Concept explainers

Videos

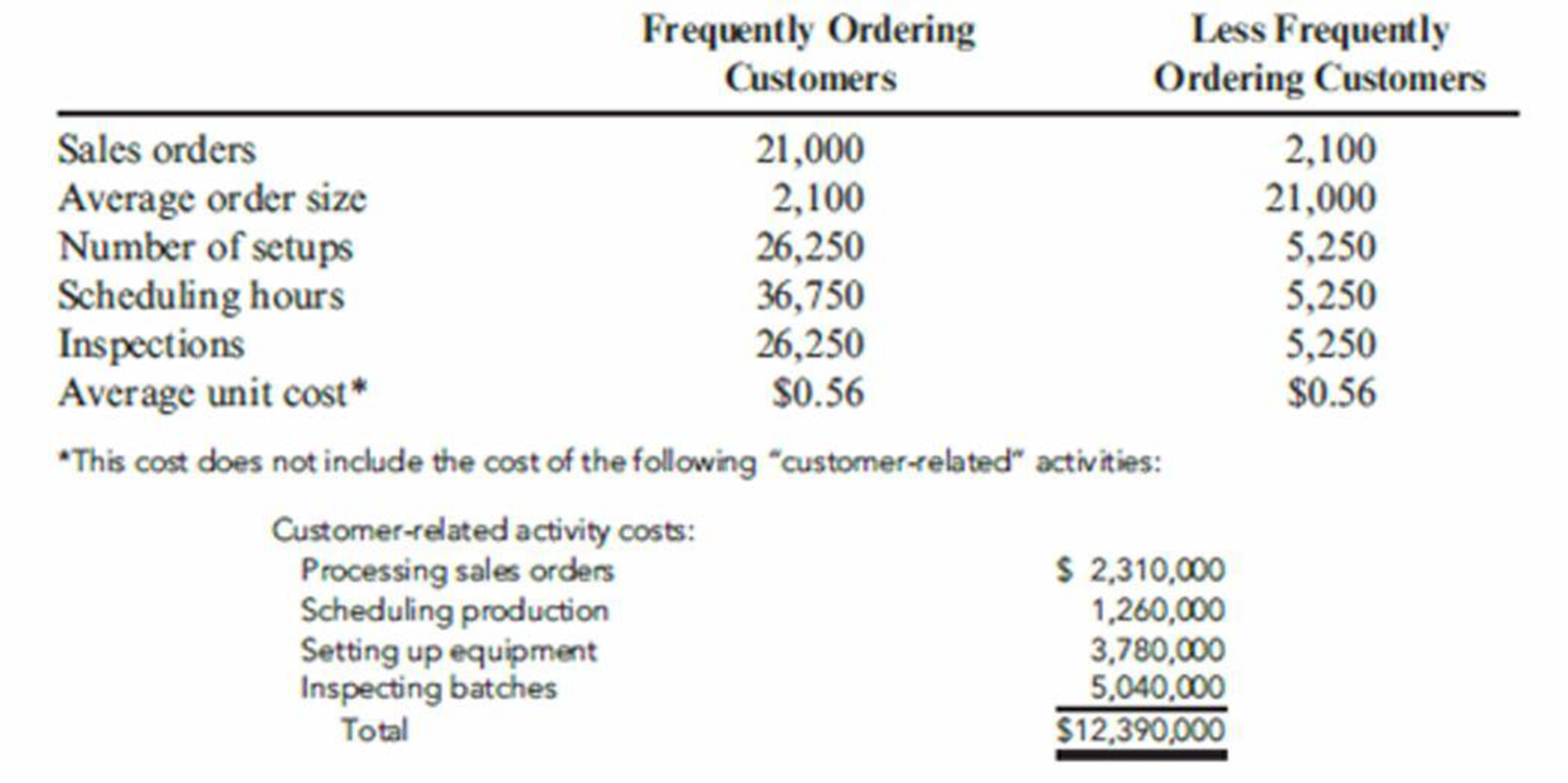

Assign the customer-related activity costs to each customer type using activity rates. Now calculate the profitability of each customer category. As a manager, how would you use this information?

Emery Company sells small machine parts to heavy equipment manufacturers for an average price of $1.05 per part. There are two types of customers: those who place small, frequent orders and those who place larger, less frequent orders. Each time an order is placed and processed, a setup is required. Scheduling is also needed to coordinate the many different orders that come in and place demands on the plant’s manufacturing resources. Emery also inspects a sample of the products each time a batch is produced to ensure that the customer’s specifications have been met Inspection takes essentially the same time regardless of the type of part being produced. Emery’s Cost Accounting Department has provided the following budgeted data for customer-related activities and costs (the amounts expected for the coming year):

Required:

- 1. Assign the customer-related activity costs to each category of customers in proportion to the sales revenue earned by each customer type. Calculate the profitability of each customer type. Discuss the problems with this measure of customer profitability.

Trending nowThis is a popular solution!

Chapter 11 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Assume you are the warehouse manager for Vinnies Vinyls, a multi-location business specializing in vinyl records. Vinniess operates under a cost-based transfer structure and the warehouse supplies all stores with the records. The stores can purchase records only from the warehouse, and the warehouse can only sell to Vinnies stores. The manager of the West store has some concerns relating to the stores financial performance and has asked for your help analyzing transfer costs. After calculating the operating income in dollars and the operating income percent, analyze the following financial information to determine costs that may need further investigation. (Hint: it may be helpful to perform a vertical analysis.)arrow_forwardVentana Window and Wall Treatments Company provides draperies, shades, and various window treatments. Ventana works with the customer to design the appropriate window treatment, places the order, and installs the finished product. Direct materials and direct labor costs are easy to trace to the jobs. Ventanas income statement for last year is as follows: Ventana wants to find a markup on cost of goods sold that will allow them to earn about the same amount of profit on each job as was earned last year. Required: 1. What is the markup on cost of goods sold (COGS) that will maintain the same profit as last year? (Round the percentage to two significant digits.) 2. A customer orders draperies and shades for a remodeling job. The job will have the following costs: What is the price that Ventana will quote given the markup percentage calculated in Requirement 1? (Round the price to the nearest dollar.) 3. What if Ventana wants to calculate a markup on direct materials cost, since it is the largest cost of doing business? What is the markup on direct materials cost that will maintain the same profit as last year? (Round the percentage to two significant digits.) What is the bid price Ventana will use for the job given in Requirement 2 if the markup percentage is calculated on the basis of direct materials cost? (Round to the nearest dollar.)arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forward

- Discuss how, as warehouse manager for Vinnies Vinyls, you view the different rate of allocated costs the warehouse is being charged compared to the West store. Describe the implications of this. What steps could you take to solve this discrepancy? What alternatives would you consider, assuming management is willing to consider making changes in the rate?arrow_forwardHenrys Cafe is a local restaurant that is growing quickly. While the company does not yet have a balanced scorecard, Henry has mentioned that being efficient in producing meals is a high priority of his business and appears to be a significant driver of profits. Henry tells you he gathers the following data: sales, cost of labor, employee turnover, labor hours, cost of ingredients, overhead costs, average training hours per employee, number of erroneous meals prepared, the time when orders were made (e.g., at 12:43 PM), the time when orders were delivered, and number of customers per day. a. Under which performance perspective on the balanced scorecard should Henrys strategic objective to efficiently produce meals be placed? b. Based on the data collected, what are at least three performance metrics Henry could develop to measure his strategic objective to efficiently produce meals? c. Identify whether the performance metrics you suggested in part (b) are leading or lagging indicators relative to a performance metric total cost of production per meal.arrow_forwardKelson Sporting Equipment, Inc., makes two types of baseball gloves: a regular model and a catchers model. The firm has 900 hours of production time available in its cutting and sewing department, 300 hours available in its finishing department, and 100 hours available in its packaging and shipping department. The production time requirements and the profit contribution per glove are given in the following table: Assuming that the company is interested in maximizing the total profit contribution, answer the following: a. What is the linear programming model for this problem? b. Develop a spreadsheet model and find the optimal solution using Excel Solver. How many of each model should Kelson manufacture? c. What is the total profit contribution Kelson can earn with the optimal production quantities? d. How many hours of production time will be scheduled in each department? e. What is the slack time in each department?arrow_forward

