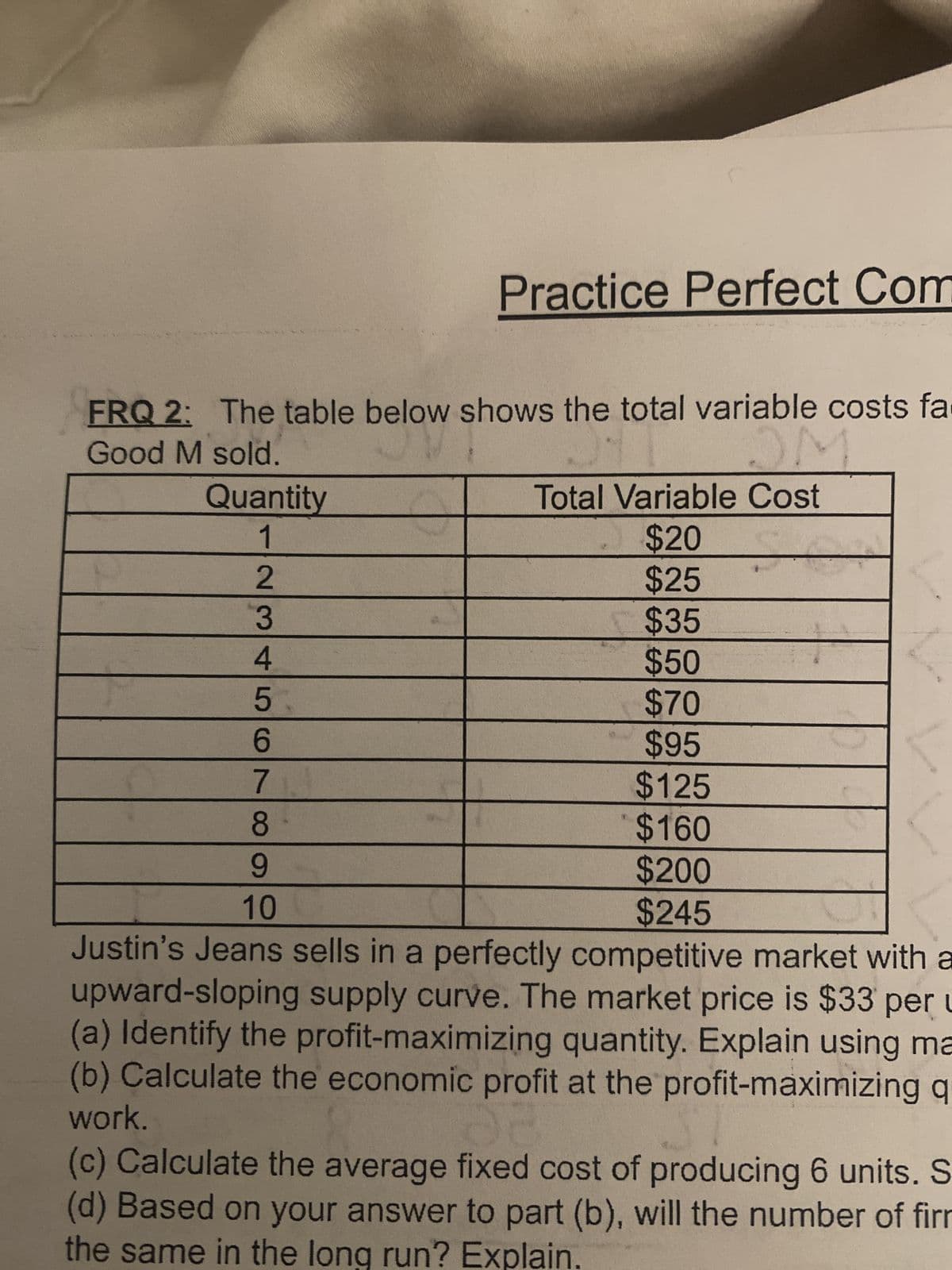

Justin’s Jeans sells in a perfectly competitive market with a downward-sloping demand curve and an upward-sloping supply curve. The market price is $33 per unit, and the total fixed cost is $30. (a) Identify the profit-maximizing quantity. Explain using marginal analysis. (b) Calculate the economic profit at the profit-maximizing quantity you identified in part (a). Show your work. (c) Calculate the average fixed cost of producing 6 units. Show your work.

Justin’s Jeans sells in a

(a) Identify the profit-maximizing quantity. Explain using marginal analysis.

(b) Calculate the economic profit at the profit-maximizing quantity you identified in part (a). Show your work.

(c) Calculate the average fixed cost of producing 6 units. Show your work.

(d) Based on your answer to part (b), will the number of firms in the industry increase, decrease, or stay the same in the long run? Explain.

(e) Based on your answer to part (b), will the market price increase, decrease, or stay the same in the long run? Explain.

(f) The income elasticity of demand for Good M is 1.4, and the cross-

(g) Now assume that the market in which Justin’s Jeans operates is in long-run equilibrium at a price of $30 per unit.

(i) Suppose annual property taxes for Justin’s Jeans increase by $2,000. Will the profit-maximizing quantity of Good M for Justin’s Jeans increase, decrease, or stay the same in the short run? Explain.

(ii) Instead suppose the government imposes a

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

(b) Calculate the economic profit at the profit-maximizing quantity you identified in part (a). Show your work.