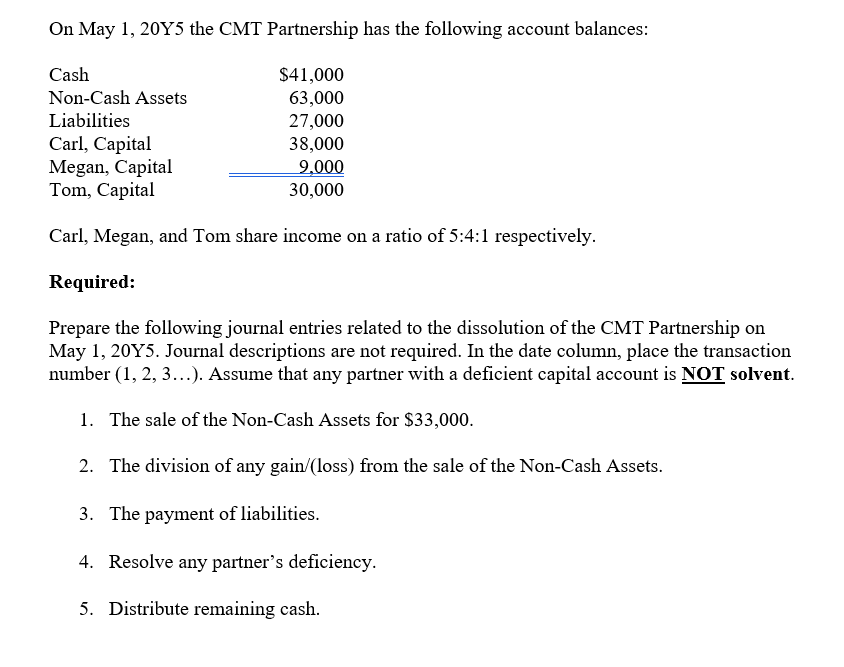

On May 1, 20Y5 the CMT Partnership has the following account balances: Cash $41,000 Non-Cash Assets 63,000 Liabilities 27,000 Carl, Capital Megan, Capital Tom, Capital 38,000 9,000 30,000 Carl, Megan, and Tom share income on a ratio of 5:4:1 respectively. Required: Prepare the following journal entries related to the dissolution of the CMT Partnership on May 1, 20Y5. Journal descriptions are not required. In the date column, place the transaction number (1, 2, 3...). Assume that any partner with a deficient capital account is NOT solvent. 1. The sale of the Non-Cash Assets for $33,000. 2. The division of any gain/(loss) from the sale of the Non-Cash Assets. 3. The payment of liabilities. 4. Resolve any partner's deficiency. 5. Distribute remaining cash.

Partnership Accounting

A partnership is a kind of arrangement between two or more people whereby they agree to manage the business operations and share its profits and losses in an agreed ratio between them. The agreement that is drafted and signed by the partners of the firm is termed as partnership deed and contains various important clauses agreed between the partners such as profit/loss sharing, interest on capital, remuneration allocation of each partner, drawings, admission of a new partner, etc.

Partner Admission and Withdrawal

A partnership is a kind of arrangement between two or more people whereby they agree to manage the business operations and share its profits and losses in an agreed ratio between them. The agreement that is drafted and signed by the partners of the firm is termed as a partnership deed and contains various important clauses agreed between the partners such as profit/loss sharing, interest on capital, remuneration allocation of each partner, drawings of a partner, etc.

Step by step

Solved in 2 steps