In 2021, the internal auditors of Blooper Inc. discovered that goods costing $12 million that were shipped f.o.b. shipping point in December of 2020 were in transit on December 31. The goods were recorded as a purchase in December of 2020 but were not included in the 2020 year-end inventory. Prepare the journal entry needed in 2021 to correct the error. (If no entry is required for a transaction/event, select "No journal entr required" in the first account field. Enter your answers in millions (1.e., 10,000,000 should be entered as 10).) View transaction list Journal entry worksheet Record the hecessary entry to correct the error.

In 2021, the internal auditors of Blooper Inc. discovered that goods costing $12 million that were shipped f.o.b. shipping point in December of 2020 were in transit on December 31. The goods were recorded as a purchase in December of 2020 but were not included in the 2020 year-end inventory. Prepare the journal entry needed in 2021 to correct the error. (If no entry is required for a transaction/event, select "No journal entr required" in the first account field. Enter your answers in millions (1.e., 10,000,000 should be entered as 10).) View transaction list Journal entry worksheet Record the hecessary entry to correct the error.

Cornerstones of Financial Accounting

4th Edition

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Jay Rich, Jeff Jones

Chapter6: Cost Of Goods Sold And Inventory

Section: Chapter Questions

Problem 71BPSB

Related questions

Question

Transcribed Image Text:Saved

Help

Save

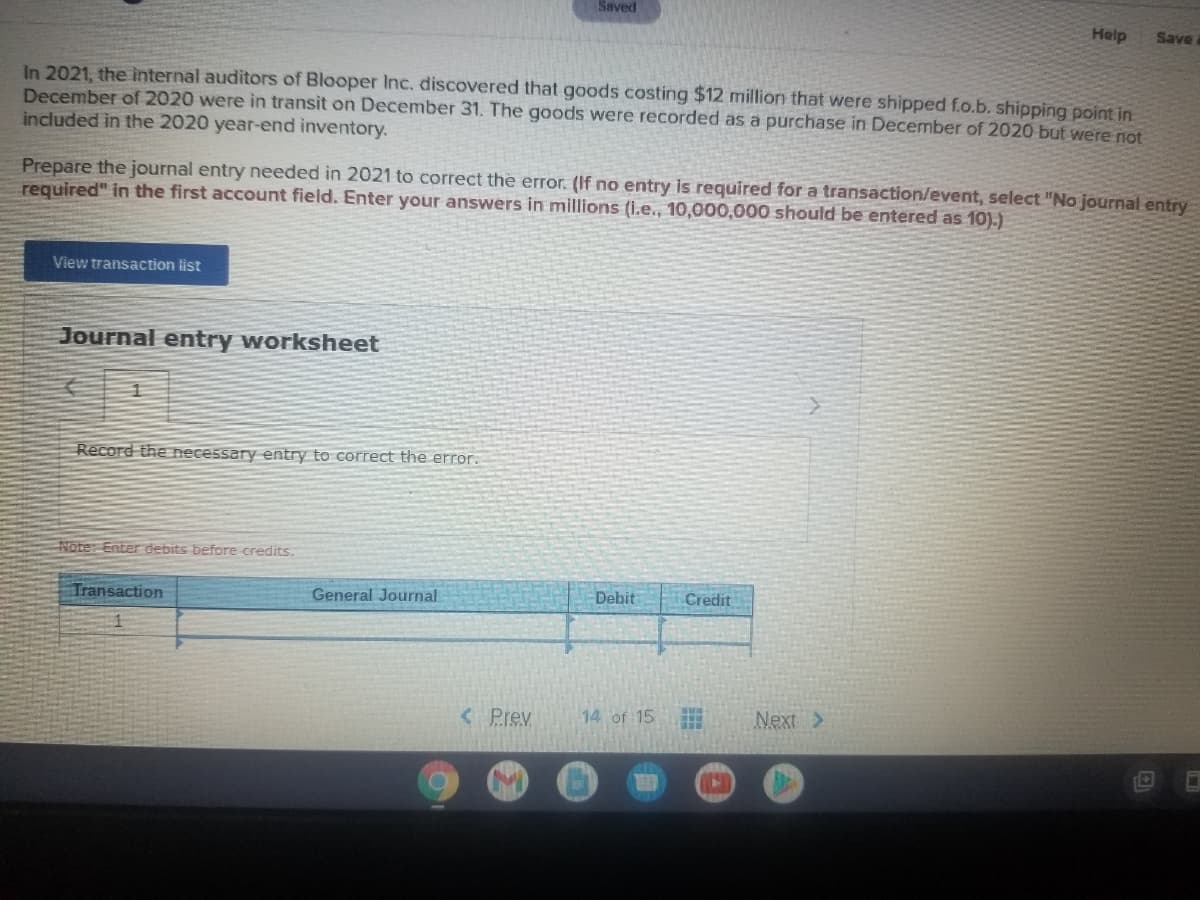

In 2021, the internal auditors of Blooper Inc. discovered that goods costing $12 million that were shipped f.o.b. shipping point in

December of 2020 were in transit on December 31. The goods were recorded as a purchase in December of 2020 but were not

included in the 2020 year-end inventory.

Prepare the journal entry needed in 2021 to correct the error. (If no entry is required for a transaction/event, select "No journal entry

required" in the first account field. Enter your answers in millions (i.e., 10,000,000 should be entered as 10).)

View transaction list

Journal entry worksheet

Record the necessary entry to correct the error.

Note: Enter debits before credits.

Transaction

General Journal

Debit

Credit

< Prev

14 of 15

Next >

Transcribed Image Text:Chapter 9 i

Saved

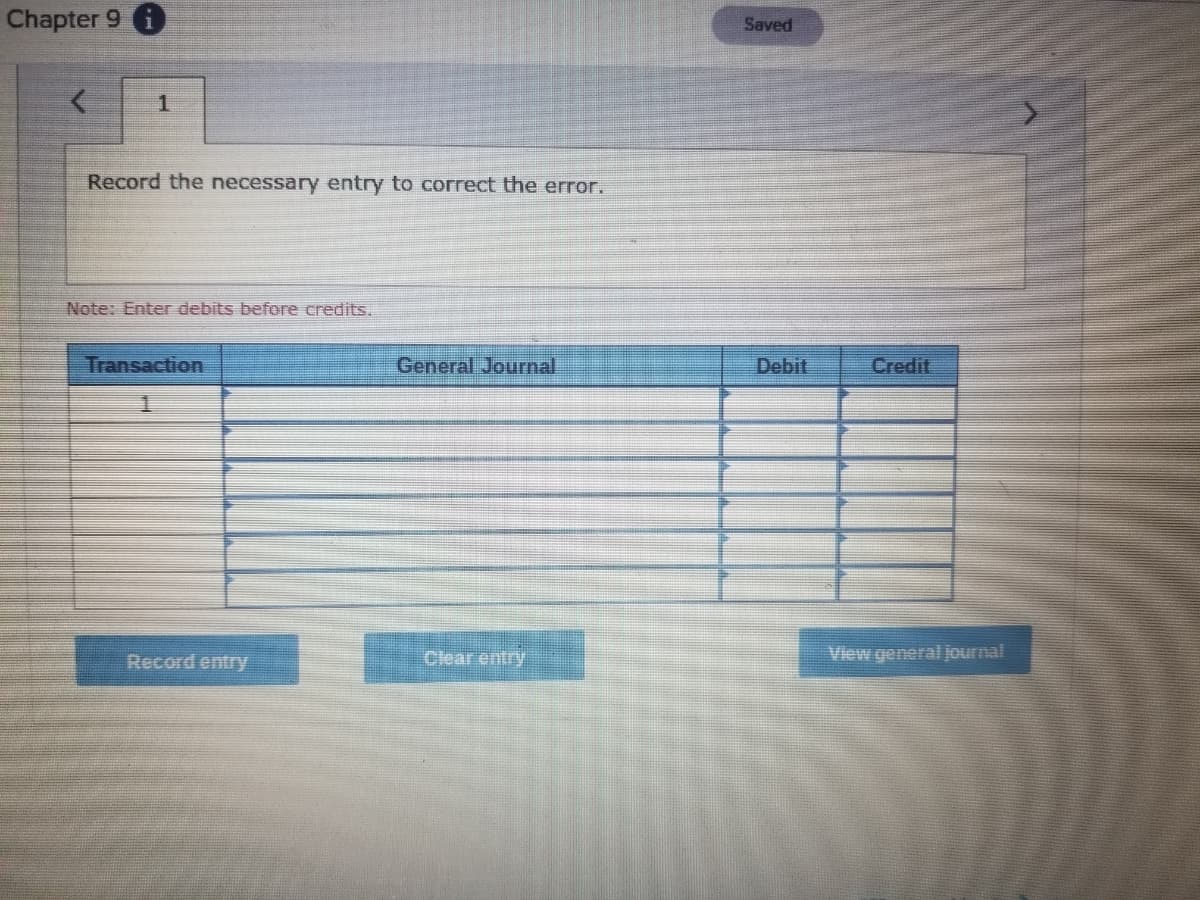

Record the necessary entry to correct the error.

Note: Enter debits before credits.

Transaction

General Journal

Debit

Credit

Record entry

Clear entry

View general journal

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning