(g) Now assume that the market in which Dave's General Store operates is in long-run equilibrium. (i) Suppose the rent paid by Dave's General Store decreases. Will Dave's General Store's profit- maximizing quantity of Good X increase, decrease, or stay the same in the short run? Explain. (ii) Instead suppose Dave's General Store hires labor in a perfectly competitive market and the market wage increases. Will Dave's General Store's profit-maximizing quantity of Good X increase, decrease, or stay the same in the short run? Explain.

(g) Now assume that the market in which Dave's General Store operates is in long-run equilibrium. (i) Suppose the rent paid by Dave's General Store decreases. Will Dave's General Store's profit- maximizing quantity of Good X increase, decrease, or stay the same in the short run? Explain. (ii) Instead suppose Dave's General Store hires labor in a perfectly competitive market and the market wage increases. Will Dave's General Store's profit-maximizing quantity of Good X increase, decrease, or stay the same in the short run? Explain.

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

14th Edition

ISBN:9781305506381

Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Chapter11: Price And Output Determination: Monopoly And Dominant Firms

Section: Chapter Questions

Problem 6E

Related questions

Question

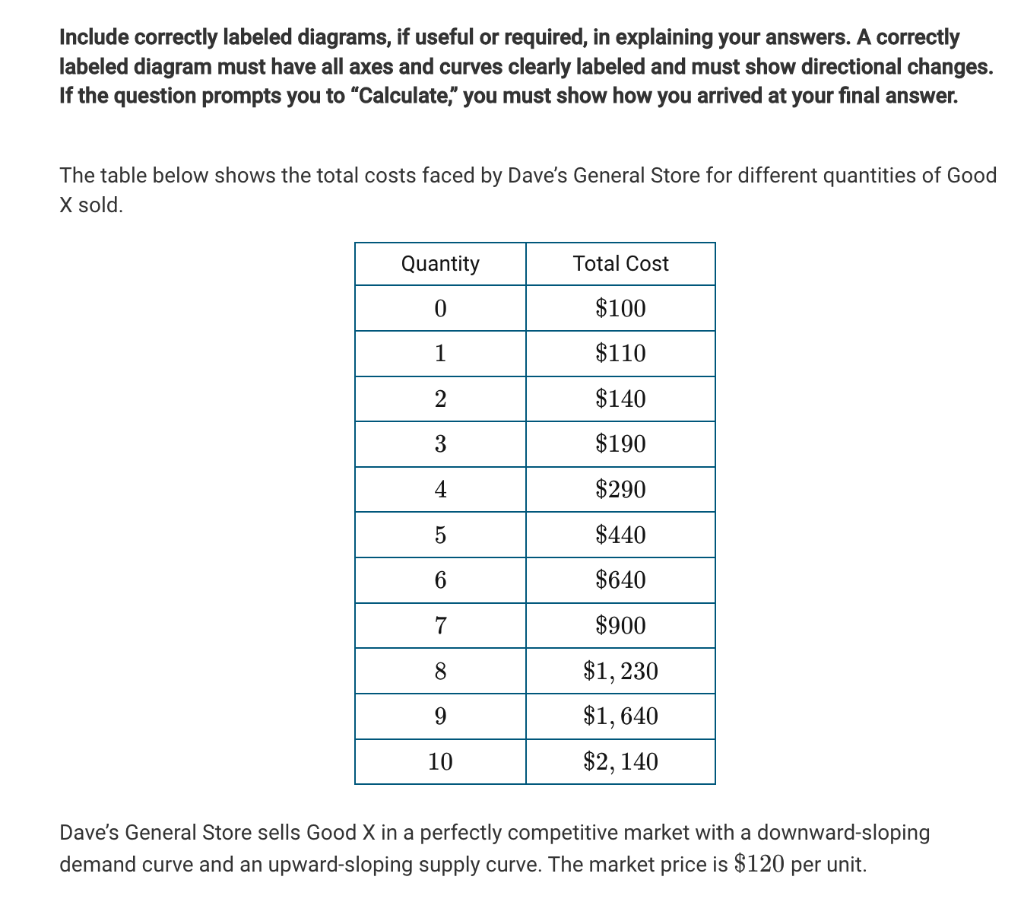

Transcribed Image Text:Include correctly labeled diagrams, if useful or required, in explaining your answers. A correctly

labeled diagram must have all axes and curves clearly labeled and must show directional changes.

If the question prompts you to "Calculate," you must show how you arrived at your final answer.

The table below shows the total costs faced by Dave's General Store for different quantities of Good

X sold.

Quantity

0

1

2

3

4

5

6

7

8

9

10

Total Cost

$100

$110

$140

$190

$290

$440

$640

$900

$1,230

$1,640

$2,140

Dave's General Store sells Good X in a perfectly competitive market with a downward-sloping

demand curve and an upward-sloping supply curve. The market price is $120 per unit.

Transcribed Image Text:(g) Now assume that the market in which Dave's General Store operates is in long-run equilibrium.

(i) Suppose the rent paid by Dave's General Store decreases. Will Dave's General Store's profit-

maximizing quantity of Good X increase, decrease, or stay the same in the short run? Explain.

(ii) Instead suppose Dave's General Store hires labor in a perfectly competitive market and the market

wage increases. Will Dave's General Store's profit-maximizing quantity of Good X increase, decrease,

or stay the same in the short run? Explain.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: Applications, Strategies an…

Economics

ISBN:

9781305506381

Author:

James R. McGuigan, R. Charles Moyer, Frederick H.deB. Harris

Publisher:

Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:

9781337106665

Author:

Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:

Cengage Learning