Concept explainers

Videos

Return on Investment (ROI) Analysis

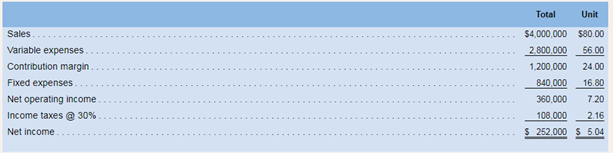

The -contribution format income statement for Huerra Company for last year is given below:

The company Lad average operating assets of $2,000,000 during the year.

Required:

1. Compute the company's return on investment (ROI) for the period using the ROI formula stated in terms of margin and turnover.

For each of the following questions, indicate whether the margin and turnover will increase, decrease, or remain unchanged as a result of the events described, and then compute the new ROE figure. Consider each question separately, starting in each case from the data used to compute the original ROI in (1) above.

2. Using Lean Production, the company is able to reduce the average level of inventory" by $400,000. (The released funds are used to pay off short-term creditors.)

3. The company achieves a cost savings of $32:000 per year by using less costly materials.

4. The company issues bonds and uses the proceeds to purchase machinery and equipment that increases average operating assets by $500:000. Interest on the bonds is $60,000 per year. Sales remain unchanged. The new, more efficient equipment reduces production costs by 520,000 per year.

5. As a result of a more intense effort by salespeople, sales are increased by 20%; operating assets remain unchanged.

6. At the beginning of the year obsolete inventory carried on the books at a cost of $40,000 is scrapped and written off as a loss.

7. At the beginning of the year the company uses $200,000 of cash (received on accounts receivable) to repurchase and retire some of its common stock.

- 1)

Return on Investment, Margin and Turnover:

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 4.5%

Explanation of Solution

- Given:

Sales = $4,000,000

Variable Expense = $2,800,000

Fixed Expenses=$840,000

Average Operating Assets = $2,000,000

- Formulae used:

- Calculations:

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 3.6%

Explanation of Solution

- Given:

Sales = $4,000,000

Variable Expense = $2,800,000

Fixed Expenses=$840,000

Average Operating Assets = $1,600,000

- Formulae used:

- Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Since the average level of inventory is reduced, the average operating assets for the year will also reduce by $400,000.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and reduces when the average operating assets decrease and turnover increases.

3)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 4.9%

Explanation of Solution

- Given: Sales = $4,000,000

Variable Expense = $3,168,000

Fixed Expenses=$840,000

Average Operating Assets = $2,000,000

- Formulae used:

- Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Since the cost savings take place for the company, the value of variable expenses will reduce $32,000.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and increases when there is a reduction in expenses.

4)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 5%

Explanation of Solution

- Given:

Sales = $4,000,000

Variable Expense = $2,780,000 [$2,800,000 - $20,000]

Fixed Expenses=$900,000 [$840,000 + $60,000]

Average Operating Assets = $2,500,000 [$2,000,000 + $500,000]

- Formulae used:

- Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Since the new plant and equipment is purchased, the average operating assets for the year will increase by $500,000.

- The cost of interest on bonds will increase the fixed expenses by $60,000 and the production cost savings will reduce variable costs by $20,000.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and increases when the average operating assets increases.

5)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 10.071%

Explanation of Solution

- Given: Sales = $4,800,000 [$4000000 + $800000]

Variable Expense = $2,800,000

Fixed Expenses=$840,000

Average Operating Assets = $2,000,000

- Formulae used:

- Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Sales increase by 20% i.e. $800,000.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and increases with an increase in the sale value.

6)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 3.92%

Explanation of Solution

- Given:

Sales = $4,000,000

Variable Expense = $2,840,000

Fixed Expenses=$840,000

Average Operating Assets = $1,960,000

- Formulae used:

Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Since the average level of inventory is scrapped, the average operating assets for the year will also reduce by $40,000 and variable expenses will increase by $40,000 to book loss on scrapping of assets.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and reduces when the average operating assets decrease and expenses increase.

7)

Return on Investment, Margin and Turnover

Return on Investment is calculated as Margin divided by Turnover. Here Margin refers to the Sales Margin and Turnover refers to the Capital Turnover Ratio.

Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

Return on Investment for the year

Answer to Problem 20P

Solution:

The Return on Investment for the year is 4.05%

Explanation of Solution

- Given:

Sales = $4,000,000

Variable Expense = $2,800,000

Fixed Expenses=$840,000

Average Operating Assets = $1,800,000

- Formulae used:

Calculations:

- Margin is the percentage of Profit earned by an entity in a given reporting period. Profit is calculated as Revenues less Cost of Goods Sold and Indirect Expenses.

- Margin is Profit expressed in terms of Sales as a percentage.

