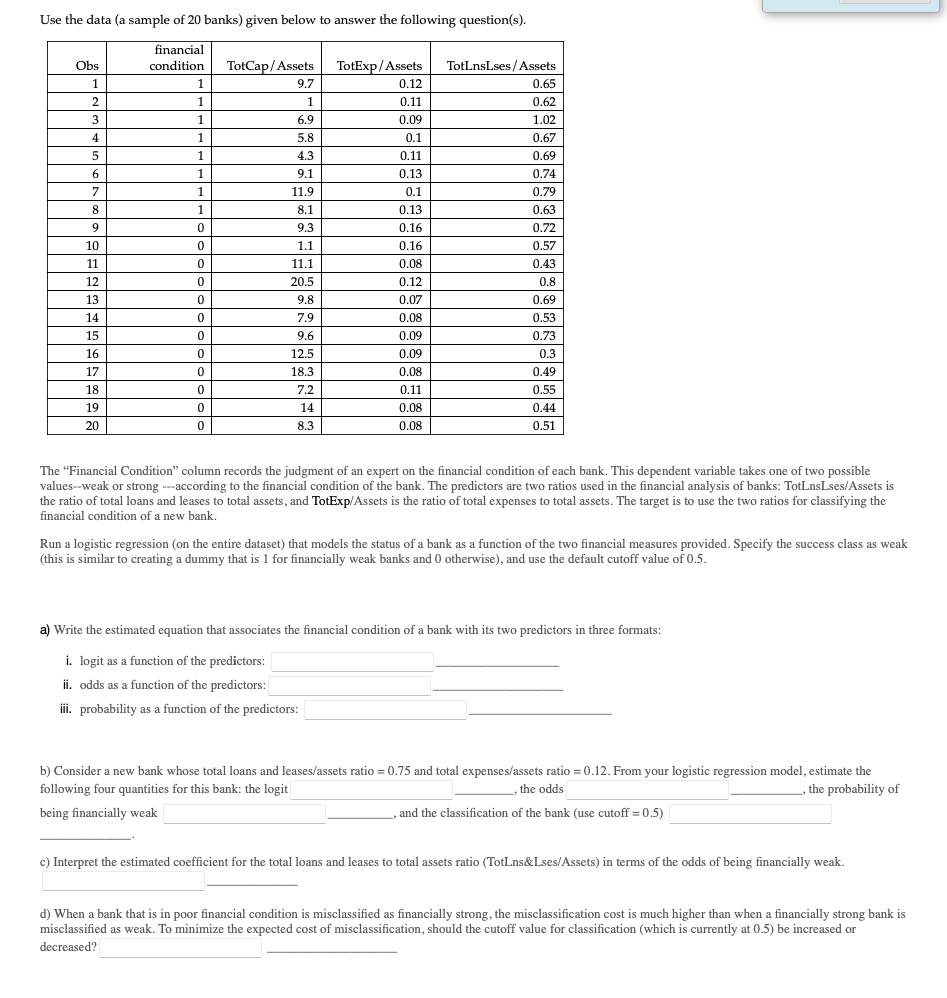

Use the data (a sample of 20 banks) given below to answer the following question(s). financial Obs condition TotCap/Assets TotExp/Assets TotLnsLses/ Assets 1 1 9.7 0.12 0.65 2 1 1 0.11 0.62 3 1 6.9 0.09 1.02 4 1 5.8 0.1 0.67 1 4.3 0.11 0.69 6. 1 9.1 0.13 0.74 7 1 11.9 0.1 0.79 8 1 8.1 0.13 0.63 9 9.3 0.16 0.72 10 1.1 0.16 0.57 11 11.1 0.08 0.43 12 20.5 0.12 0.8 13 9.8 0.07 0.69 14 7.9 0.08 0.53 15 9.6 0.09 0.73 16 12.5 0.09 0.3 17 18.3 0.08 0.49 18 7.2 0.11 0.55 19 14 0.08 0.44 20 8.3 0.08 0.51 The "Financial Condition" column records the judgment of an expert on the financial condition of each bank. This dependent variable takes one of two possible values--weak or strong ---according to the financial condition of the bank. The predictors are two ratios used in the financial analysis of banks: TotLnsLses/Assets is the ratio of total loans and leases to total assets, and TotExp/Assets is the ratio of total expenses to total assets. The target is to use the two ratios for classifying the financial condition of a new bank. Run a logistic regression (on the entire dataset) that models the status of a bank as a function of the two financial measures provided. Specify the success class as weak (this is similar to creating a dummy that is 1 for financially weak banks and 0 otherwise), and use the default cutoff value of 0.5. a) Write the estimated equation that associates the financial condition of a bank with its two predictors in three formats: i. logit as a function of the predictors: ii. odds as a function of the predictors: iii. probability as a function of the predictors: b) Consider a new bank whose total loans and leases/assets ratio = 0.75 and total expenses/assets ratio = 0.12. From your logistic regression model, estimate the following four quantities for this bank: the logit , the odds the probability of being financially weak and the classification of the bank (use cutoff = 0.5) c) Interpret the estimated coefficient for the total loans and leases to total assets ratio (TotLns&Lses/Assets) in terms of the odds of being financially weak. d) When a bank that is in poor financial condition is misclassified as financially strong, the misclassification cost is much higher than when a financially strong bank is misclassified as weak. To minimize the expected cost of misclassification, should the cutoff value for classification (which is currently at 0.5) be increased or decreased?

Use the data (a sample of 20 banks) given below to answer the following question(s). financial Obs condition TotCap/Assets TotExp/Assets TotLnsLses/ Assets 1 1 9.7 0.12 0.65 2 1 1 0.11 0.62 3 1 6.9 0.09 1.02 4 1 5.8 0.1 0.67 1 4.3 0.11 0.69 6. 1 9.1 0.13 0.74 7 1 11.9 0.1 0.79 8 1 8.1 0.13 0.63 9 9.3 0.16 0.72 10 1.1 0.16 0.57 11 11.1 0.08 0.43 12 20.5 0.12 0.8 13 9.8 0.07 0.69 14 7.9 0.08 0.53 15 9.6 0.09 0.73 16 12.5 0.09 0.3 17 18.3 0.08 0.49 18 7.2 0.11 0.55 19 14 0.08 0.44 20 8.3 0.08 0.51 The "Financial Condition" column records the judgment of an expert on the financial condition of each bank. This dependent variable takes one of two possible values--weak or strong ---according to the financial condition of the bank. The predictors are two ratios used in the financial analysis of banks: TotLnsLses/Assets is the ratio of total loans and leases to total assets, and TotExp/Assets is the ratio of total expenses to total assets. The target is to use the two ratios for classifying the financial condition of a new bank. Run a logistic regression (on the entire dataset) that models the status of a bank as a function of the two financial measures provided. Specify the success class as weak (this is similar to creating a dummy that is 1 for financially weak banks and 0 otherwise), and use the default cutoff value of 0.5. a) Write the estimated equation that associates the financial condition of a bank with its two predictors in three formats: i. logit as a function of the predictors: ii. odds as a function of the predictors: iii. probability as a function of the predictors: b) Consider a new bank whose total loans and leases/assets ratio = 0.75 and total expenses/assets ratio = 0.12. From your logistic regression model, estimate the following four quantities for this bank: the logit , the odds the probability of being financially weak and the classification of the bank (use cutoff = 0.5) c) Interpret the estimated coefficient for the total loans and leases to total assets ratio (TotLns&Lses/Assets) in terms of the odds of being financially weak. d) When a bank that is in poor financial condition is misclassified as financially strong, the misclassification cost is much higher than when a financially strong bank is misclassified as weak. To minimize the expected cost of misclassification, should the cutoff value for classification (which is currently at 0.5) be increased or decreased?

Glencoe Algebra 1, Student Edition, 9780079039897, 0079039898, 2018

18th Edition

ISBN:9780079039897

Author:Carter

Publisher:Carter

Chapter10: Statistics

Section10.4: Distributions Of Data

Problem 19PFA

Related questions

Question

Transcribed Image Text:Use the data (a sample of 20 banks) given below to answer the following question(s).

financial

Obs

condition

TotCap/Assets

TotExp/Assets

TotLnsLses/ Assets

1

1

9.7

0.12

0.65

2

1

1

0.11

0.62

3

1

6.9

0.09

1.02

4

1

5.8

0.1

0.67

1

4.3

0.11

0.69

6.

1

9.1

0.13

0.74

7

1

11.9

0.1

0.79

8

1

8.1

0.13

0.63

9

9.3

0.16

0.72

10

1.1

0.16

0.57

11

11.1

0.08

0.43

12

20.5

0.12

0.8

13

9.8

0.07

0.69

14

7.9

0.08

0.53

15

9.6

0.09

0.73

16

12.5

0.09

0.3

17

18.3

0.08

0.49

18

7.2

0.11

0.55

19

14

0.08

0.44

20

8.3

0.08

0.51

The "Financial Condition" column records the judgment of an expert on the financial condition of each bank. This dependent variable takes one of two possible

values--weak or strong ---according to the financial condition of the bank. The predictors are two ratios used in the financial analysis of banks: TotLnsLses/Assets is

the ratio of total loans and leases to total assets, and TotExp/Assets is the ratio of total expenses to total assets. The target is to use the two ratios for classifying the

financial condition of a new bank.

Run a logistic regression (on the entire dataset) that models the status of a bank as a function of the two financial measures provided. Specify the success class as weak

(this is similar to creating a dummy that is 1 for financially weak banks and 0 otherwise), and use the default cutoff value of 0.5.

a) Write the estimated equation that associates the financial condition of a bank with its two predictors in three formats:

i. logit as a function of the predictors:

ii. odds as a function of the predictors:

iii. probability as a function of the predictors:

b) Consider a new bank whose total loans and leases/assets ratio = 0.75 and total expenses/assets ratio = 0.12. From your logistic regression model, estimate the

following four quantities for this bank: the logit

, the odds

the probability of

being financially weak

and the classification of the bank (use cutoff = 0.5)

c) Interpret the estimated coefficient for the total loans and leases to total assets ratio (TotLns&Lses/Assets) in terms of the odds of being financially weak.

d) When a bank that is in poor financial condition is misclassified as financially strong, the misclassification cost is much higher than when a financially strong bank is

misclassified as weak. To minimize the expected cost of misclassification, should the cutoff value for classification (which is currently at 0.5) be increased or

decreased?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Recommended textbooks for you

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill