Kenneth, 32 years old, is a business development manager working for a 2-year-old start-up company running a cryptocurrency exchange. He is paid a monthly salary of $5,000 and an additional business allowance of $1,000 per month. While the company is well-funded by a private equity fund from China, he does not get any bonus as the company is still in the red. His boss has told him that the company will start making money once the MAS approves their application for a Payment Services License. He was also told that the odds of getting the license is 50%. Although he knows his career and income is not very secured in the short run, he does not see th need to manage his spendthrift lifestyle. This is because he is single, and his parents are financially independent and they are happy to allowed him to stay with them as he is the only so Kenneth does not own any property or a car now, hence he does not have a mortgage or car loan. The only debt that he is repaying every month now and for the next few years is a substantial DBS credit card debt which he chalked up last year due to his over spending habit o branded apparel and leather goods, and an expensive Rolex Daytona Chronograph watch. He has also inflated those credit card debt by paying for his daily commute in taxi, Grab and Gojek

Kenneth, 32 years old, is a business development manager working for a 2-year-old start-up company running a cryptocurrency exchange. He is paid a monthly salary of $5,000 and an additional business allowance of $1,000 per month. While the company is well-funded by a private equity fund from China, he does not get any bonus as the company is still in the red. His boss has told him that the company will start making money once the MAS approves their application for a Payment Services License. He was also told that the odds of getting the license is 50%. Although he knows his career and income is not very secured in the short run, he does not see th need to manage his spendthrift lifestyle. This is because he is single, and his parents are financially independent and they are happy to allowed him to stay with them as he is the only so Kenneth does not own any property or a car now, hence he does not have a mortgage or car loan. The only debt that he is repaying every month now and for the next few years is a substantial DBS credit card debt which he chalked up last year due to his over spending habit o branded apparel and leather goods, and an expensive Rolex Daytona Chronograph watch. He has also inflated those credit card debt by paying for his daily commute in taxi, Grab and Gojek

Chapter9: Acquisitions Of Property

Section: Chapter Questions

Problem 51P

Related questions

Question

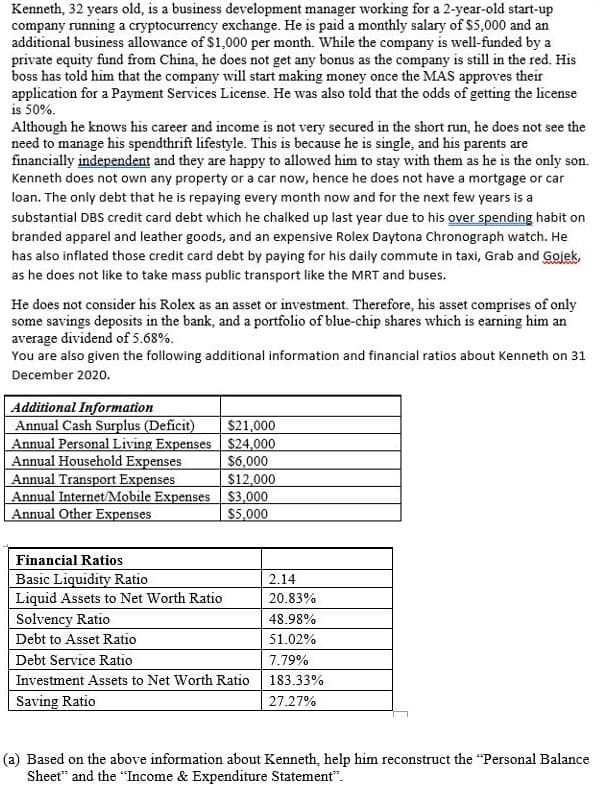

Transcribed Image Text:Kenneth, 32 years old, is a business development manager working for a 2-year-old start-up

company running a cryptocurrency exchange. He is paid a monthly salary of $5,000 and an

additional business allowance of $1,000 per month. While the company is well-funded by a

private equity fund from China, he does not get any bonus as the company is still in the red. His

boss has told him that the company will start making money once the MAS approves their

application for a Payment Services License. He was also told that the odds of getting the license

is 50%.

Although he knows his career and income is not very secured in the short run, he does not see the

need to manage his spendthrift lifestyle. This is because he is single, and his parents are

financially independent and they are happy to allowed him to stay with them as he is the only son.

Kenneth does not own any property or a car now, hence he does not have a mortgage or car

loan. The only debt that he is repaying every month now and for the next few years is a

substantial DBS credit card debt which he chalked up last year due to his over spending habit on

branded apparel and leather goods, and an expensive Rolex Daytona Chronograph watch. He

has also inflated those credit card debt by paying for his daily commute in taxi, Grab and Gojek,

as he does not like to take mass public transport like the MRT and buses.

He does not consider his Rolex as an asset or investment. Therefore, his asset comprises of only

some savings deposits in the bank, and a portfolio of blue-chip shares which is earning him an

average dividend of 5.68%.

You are also given the following additional information and financial ratios about Kenneth on 31

December 2020.

Additional Information

Annual Cash Surplus (Deficit)

Annual Personal Living Expenses $24,000

Annual Household Expenses

Annual Transport Expenses

Annual Internet/Mobile Expenses $3,000

Annual Other Expenses

$21,000

S6,000

$12,000

$5,000

Financial Ratios

Basic Liquidity Ratio

Liquid Assets to Net Worth Ratio

Solvency Ratio

Debt to Asset Ratio

2.14

20.83%

48.98%

51.02%

Debt Service Ratio

7.79%

Investment Assets to Net Worth Ratio

183.33%

Saving Ratio

27.27%

(a) Based on the above information about Kenneth, help him reconstruct the "Personal Balance

Sheet" and the "Income & Expenditure Statement".

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT