Q: Suppose the market for coffee is characterized by perfect competition. Assume that all firms are…

A: Answer: Given, LATC (long-run average total cost) function: LATC=Q+5+25Q LMC (long-run marginal…

Q: Each of 6 identical firms in a competitive market has a cost function: C= 30 + 2q? and the market…

A: There are 6 identical firms in the perfectly competitive market. Each firm has following cost…

Q: If a perfectly competitive firm increases production from 10 units to 11 units and the market price…

A: The perfect-competition is a form of market, where all the firms are price-taker and the prices(P)…

Q: The demand curve for guitars is given by Pd = 200 - 5Qd and supply for guitars is given by Ps = 20 +…

A: demand function is Pd = 200 - 5Qd and supply function is Ps = 20 + Qs Total surplus is : Consumer…

Q: Given P = 300 + 200Qs (demand equation), P = 6300 − 50Qd (supply equation), and TC = 500 + 10Q +…

A: For a competitive firm, prices are given and it has to produce where P=MC Where P is determined by…

Q: Consider a competitive industry with a large number of firms, all of which have identical cost…

A: In a competitive market a firm produces output at P=MC Where MC = dC/dY

Q: Next, consider a case that the integrated firm produce the product and sell directly to consumers.…

A: Introduction Here we have a case of integrated market where firm produces the product and sell…

Q: Two separate firms produce the complimentary goods of left shoes and right shoes. Assume the demand…

A: In economics, the marginal cost is the alternate withinside the overall cost that arises whilst the…

Q: The solar-heating industry in a southwestern state is composed of just two firms. The market for…

A: Firm 1 profit : pi1 = 5Q1 - Q12 - 0.5Q22 + 12 Firm 2 profit : pi2 = 9Q2 - 1.5Q22 - Q12 + 20 When…

Q: Assume that marginal revenue equals rising marginal cost at 100 units of output. At this output…

A: Here, given information is: Output level= 100 units Average total cost= $11 Total variable cost=…

Q: Suppose that there are 100 consumers in a perfectly competitive market and individual demand curves…

A: Perfectly competitive market refers to such a market where there are very large number of buyers and…

Q: Q.3 Two firms produce homogeneous products. The inverse demand function is given by: p(x₁, x2) =…

A:

Q: A firm's demand function is Q = 16 – P and its total cost function is defined as TC = 3 + Q +…

A: Profit depends on total revenue and total cost of a firm. Profit is a difference between total…

Q: Assume that the cannabis firm called Aphria Inc. purchases resources a and b under perfectly…

A: The profit is maximum at:MP* price equal to input prices

Q: Each of the 8 firms in a competitive market has a cost function of C= 5+q°. The market demand…

A: A Perfectly competitive firm has a constant price at all levels of output. Profit is maximized at…

Q: Suppose the price reaction function for Mars' chocolate bars is Pm = (Vm+cm)/2)+0.5Ph, where Pm is…

A: Price reaction function for Mars chocolate is:- Pm = (Vm +Cm)/2) + 0.5Ph Price reaction function for…

Q: Suppose that there are 90 firms in a market, each with the following cost function: C(q) = 11 + 5q².…

A: We first derive the individual supply curve, Cost firm bears, C(q)=11+5q2 Firm will sell at the…

Q: Description Throughout this Quiz, we will consider of an industry with either one or two firms in…

A: Considering both firms to be profit maximizing: IN case of bertrand competition where firms charge…

Q: Suppose the cost function of firm A, which produces two goods, is given by C = 100 − .5 Q1Q2 +…

A: Cost complementarity is the decline in MC due to increase in production. Economies of scope:…

Q: Derive the profit function 7(p) and supply function (or correspondence) y(p) for the single-output…

A: GIVEN Derive the profit function ∏(p) and supply function (or correspondence) y(p) for the…

Q: firm’s production function is Q = 10 + 30L - .5L2+ 30K – K2, and its competitive demand function is…

A: Answer A firm’s production function is Q = 10 + 30L - 0.5L2 + 30K – K2 MPL = = 40 - L At…

Q: All of the following are ways by which existing firms can deter the entry of new firms into an…

A: The answer to above is (A) threating to raise prices. When a new firm enters the industry , it faces…

Q: Please Answer both questions briefly Q1. What are the equilibrium conditions for a firm operating…

A: Note: Since you've asked multiple question, we will solve the first question for you. If you want…

Q: inverse demand function is P = 200 -20, and the firm's cost function is C( Determine the firm's…

A: A contestable market is that market where no restrictions to entry and exit. When firms in a…

Q: Here is a market with three firms: 1, 2, and 3. The demand curve is P=100-Q. There is no fixed cost…

A: The demand curve is a graphical representation of the relationship between a good's or service's…

Q: Solve the attahment.

A: Given: Cost function: C(Q) = 100 + Q2 Price = $10

Q: Suppose the doll company American Girl has an inverse demand curve of P = 150 – 0.25Q, where Q…

A: Total cost (TC): - it is the sum of fixed and variable costs incurred in the production process.…

Q: The information below applies to a competitive firm that sells its output for $44.00 per unit. •…

A: In a competitive equilibrium, Price=Marginal Revenue. MR=44 Now, we calculate Marginal Cost When…

Q: Suppose you are given the following information about a particular industry: QD = 8800 – 100P Market…

A: At equilibrium, quantity demanded = quantity supplied and perfectly competitive firms are price…

Q: Question 19 relies on the following information: Vendors L and R sell a homogenous output at prices…

A: Introduction Values of two vendors L and R has given. Value of vendor L is V = 10 - PL - 4ti here t…

Q: Next, consider a case that the integrated firm produce the product and sell directly to consumers.…

A: We have demand for integrated firm is p=70-q and MC= 10.

Q: Suppose the daily demand function for pizza in St. Catharines is Qd = 1525 – 5P. For one pizza…

A: Given, Qd = 1525 − 5P C(q) = 3q+0.01q2 MC = 3 + 0.02q

Q: Given that a firm's inverse demand function is P = 100 – 5Q and total cost is given by C = 550 +…

A: Profit maximizing quantity of output is when marginal revenue equals marginal cost.

Q: Assume that a competitive firm has the total cost function:…

A: The perfect competition is the market structure which is characterized by the presence of a large…

Q: Assume a firm's marginal costs are increasing at its current level of output. If a firm's marginal…

A: Marginal costs are the costs that measure the change in the total cost of production when the…

Q: The figure deplcts the demand curve for Beautiful Cars, and the marginal cost and Isoprofit curves…

A: Demand curve is a graphic representation of the relationship between price of the product and the…

Q: The inverse market demand curve for bean sprouts is given by: P(Y) = 100-2Y, The total cost…

A: The Stackelberg model was created by H.von Stackelberg and in this model, firms move sequentially…

Q: Consider the competitive firm in Figure 3-1. At the profit maximizing level of output, the firm is…

A: Economic profit or loss can be understood as the difference which occur between revenue from sales…

Q: Consider a competitive industry with a large number of firms, all of which have identical cost…

A: In the short run, a competitive firm produces output where price is equal to its marginal cost.

Q: Assume that marginal revenue equals rising marginal cost at 100 units of output. At this output…

A: Price = 3 Average variable cost = variable cost/ output = 600/100 = 6 Since the price is below the…

Q: 2. Consider a market for a homogenous good with the following inverse demand function: P = 52 – 2Q…

A: we have P=52-2Q and Total cost C(Q)=4Q so π(profit) = TR-TC=PxQ-TC=(52-2Q)Q-4Q=52Q-2Q2-4Q Thus…

Q: A firm produces two goods in pure competition and has the following total revenue and total cost…

A: Given: The total revenue function is TR = P1Q1 + P2Q2 The total cost function is TC = 2Q12 + Q1Q2…

Q: Suppose that the identical firms in a perfectly competitive market for cakes have long-run total…

A: To calculate P we know that MC is equal to The ATC in the long-run supply curve because the…

Q: Suppose that the market inverse demand function is p(yT)=80-yT and the firm's total cost functions…

A: A duopoly market structure is a type of oligopoly where two firms have dominant or exclusive control…

Q: Assume that there are two firms in a market with inverse demand function P(Q) = 120-Q. Both firms…

A: Consumer surplus means a situation in which the willing to pay price by the consumer is higher than…

Q: The inverse demand function is P = 200 – 2Q. Total cost is zero. Calculate output, price, and…

A: The oligopoly market is the type of market structure where there are few firms in the market but…

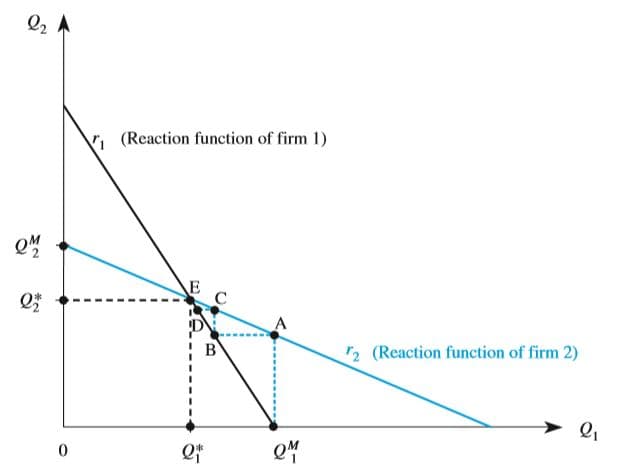

In Figure, what is the profit-maximizing level of output for firm 2 when firm 1 produces zero units of output? What is it when firm 1 produces Q*1 units?

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 4 images

- When average cost decreases as output increases, Group of answer choices marginal cost is below average cost average variable cost is rising average fixed cost is rising marginal cost is above average cost1. A firm that sells in two separate markets has the profit function where q1 and q2 sales in the two markets. Find the profit maximizing sales in each market, using the Hessian to check second-order conditions for a maximum. 2. Find the values of q1 and q2 that will maximizing the profit function and check that second-order conditions are met using the Hessian matrix.Differentiate economies of scale and economies of scope.

- Average fixed cost Multiple Choice declines continuously as output is expanded. keeps constant as output is expanded. increases continuously as output increases. initially declines, reaches a minimum, and then begins to increase as output increases.Before the point of diminishing marginal returns, marginal cost will be increasing. Group of answer choices True FalseIn economics, profit revenue marginal cost small incremental changes or adjustments are identified as _____.

- Suppose the situation changes. JointJuice has its plant in Portland Oregon. The local government passes a new tax on businesses that raises JointJuice’s fixed cost by $25 per period. The cost function now becomes: C(q) = 300 + 6q + 0.1q^2 All the other firms in the market are in other states/cities that are not subject to the laws or taxes of Portland. Calculate JointJuice’s optimal output level and profits if the market price for the product stays the same as for part a. What will the firm do in the long run? Is it reasonable to assume the market price prevailing today will remain the same in the long run? If so why? If not, why not? How about the number of firms in the market?The manufacturer of an energy drink spends $1.28 to make each drink and sells them for $3.27. The manufacturer also has fixed costs each month of $835.8.ⓐ Find the cost function C when x energy drinks are manufactured. C(x)= ⓑ Find the revenue function R when x drinks are sold. R(x)= ⓒ Find the break-even point. (Enter you answer as an ordered pair of the form (x,$). __________________For a certain product, suppose that total costs are given by c(x) = 1600 + 1500x and total revenues by R(x) = 1600x-x2 (b) Find the profit function, p(x). c) Find the number of units that will maximize profit. (d) Find the maximum profit.