Managerial Accounting: The Cornerstone of Business Decision-Making

7th Edition

ISBN: 9781337115773

Author: Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 10, Problem 44E

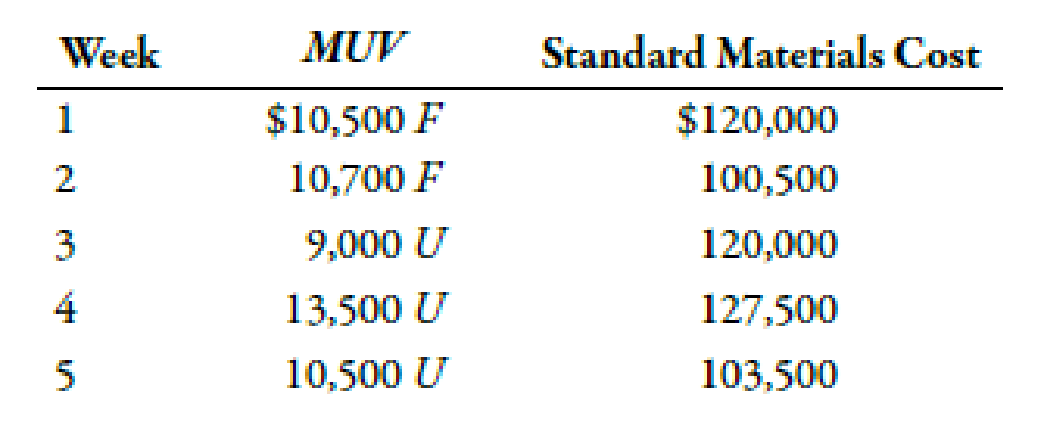

Sommers Company uses the following rule to determine whether materials usage variances should be investigated: A materials usage variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10% of the

Required:

- 1. Using the rule provided, identify the cases that will be investigated.

- 2. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of an unfavorable materials usage variance is the use of lower-quality materials than are normally used. Who is responsible? What corrective action would likely be taken?

- 3. CONCEPTUAL CONNECTION Suppose investigation reveals that the cause of a significant unfavorable materials usage variance is attributable to a new approach to manufacturing that takes less labor time but causes more material waste. Examination of the labor efficiency variance reveals that it is favorable and larger than the unfavorable materials usage variance. Who is responsible? What action should be taken?

Expert Solution & Answer

Trending nowThis is a popular solution!

Chapter 10 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

Ch. 10 - Discuss the dirrerence between budgets and...Ch. 10 - Describe the relationship that unit standards have...Ch. 10 - Why is historical experience often a poor basis...Ch. 10 - Prob. 4DQCh. 10 - Explain why standard costing systems adopted.Ch. 10 - How does standard costing improve the control...Ch. 10 - Discuss the differences among actual costing,...Ch. 10 - Prob. 8DQCh. 10 - The budget variance for variable production costs...Ch. 10 - When should a standard cost variance be...

