face then no more calculations are needed.

3. Eliminate the stated rate, you don't need it anymore as you already know the cash flows from

the bond.

4. Use the market rate and compounding periods to determine the correct factor to present value

the cash flows.

Practice

ABC Corporation wants to issue five-year $1,000 bonds 10% stated rate paying semi-annual interest.

Market rate of interest is 8%; (therefore, semiannual would be 5% stated rate and 4% market rate

respectively). What is the bond issue price on January 1, 20XA?

Calculate the issue price of the bond:

CASH FLOW X PV FACTOR (use market rate) =

Present Value

Present Value of Principal (Face)

Present Value of Interest Payment

(Face x stated)

Issue price (sales price)

OR with the TI BAII Plus Calculator

PMT

СРТ PV

IY

FV

The issue price:

Calculate the difference:

Bond issue price

Bond face amount

Difference

Record the bond issuance on January 1, 20XA](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2Fc9d06b09-34b2-4a0b-b1fb-2ba46d6a9f5a%2Fd35f50fd-113d-4b04-89eb-93810df6a983%2Frl79wey_processed.jpeg&w=3840&q=75)

Transcribed Image Text:Bonds can be issued (sold) for more or less than their face value.

Sells at Face Amount (100%):

Bond Premium (>100%):

Bond Discount (<100%):

Determining the Issue Price of a Bond

1. Identify the two cash flows provided by the bond (Face value-a single sum AND Interest

payments [face x stated rate or if semiannual then face x % stated rate]-an annuity).

2. Compare the market rate with the stated rate to determine if bond will sell at face, premium or

discount. If at face then no more calculations are needed.

3. Eliminate the stated rate, you don't need it anymore as you already know the cash flows from

the bond.

4. Use the market rate and compounding periods to determine the correct factor to present value

the cash flows.

Practice

ABC Corporation wants to issue five-year $1,000 bonds 10% stated rate paying semi-annual interest.

Market rate of interest is 8%; (therefore, semiannual would be 5% stated rate and 4% market rate

respectively). What is the bond issue price on January 1, 20XA?

Calculate the issue price of the bond:

CASH FLOW X PV FACTOR (use market rate) =

Present Value

Present Value of Principal (Face)

Present Value of Interest Payment

(Face x stated)

Issue price (sales price)

OR with the TI BAII Plus Calculator

PMT

СРТ PV

IY

FV

The issue price:

Calculate the difference:

Bond issue price

Bond face amount

Difference

Record the bond issuance on January 1, 20XA

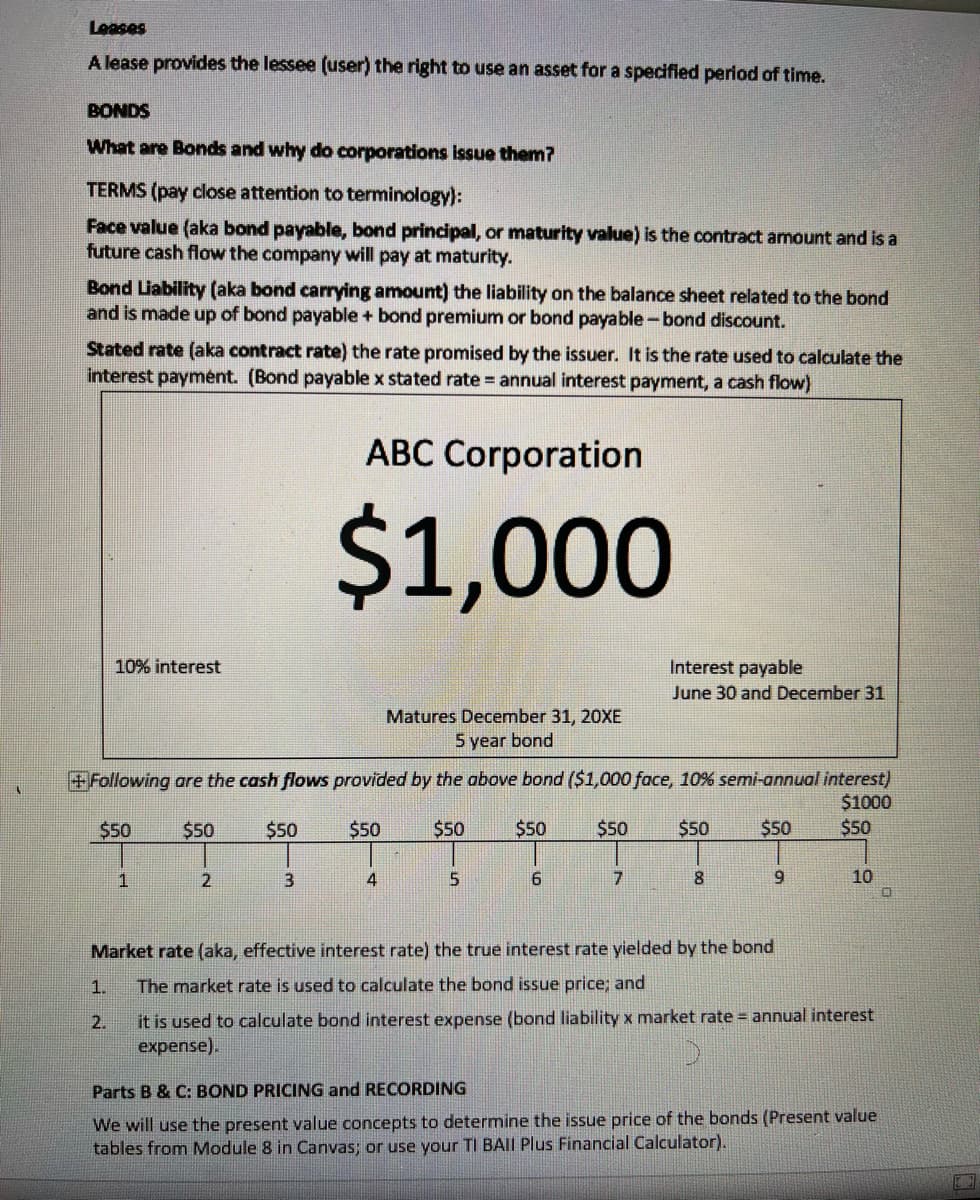

Transcribed Image Text:Leases

A lease provides the lessee (user) the right to use an asset for a specified period of time.

BONDS

What are Bonds and why do corporations issue them?

TERMS (pay close attention to terminology):

Face value (aka bond payable, bond principal, or maturity value) is the contract amount and is a

future cash flow the company will pay at maturity.

Bond Liability (aka bond carrying amount) the liability on the balance sheet related to the bond

and is made up of bond payable + bond premium or bond payable-bond discount.

Stated rate (aka contract rate) the rate promised by the issuer. It is the rate used to calculate the

interest paymént. (Bond payable x stated rate = annual interest payment, a cash flow)

ABC Corporation

$1,000

10% interest

Interest payable

June 30 and December 31

Matures December 31, 20XE

5 year bond

+Following are the cash flows provided by the above bond ($1,000 face, 10% semi-annual interest)

$1000

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

1

4

8.

9.

10

Market rate (aka, effective interest rate) the true interest rate yielded by the bond

1.

The market rate is used to calculate the bond issue price; and

it is used to calculate bond interest expense (bond liability x market rate annual interest

expense).

2.

Parts B & C: BOND PRICING and RECORDING

We will use the present value concepts to determine the issue price of the bonds (Present value

tables from Module 8 in Canvas; or use your TI BAII Plus Financial Calculator).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning