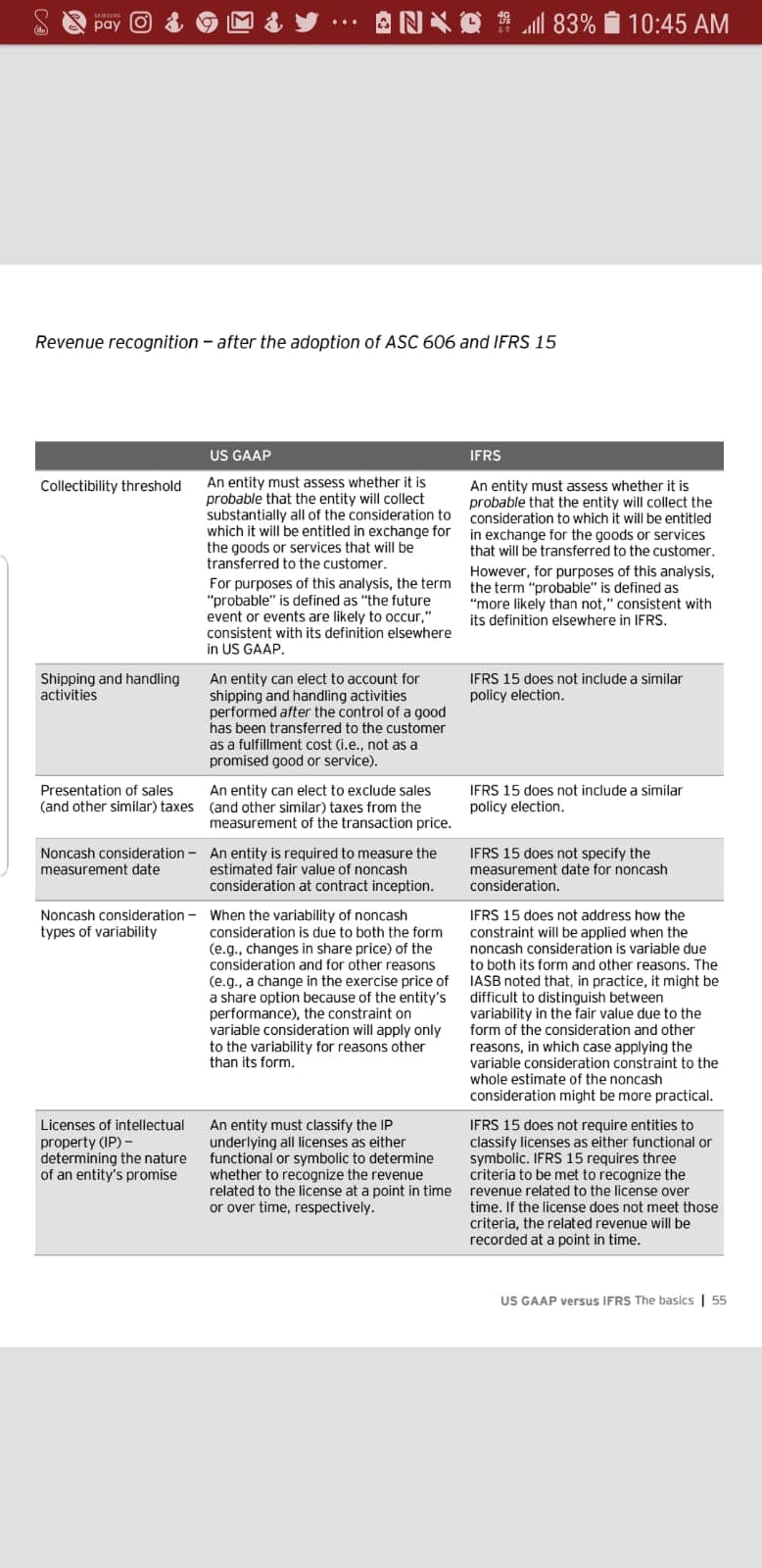

Revenue recognition-after the adoption of ASC 606 and IFRS 15 US GAAP IFRS Collectibility threshold An etity must assess whether it is probable that the entity will collect substantially all of the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer An entity must assess whether it is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer For purposes of this analysis, the term "probable" is defined as "the future event or events are likely to occur," consistent with its definition elsewhere in US GAAP. However, for purposes of this analysis, the term "probable" is defined as "more likely than not," consistent with its definition elsewhere in IFRS Shipping and handling activities An entity can elect to account for shipping and handling activities performed after the control of a good has been transferred to the customer as a fulfillment cost (i.e., not as a promised good or service) IFRS 15 does not include a similar policy election Presentation of sales (and other similar) taxes entity can elect to exclude sales (and other similar) taxes from the measurement of the transaction price FRS 15 does not include a similar policy election. Noncash consideration An entity is required to measure the IFRS 15 does not specify the measurement date estimated fair value of noncash consideration at contract inception consideration. measurement date for noncash Noncash considerationWhen the variability of noncash types of variability IFRS 15 does not address how the consideration is due to both the form constraint will be applied when the (e.g., changes in share price) of the nncash consideration is variable due consideration and for other reasons to both its form and other reasons. The (e.g., a change in the exercise price ofIASB noted that, in practice, it might be a share option because of the entity's difficult to distinguish between performance), the constraint on variable consideration will apply only orm of the consideration and other to the variability for reasons other than its form. variability in the fair value due to the reasons, in which case applying the variable consideration constraint to the whole estimate of the noncash consideration might be more practical Licenses of intellectual property (IP)- determining the nature of an entity's promise An entity must classify the IP underlying all licenses as either functional or symbolic to determine whether to recognize the revenue related to the license at a point in time or over time, respectively. IFRS 15 does not require entities to classify licenses as either functional or ymbolic. IFRS 15 requires three criteria to be met to recognize the revenue related to the license over time. If the license does not meet those criteria, the related revenue will be recorded at a point in time US GAAP versus IFRS The basics55

Revenue recognition-after the adoption of ASC 606 and IFRS 15 US GAAP IFRS Collectibility threshold An etity must assess whether it is probable that the entity will collect substantially all of the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer An entity must assess whether it is probable that the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer For purposes of this analysis, the term "probable" is defined as "the future event or events are likely to occur," consistent with its definition elsewhere in US GAAP. However, for purposes of this analysis, the term "probable" is defined as "more likely than not," consistent with its definition elsewhere in IFRS Shipping and handling activities An entity can elect to account for shipping and handling activities performed after the control of a good has been transferred to the customer as a fulfillment cost (i.e., not as a promised good or service) IFRS 15 does not include a similar policy election Presentation of sales (and other similar) taxes entity can elect to exclude sales (and other similar) taxes from the measurement of the transaction price FRS 15 does not include a similar policy election. Noncash consideration An entity is required to measure the IFRS 15 does not specify the measurement date estimated fair value of noncash consideration at contract inception consideration. measurement date for noncash Noncash considerationWhen the variability of noncash types of variability IFRS 15 does not address how the consideration is due to both the form constraint will be applied when the (e.g., changes in share price) of the nncash consideration is variable due consideration and for other reasons to both its form and other reasons. The (e.g., a change in the exercise price ofIASB noted that, in practice, it might be a share option because of the entity's difficult to distinguish between performance), the constraint on variable consideration will apply only orm of the consideration and other to the variability for reasons other than its form. variability in the fair value due to the reasons, in which case applying the variable consideration constraint to the whole estimate of the noncash consideration might be more practical Licenses of intellectual property (IP)- determining the nature of an entity's promise An entity must classify the IP underlying all licenses as either functional or symbolic to determine whether to recognize the revenue related to the license at a point in time or over time, respectively. IFRS 15 does not require entities to classify licenses as either functional or ymbolic. IFRS 15 requires three criteria to be met to recognize the revenue related to the license over time. If the license does not meet those criteria, the related revenue will be recorded at a point in time US GAAP versus IFRS The basics55

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter17: Advanced Issues In Revenue Recognition

Section: Chapter Questions

Problem 1C: Prior to ASU 2014-09 changing the principles underlying revenue recognition, companies recognized...

Related questions

Question

100%

Choose three out of six differences on page 55, (attached) and, for each of these three differences, "explain" whether you prefer IFRS or U.S. GAAP.?

Transcribed Image Text:Revenue recognition-after the adoption of ASC 606 and IFRS 15

US GAAP

IFRS

Collectibility threshold An etity must assess whether it is

probable that the entity will collect

substantially all of the consideration to

which it will be entitled in exchange for

the goods or services that will be

transferred to the customer

An entity must assess whether it is

probable that the entity will collect the

consideration to which it will be entitled

in exchange for the goods or services

that will be transferred to the customer

For purposes of this analysis, the term

"probable" is defined as "the future

event or events are likely to occur,"

consistent with its definition elsewhere

in US GAAP.

However, for purposes of this analysis,

the term "probable" is defined as

"more likely than not," consistent with

its definition elsewhere in IFRS

Shipping and handling

activities

An entity can elect to account for

shipping and handling activities

performed after the control of a good

has been transferred to the customer

as a fulfillment cost (i.e., not as a

promised good or service)

IFRS 15 does not include a similar

policy election

Presentation of sales

(and other similar) taxes

entity can elect to exclude sales

(and other similar) taxes from the

measurement of the transaction price

FRS 15 does not include a similar

policy election.

Noncash consideration An entity is required to measure the IFRS 15 does not specify the

measurement date

estimated fair value of noncash

consideration at contract inception consideration.

measurement date for noncash

Noncash considerationWhen the variability of noncash

types of variability

IFRS 15 does not address how the

consideration is due to both the form constraint will be applied when the

(e.g., changes in share price) of the nncash consideration is variable due

consideration and for other reasons to both its form and other reasons. The

(e.g., a change in the exercise price ofIASB noted that, in practice, it might be

a share option because of the entity's difficult to distinguish between

performance), the constraint on

variable consideration will apply only orm of the consideration and other

to the variability for reasons other

than its form.

variability in the fair value due to the

reasons, in which case applying the

variable consideration constraint to the

whole estimate of the noncash

consideration might be more practical

Licenses of intellectual

property (IP)-

determining the nature

of an entity's promise

An entity must classify the IP

underlying all licenses as either

functional or symbolic to determine

whether to recognize the revenue

related to the license at a point in time

or over time, respectively.

IFRS 15 does not require entities to

classify licenses as either functional or

ymbolic. IFRS 15 requires three

criteria to be met to recognize the

revenue related to the license over

time. If the license does not meet those

criteria, the related revenue will be

recorded at a point in time

US GAAP versus IFRS The basics55

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College