Ch. 10 - What are control limits, and how are they set?Ch. 10 - Explain why the materials price variance is often...Ch. 10 - The materials usage variance is always the...Ch. 10 - The labor rate variance is never controllable. Do...Ch. 10 - Prob. 15DQCh. 10 - What is kaizen costing? On which part of the value...Ch. 10 - What is target costing? Describe how costs are...Ch. 10 - Prob. 18DQCh. 10 - The variable overhead efficiency variance has...Ch. 10 - Describe the difference between the variable...Ch. 10 - What is the cause of an unfavorable volume...Ch. 10 - Does the volume variance convey any meaningful...Ch. 10 - Which do you think is more important for control...Ch. 10 - Prob. 1MCQCh. 10 - A currently attainable standard is one that a....Ch. 10 - An ideal standard is one that a. uses only...Ch. 10 - The underlying details for the standard cost per...Ch. 10 - The standard quantity of materials allowed is...Ch. 10 - The standard direct labor hours allowed is...Ch. 10 - Investigating variances from standard is a. always...Ch. 10 - Prob. 8MCQCh. 10 - The materials price variance is usually computed...Ch. 10 - Responsibility for the materials usage variance is...Ch. 10 - Responsibility for the labor rate variance...Ch. 10 - Responsibility for the labor efficiency variance...Ch. 10 - (Appendix 10A) Which of the following items...Ch. 10 - (Appendix 10A) Which of the following is true...Ch. 10 - The total variable overhead variance is the...Ch. 10 - A variable overhead spending variance can occur...Ch. 10 - The total variable overhead variance can be...Ch. 10 - The total fixed overhead variance is a. the...Ch. 10 - The total fixed overhead variance can be expressed...Ch. 10 - An unfavorable volume variance can occur because...Ch. 10 - Prob. 21BEACh. 10 - Control Limits During the last 6 weeks, the actual...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Rath Company showed the following information for...Ch. 10 - Variable Overhead Spending and Efficiency...Ch. 10 - Performance Report for Variable Variances Humo...Ch. 10 - Total Fixed Overhead Variance Bradshaw Company...Ch. 10 - Fixed Overhead Spending and Volume Variances,...Ch. 10 - Prob. 32BEBCh. 10 - Control Limits During the last 6 weeks, the actual...Ch. 10 - Prob. 34BEBCh. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Use the following information to complete Brief...Ch. 10 - Mulliner Company showed the following information...Ch. 10 - Variable Overhead Spending and Efficiency...Ch. 10 - Performance Report for Variable Variances Potter...Ch. 10 - Bulger Company provided the following data:...Ch. 10 - Fixed Overhead Spending and Volume Variances,...Ch. 10 - Standard Quantities of Labor and Materials...Ch. 10 - Sommers Company uses the following rule to...Ch. 10 - Use the following information for Exercises 10-45...Ch. 10 - Refer to the information for Cinturon Corporation...Ch. 10 - Refer to the information for Cinturon Corporation...Ch. 10 - Materials Variances Manzana Company produces apple...Ch. 10 - Labor Variances Verde Company produces wheels for...Ch. 10 - At the beginning of the year, Craig Company had...Ch. 10 - Jackie Iverson was furious. She was about ready to...Ch. 10 - 10-52 Materials and Labor Variances Refer to the...Ch. 10 - Refer to the information for Deporte Company...Ch. 10 - Esteban Products produces instructional aids,...Ch. 10 - Escuchar Products, a producer of DVD players, has...Ch. 10 - Use the following information for Exercises 10-56...Ch. 10 - Refer to the information for Rostand Inc. above....Ch. 10 - At the beginning of the year, Lopez Company had...Ch. 10 - Zepol Company is planning to produce 600,000 power...Ch. 10 - Last year, Gladner Company had planned to produce...Ch. 10 - Anker Company had the data below for its most...Ch. 10 - Cabanarama Inc. designs and manufactures...Ch. 10 - Basuras Waste Disposal Company has a long-term...Ch. 10 - Tom Belford and Tony Sorrentino own a small...Ch. 10 - Mantenga Company provides routine maintenance...Ch. 10 - Buenolorl Company produces a well-known cologne....Ch. 10 - The management of Golding Company has determined...Ch. 10 - Phono Company manufactures a plastic toy cell...Ch. 10 - Botella Company produces plastic bottles. The unit...Ch. 10 - The Lubbock plant of Morrils Small Motor Division...Ch. 10 - Moleno Company produces a single product and uses...Ch. 10 - The Lubbock plant of Morrils Small Motor Division...Ch. 10 - Extrim Company produces monitors. Extrims plant in...Ch. 10 - Lynwood Company produces surge protectors. To help...Ch. 10 - Shumaker Company manufactures a line of high-top...Ch. 10 - Paul Golding and his wife, Nancy, established...Ch. 10 - Prob. 79CCh. 10 - Prob. 1MTCCh. 10 - The Two Cost Systems Sacred Heart Hospital (SHH)...Ch. 10 - Prob. 3MTCCh. 10 - Prob. 4MTCCh. 10 - The Two Cost Systems Sacred Heart Hospital (SHH)...Ch. 10 - Prob. 6MTCCh. 10 - Prob. 7MTCCh. 10 - Prob. 8MTCCh. 10 - Prob. 9MTCCh. 10 - Sacred Heart Hospital (SHH) faces skyrocketing...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of 12,000 or 10 percent of the standard labor cost. Reports for the past five weeks provided the following information: Required: 1. Using the rule provided, identify the cases that will be investigated. 2. Suppose that investigation reveals that the cause of an unfavorable direct labor efficiency variance is the use of lower quality direct materials than are usually used. Who is responsible? What corrective action would likely be taken? 3. Suppose that investigation reveals that the cause of a significant favorable direct labor efficiency variance is attributable to a new approach to manufacturing that takes less labor time but causes more direct materials waste. Upon examining the direct materials usage variance, it is discovered to be unfavorable, and it is larger than the favorable direct labor efficiency variance. Who is responsible? What action should be taken? How would your answer change if the unfavorable variance were smaller than the favorable?arrow_forwardThe management of Golding Company has determined that the cost to investigate a variance produced by its standard cost system ranges from 2,000 to 3,000. If a problem is discovered, the average benefit from taking corrective action usually outweighs the cost of investigation. Past experience from the investigation of variances has revealed that corrective action is rarely needed for deviations within 8% of the standard cost. Golding produces a single product, which has the following standards for materials and labor: Actual production for the past 3 months follows, with the associated actual usage and costs for materials and labor. There were no beginning or ending raw materials inventories. Required: 1. What upper and lower control limits would you use for materials variances? For labor variances? 2. Compute the materials and labor variances for April, May, and June. Identify those that would require investigation by comparing each variance to the amount of the limit computed in Requirement 1. Compute the actual percentage deviation from standard. Round all unit costs to four decimal places. Round variances to the nearest dollar. Round variance rates to three decimal places so that percentages will show to one decimal place. 3. CONCEPTUAL CONNECTION Let the horizontal axis be time and the vertical axis be variances measured as a percentage deviation from standard. Draw horizontal lines that identify upper and lower control limits. Plot the labor and material variances for April, May, and June. Prepare a separate graph for each type of variance. Explain how you would use these graphs (called control charts) to assist your analysis of variances.arrow_forwardIn all of the exercises involving variances, use F and U to designate favorable and unfavorable variances, respectively. E8-1 through E8-5 use the following data: The standard operating capacity of Tecate Manufacturing Co. is 1,000 units. A detailed study of the manufacturing data relating to the standard production cost of one product revealed the following: 1. Two pounds of materials are needed to produce one unit. 2. Standard unit cost of materials is 8 per pound. 3. It takes one hour of labor to produce one unit. 4. Standard labor rate is 10 per hour. 5. Standard overhead (all variable) for this volume is 4,000. Each case in E8-1 through E8-5 requires the following: a. Set up a standard cost summary showing the standard unit cost. b. Analyze the variances for materials and labor. c. Make journal entries to record the transfer to Work in Process of: 1. Materials costs 2. Labor costs 3. Overhead costs (When making these entries, include the variances.) d. Prepare the journal entry to record the transfer of costs to the finished goods account. Standard unit cost; variance analysis; journal entries 1,000 units were started and finished. Case 1: All prices and quantities for the cost elements are standard, except for materials cost, which is 8.50 per pound. Case 2: All prices and quantities for the cost elements are standard, except that 1,900 lb of materials were used.arrow_forward

- Kavallia Company set a standard cost for one item at 328,000; allowable deviation is 14,500. Actual costs for the past six months are as follows: Required: 1. Calculate the variance from standard for each month. Which months should be investigated? 2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or 14,500. Now which months should be investigated?arrow_forwardMarten Company has a cost-benefit policy to investigate any variance that is greater than 1,000 or 10% of budget, whichever is larger. Actual results for the previous month indicate the following: The company should investigate: a. neither the materials variance nor the labor variance. b. the materials variance only. c. the labor variance only. d. both the materials variance and the labor variance.arrow_forwardUsing variance analysis and interpretation Last year, Wrigley Corp. adopted a standard cost system. Labor standards were set on the basis of time studies and prevailing wage rates. Materials standards were determined from materials specifications and the prices then in effect. On June 30, the end of the current fiscal year, a partial trial balance revealed the following: Standards set at the beginning of the year have remained unchanged. All inventories are priced at standard cost. What conclusions can be drawn from each of the four variances shown in Wrigleys trial balance?arrow_forward

- Cortez Manufacturing, Inc. has the following flexible budget formulas and amounts: Actual results for May for the production and sale of 5,000 units were as follows: Prepare a performance report for May that includes the identification of the favorable and unfavorable variances.arrow_forwardRefer to the information for Cinturon Corporation on the previous page. Required: 1. Break down the total variance for materials into a price variance and a usage variance using the columnar and formula approaches. 2. CONCEPTUAL CONNECTION Suppose the Boise plant manager investigates the materials variances and is told by the purchasing manager that a cheaper source of leather strips had been discovered and that this is the reason for the favorable materials price variance. Quite pleased, the purchasing manager suggests that the materials price standard be updated to reflect this new, less expensive source of leather strips. Should the plant manager update the materials price standard as suggested? Why or why not?arrow_forwardUsing variance analysis and interpretation Last year, Endicott Corp. adopted a standard cost system. Labor standards were set on the basis of time studies and prevailing wage rates. Materials standards were determined from materials specifications and the prices then in effect. On June 30, the end of the current fiscal year, a partial trial balance revealed the following: Standards set at the beginning of the year have remained unchanged. All inventories are priced at standard cost. What conclusions can be drawn from each of the four variances shown in Endicotts trial balance?arrow_forward

- Warner Company has the following data for the past year: Warner uses the overhead control account to accumulate both actual and applied overhead. Required: 1. Calculate the overhead variance for the year and close it to cost of goods sold. 2. Assume the variance calculated is material. After prorating, close the variances to the appropriate accounts and provide the final ending balances of these accounts. 3. What if the variance is of the opposite sign calculated in Requirement 1? Provide the appropriate adjusting journal entries for Requirements 1 and 2.arrow_forwardAs part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracers monthly operating budgets. The following direct labor standard was established for one of Tracers products, effective June 1, 2012, the beginning of the fiscal year: The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the companys skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year. For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams. Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials. Required: 1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units. 2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units? 3. Determine the amount that should be included in Tracers January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. (CMA adapted)arrow_forwardRefer to the information for Cinturon Corporation on the previous page. Required: 1. Break down the total variance for labor into a rate variance and an efficiency variance using the columnar and formula approaches. 2. CONCEPTUAL CONNECTION As part of the investigation of the unfavorable variances, the plant manager interviews the production manager. The production manager complains strongly about the quality of the leather strips. He indicates that the strips are of lower quality than usual and that workers have to be more careful to avoid a belt with cracks and more time is required. Also, even with extra care, many belts have to be discarded and new ones produced to replace the rejects. This replacement work has also produced some overtime demands. What corrective action should the plant manager take?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

What is variance analysis?; Author: Corporate finance institute;https://www.youtube.com/watch?v=SMTa1lZu7Qw;License: Standard YouTube License, CC-BY