- Turnover is the capital turnover ratio. This is calculated by dividing the sales by the average operating assets for the year.

- Return on Investment is calculated as Margin divided by Turnover.

- Return on Investment calculations are important from a business standpoint as they help in evaluation of new investment proposals, make or buy decisions, capital expenditure projects and whether to invest in a particular company or not.

- Since cash which is received from accounts receivable, is used to purchase common stock, the value of average operating assets will reduce

- Hence there is no impact on the balance of average operating assets and return on investment.

Hence it can be seen that the Return on Investment is calculated as Margin divided by Turnover and reduces when the average operating assets decrease.

Want to see more full solutions like this?

Chapter 10 Solutions

Introduction To Managerial Accounting

- During the current year, Sokowski Manufacturing earned income of $350,000 from total sales of $5,500,000 and average capital assets of $12,000,000. A. Based on this information, calculate asset turnover. B. Using the sales margin from the previous exercise, what is the total ROI for the company during the current year?arrow_forwardThe following selected data pertain to the Argent Division for last year: Required: 1. How much is the residual income? 2. How much is the return on investment? (Rounded to four significant digits.)arrow_forwardThe income statement comparison for Rush Delivery Company shows the income statement for the current and prior year. A. Determine the operating income (loss) (dollars) for each year. B. Determine the operating income (percentage) for each year. C. The company made a strategic decision to invest in additional assets in the current year. These amounts are provided. Using the total assets amounts as the investment base, calculate the ROI. Was the decision to invest additional assets in the company successful? Explain. D. Assuming an 8% cost of capital, calculate the RI for each year. Explain how this compares to your findings in part C.arrow_forward

- The income statement comparison for Forklift Material Handling shows the income statement for the current and prior year. A. Determine the operating income (loss) (dollars) for each year. B. Determine the operating income (percentage) for each year. C. The company made a strategic decision to invest in additional assets in the current year. These amounts are provided. Using the total assets amounts as the investment base, calculate the return on investment. Was the decision to invest additional assets in the company successful? Explain. D. Assuming an 8% cost of capital, calculate the residual income for each year. Explain how this compares to your findings in part C.arrow_forwardForchen, Inc., provided the following information for two of its divisions for last year: Required: 1. For the Small Appliances Division, calculate: a. Average operating assets b. Margin c. Turnover d. Return on investment (ROI) 2. For the Cleaning Products Division, calculate: a. Average operating assets b. Margin c. Turnover d. Return on investment (ROI) 3. What if operating income for the Small Appliances Division was 2,000,000? How would that affect average operating assets? Margin? Turnover? ROI? Calculate any changed ratios (round to four significant digits).arrow_forwardContribution margin, break-even sales, cost-volume-profit chart, margin of safety, and operating leverage Belmain Co. expects to maintain the same inventories at the end of 20Y7 as at the beginning of the year. The total of all production costs for the year is therefore assumed to be equal to the cost of goods sold. With this in mind, the various department heads were asked to submit estimates of the costs for their departments during the year. A summary report of these estimates is as follows: It is expected that 12,000 units will be sold at a price of 240 a unit. Maximum sales within the relevant range are 18,000 units. Instructions 1. Prepare an estimated income statement for 20Y7. 2. What is the expected contribution margin ratio? 3. Determine the break-even sales in units and dollars. 4. Construct a cost-volume-profit chart indicating the break-even sales. 5. What is the expected margin of safety in dollars and as a percentage of sales? (Round to one decimal place.) 6. Determine the operating leverage.arrow_forward

- During the current year, Plainfield Manufacturing earned income of $845,000 from total sales of $9,350,000 and average capital assets of $13,500,000. Using the sales margin from the previous exercise, what is the total ROI for the company during the current year?arrow_forwardCost-Volume-Profit, Margin of Safety Victoria Company produces a single product. Last years income statement is as follows: Required: 1. Compute the break-even point in units and sales dollars calculated using the break-even units. 2. What was the margin of safety for Victoria last year in sales dollars? 3. Suppose that Victoria is considering an investment in new technology that will increase fixed cost by 250,000 per year but will lower variable costs to 45% of sales. Units sold will remain unchanged. Prepare a budgeted income statement assuming that Victoria makes this investment. What is the new break-even point in sales dollars, assuming that the investment is made?arrow_forwardA Using Common Size Statements The following income statement and vertical analysis data are available for Riley Manufacturing: Required: 1. CONCEPTUAL CONNECTION Suggest why net income declined from $273,200 to $41,600 while the cost of goods sold percentage decreased each year and selling and administrative expenses remained nearly constant. 2. CONCEPTUAL CONNECTION Determine what could cause sales to decline while the gross margin percentage increases.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub