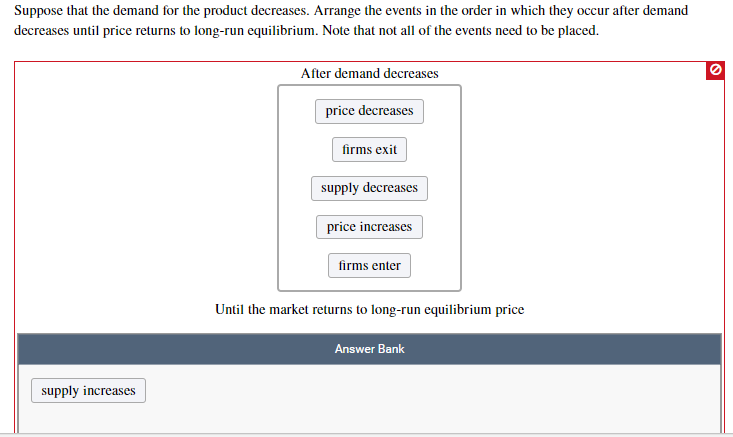

Suppose that the demand for the product decreases. Arrange the events in the order in which they occur after demand decreases until price returns to long-run equilibrium. Note that not all of the events need to be placed. After demand decreases price decreases firms exit supply decreases price increases firms enter Until the market returns to long-run equilibrium price Answer Bank supply increases

Q: In the short run, firms will . In the long run, the supply curve will On the previous graph, show…

A:

Q: PRICE (Dollars per quart) Short-run Subply Demand Short-run Supply Short-run Equilbrium Demand…

A: The curve that depicts various quantities of goods and services being demanded at various price…

Q: Consider the equilibrium depicted as your final short-run equilibrium (SRE). Is your price depicted…

A: A perfect market, sometimes known as an atomistic market, is defined by various idealising…

Q: Improved robot technology was recently incorporated into the process of producing automobiles. What…

A: The supply schedule is the tabular representation of the price and quantity supplied. The supply…

Q: Supply tends to be more elastic in the short-run, and less elastic in the long-run. Group of answer…

A: The notion of supply is used in economics to determine the quantity of an item or service produced…

Q: The ability of firms to enter and exit a market over time means that, in the long run, a. the demand…

A: Elasticity is an economic measure that determines the reactive nature of the quantity to the changes…

Q: True or false: In economics, excess supply in a competitive market with no intervention will lead…

A: Diseconomies of scale will take place,when the average cost increases and the output decreases.…

Q: The slow recovery from the recession of 2007–2009 forced many firms to develop new competitive…

A: The slow recovery from the recession of 2007-2009 disincentivized firms to lend from financial…

Q: If the price of a substitute increases, which of the following is most likely to happen in the…

A: Substitute Good: In economics, the term 'substitute good' is used to refer to goods that can be used…

Q: Which one of the following statements is correct? The demand for the product of a perfectly…

A: (Q)Which one of the following statements is correct? The demand for the product of a perfectly…

Q: The ability of firms to enter and exit a market overtime means that, in the long run, Select one…

A: Meaning of Perfect Competition: The term perfect competition refers to the market under which…

Q: The short run supply curve for a firm in a perfectly competitive industry is its: A average cost…

A: Perfect competition is an ideal sort of market structure where all makers and purchasers have full…

Q: The profit maximizing firms in a perfectly competitive industry with free entry have average total…

A: The pure competitive market defines a market where a massive number of buyers and business companies…

Q: Firms in this industry will make economic losses in the short run. The equilibrium market price in…

A: The perfect competition would result in the large number of buyers and sellers in the market. The…

Q: With identical firms, constant input prices, and all the other characteristics of a competitive…

A: A shift in demand is the change the determinant of demand other than the prices. It is the situation…

Q: Austria is one of the largest exporters of oil. At the end of 2019, the global price of oil fell…

A: Here, it is given that the price of oil decreases, which is a final good and exported by Austria to…

Q: What relationship, if any, can you detect between the facts that farmers’ fixed costs of production…

A: The law of supply established the quantity supplied of a good or service as a positive function of…

Q: short-run market

A: In the short run, the firm will shutdown and the firm is not able to cater its variable costs.…

Q: Let Inverse market demand be the linear form: P = 39 – 0.009 Q; P is price and Q is output.…

A: Given : Inverse market demand be the linear form: P=39— 0.009 Q

Q: Question 2 For each of the following events identify which of the determinates of demand or supply…

A: “Since you have posted a question with multiple sub-parts, we will solve first three subparts for…

Q: In a competitive market with free entry and exit from the market a permanent rise in demand will…

A: A competitive market is one where there are several firms selling an identical product. Firms can…

Q: Complete the following statements. In an increasing-cost industry, an increase in demand will result…

A: When talking about increasing cost industry, it is the industry in which a firm faces an increase in…

Q: f the firm is producing at a quantity where marginal revenue exceeds marginal cost then, in order to…

A: The monetary value of production is that the distinction in total production prices that results…

Q: Consider the perfectly competitive market for gasoline. The aggregate demand forgasoline is D (p) =…

A: Perfect competitive market refers to that form of market where large numbers of sellers and buyers…

Q: The following diagram shows the market demand for steel. Use the orange points (square symbol) to…

A: In a perfectly competitive market, there is a large number of small firms selling homogenous…

Q: If firms exit an industry, the Select one: a. output of the industry increases. b. profits of…

A: "In the long-run firms exit the industry if the firms in the industry are earning economic losses."

Q: emand increases at the same time that supply increases then... Group of answer choices Equilibrium…

A: when demand increases, the price and quantity demanded increases. at the same time increase in…

Q: Create a firm model (two graphs, one for total units and one for marginal units) that shows how…

A: (i) Firms maximizes their profit by producing at an output level where the Marginal cost (Cost…

Q: Assuming the Petroleum Company of Barbados did not issue a directive for an increase in supply and a…

A: Hi, thank you for the question. As per our Honor code, we are allowed to attempt only the first…

Q: Consider that unusually good weather in Washington led to a bumper crop of blueberries in the state.…

A: We will answer the first question since the exact one was not specified. Please submit a new…

Q: Describe the situations under which a firms capacity must lag and lead to the demand ?

A: In a Market, a firm produce output to meet the market demand and to satisfy consumers' needs and…

Q: Distinguish between short-run and long-run supply curves.

A: Short run refers to a period of time during which some manufacturing elements are constant while…

Q: In the short run, firms will In the short run, the supply curve will On the previous graph, show the…

A: A perfectly competitive firm can adjust in the long run to changes in market demand for the…

Q: Draw the short-run situation in a P.C. market satisfying: Market demand and supply determines that…

A: Under perfect competition, there are a large number of firms. The firms sell identical products.…

Q: Improved robot technology was recently incorporated into the process of producing automobiles. What…

A: We will answer the first question since the exact one was not specified. Please submit a new…

Q: Suppose you own shares in a stock index fund that tracks the value of the S&P 500. The firm that…

A: Capital markets are places where profits and savings are channeled to those in need, amongst…

Q: Basic Demand and Supply analysis Show what happens in the short-run (within 1 year) when the…

A: When talking about demand and supply, any change in market condition or behavior of the market…

Q: Economists assume that by pursuing a strategy of cost minimization of production, most firms try to…

A: The producer can have either profit maximization motive or cost minimization motive. The cost…

Q: If resource prices rise and the per-unit cost of producing a product increases as the firms in an…

A: Long run supply curve refers to the portion of marginal cost curve which is above average total…

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

- Suppose that the demand for the product decreases. Arrange the events in the order in which they occur after demand decreases until price returns to long‑run equilibrium. Note that not all of the events need to be placed. After demand decreases firms enter price increases supply decreases firms exit price decreases supply increases Until the market returns to long‑run equilibrium priceStarting from an equilibrium condition, consider an increase in income in a perfectly com-petitive market with a normal good. (a) Draw the MC, ATC and price level on the same graph before and after the change in income. (b) What will happen to the number of firms in the long-run? (c) If the number of firms change, what will happen to the short-run supply curve? (d) What’s the long-run production and price level. (e) Draw the long-run supply curve.Market Equilibrium A retail chain will buy 800 televisions if the price is $350 each and 1200 if the priceis $300. A wholesaler will supply 700 of these televisions at $280 each and 1400 at $385 each. Assumingthat the supply and demand functions are linear, findthe market equilibrium point and explain what itmeans.

- A market is in long-run equilibrium and firms inthis market have identical cost structures. Supposedemand in this market decreases. Describe whathappens to the profit-maximizing output quantityfor individual firms as the market leaves and thenreturns to long-run equilibrium.1.0 - If the demand forApple Cinnamon Cheerios decreases at all prices, what will happen to thedemand curve? Show the shift in the demand curve on the same diagram and explain what happensto the firm’s output and profits.Short-run supply and long-run equilibrium Consiber the competitive market for rhodium. Assume that no matter how many firms operate in the induatry, every firm is identical and faces the same marpinal cost (MC), averapt total cost (ATC), and average variable cost (AVC ) curves plotted in the following praph. The following graph plots the market demand curve for thodium. If there were 10 firms in this market, the short-run equilibrium price of rhodium would be per pound. At that price, firms in this industry would. Therefore, in the long run, firms would the rhodium market. Because you know that competitive firms earn economic profit in the long run, you know the long-run equilibrium price must be per pound. From the graph, you can see that this means there will be firms operating in the rhodium industry in long-run equilibrium. True or False: Assuming implicit costs are positive, each of the firms operating in this industry in the long run earns positive accounting profit. True False

- In mid-2010, Saudi Arabia and Venezuela (both members of OPEC)produced an average of 8 million and 3 million barrels of oil a day,respectively. Production costs were about $20 per barrel, and the price ofoil averaged $80 per barrel. Each country had the capacity to producean extra 1 million barrels per day. At that time, it was estimated that each1-million-barrel increase in supply would depress the average price of oilby $10.a. Fill in the missing profit entries in the payoff table.b. What actions should each country take and why?Venezuela3 M barrels 4 M barrels8 M barrels _____, _____ _____, _____ Saudi Arabia9 M barrels _____, _____ _____, _____c10GameTheoryandCompetitiveStrategy.qxd 9/29/11 1:33 PM Page 430Summary 431c. Does the asymmetry in the countries’ sizes cause them to take differentattitudes toward expanding output? Explain why or why not. Commenton whether or not a prisoner’s dilemma is present.Hi there. can you please assist on the following question define the following 1. Short -run poeriod 2.Collusion 3. price elasticity of demandADVANCED ANALYSIS Currently, at a price of $2 each, 300 popsicles are sold per day in the perpetually hot town of Rostin. Consider the elasticity of supply. In the short run, a price increase from $2 to $4 is unit-elastic (Es = 1). In the long run, a price increase from $2 to $4 has an elasticity of supply of 1.50. (Hint: Apply the midpoints approach to the elasticity of supply.) a. How many popsicles will be sold each day in the short run if the price rises to $4 each? per day. b. So how many popsicles will be sold per day in the long run if the price rises to $4 each? per day. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.

- The handmade snuffbox industry is composed of 100 identical firms each having short-run total costs given by , where q is the output per day.20.5105STCqq=++(a) What is the short-run supply curve for each firm? What is the short-run supply curve for the market?(b) Suppose the demand is given by . What will be the equilibrium (both quantity and 110050QP=-price) in this marketplace? (c) What will each firm’s short-run profits be?“New England power producers are preparing for potential strain on the grid this winter [Winter 2022-23: December 2022 through February 2023] as a surge in natural-gas demand abroad threatens to reduce supplies they need to generate electricity.” For Question 1, consider the New England market for electricity prior to Winter 2022-23 by considering this setting roughly one year ago, in December 2021. Assume that in December of 2021, the market for electricity was in a short-run equilibrium. Draw a graph that shows supply and demand for electricity market in its December 2021 equilibrium. This graph will serve as a starting point for your analysis in Questions 2 through 5. When drawing this graph, please assume that the demand curve is downward sloping and supply curve is upward sloping. Clearly show the market equilibrium in December 2021, labeling the equilibrium price and quantity. Please remember to clearly label your axes, with P on the vertical axis and Q on the horizontal axis.…Answer the question on the basis of the following demand and cost data for a specific firm. Demand Data Cost Data (1) Price (2) Price (3) Quantity Output Total Cost $12.00 $10.00 6 6 $61 11.00 8.85 7 7 62 10.00 8.00 8 8 64 9.00 7.00 9 9 67 8.00 6.10 10 10 72 7.00 5.00 11 11 79 6.00 4.15 12 12 86 With the demand schedule shown by columns (2) and (3), in long-run equilibrium A) price will equal ATC B). total cost will exceed total revenue. C) marginal cost will exceed price. D) price will equal marginal revenue