- Moss Manufacturing produces several types of bolts. The products are produced in batches according to customer order. Although there are a variety of bolts, they can be grouped into three product families. The number of units sold is the same for each family. The selling prices for the three families range from 0.50 to 0.80 per unit. Because the product families are used in different kinds of products, customers also can be grouped into three categories, corresponding to the product family they purchase. Historically, the costs of order entry, processing, and handling were expensed and not traced to individual products. These costs are not trivial and totaled 6,300,000 for the most recent year. Furthermore, these costs had been increasing over time. Recently, the company had begun to emphasize a cost reduction strategy; however, any cost reduction decisions had to contribute to the creation of a competitive advantage. Because of the magnitude and growth of order-filling costs, management decided to explore the causes of these costs. They discovered that order-filling costs were driven by the number of customer orders processed. Further investigation revealed the following cost behavior: Step-fixed cost component: 70,000 per step; 2,000 orders define a step Variable cost component: 28 per order Moss currently has sufficient steps to process 100,000 orders. The expected customer orders for the year total 140,000. The expected usage of the order-filling activity and the average size of an order by product family are as follows: As a result of the cost behavior analysis, the marketing manager recommended the imposition of a charge per customer order. The president of the company concurred. The charge was implemented by adding the cost per order to the price of each order (computed using the projected ordering costs and expected orders). This ordering cost was then reduced as the size of the order increased and eliminated as the order size reached 2,000 units. (The marketing manager indicated that any penalties imposed for orders greater than this size would lose sales from some of the smaller customers.) Within a short period of communicating this new price information to customers, the average order size for all three product families increased to 2,000 units. Required: 1. Moss traditionally has expensed order-filling costs (following GAAP guidelines). Under this approach, how much cost is assigned to customers? Do you agree with this practice? Explain. 2. Consider the following claim: by expensing the order-filling costs, all products were undercosted; furthermore, products ordered in small batches are significantly undercosted. Explain, with supporting computations where possible. Explain how this analysis also reveals the costs of various customer categories. 3. Calculate the reduction in order-filling costs produced by the change in pricing strategy. (Assume that resource spending is reduced as much as possible and that the total units sold remain unchanged.) Explain how exploiting customer linkages produced this cost reduction. Moss also noticed that other activity costs, such as those for setups, scheduling, and materials handling costs, were reduced significantly as a result of this new policy. Explain this outcome, and discuss its implications. 4. Suppose that one of the customers complains about the new pricing policy. This buyer is a lean, JIT firm that relies on small, frequent orders. In fact, this customer accounted for 30 percent of the Family A orders. How should Moss deal with this customer? 5. One of Mosss goals is to reduce costs so that a competitive advantage might be created. Describe how the management of Moss might use this outcome to help create a competitive advantage.arrow_forwardRizzo Goal Inc. produces and sells hockey equipment, often custom made for online orders. The company has the following performance metrics on its balanced scorecard: days from ordered to delivered, number of shipping errors, customer retention rate, and market share. A measure map illustrates that the days from ordered to delivered and the number of shipping errors are both expected to directly affect the customer retention rate, which affects market share. Additional internal analysis finds that: Every shipping error over three shipping errors per month reduces the customer retention rate by 1.5%. On average, each day above three days from ordered to delivered yields a reduction in the customer retention rate of 1%. Each day before three days from order to delivery yields an increase in the customer retention rate of 1%, on average. Rizzo Goal Inc.s current customer retention rate is 60%. The company estimates that for every 1% increase or decrease in the customer retention rate, market share changes 0.5% in the same direction. Rizzo Goal Inc.s current market share is 21.4%. Ignoring any other factors, if the company has six shipping errors this month and an average of 3.5 days from ordered to delivered, determine (a) the new customer retention rate and (b) the new market share that Rizzo Goal Inc. expects to have.arrow_forwardStan is opening a coffee shop next to Big State University. He knows that controlling his costs will be important to the success of the shop. He will not be able to work all the hours the shop is open, so the employees will need some guidelines to perform their jobs correctly. After talking to an accounting professor, he decides he needs a standard cost system for his shop. Describe the process Stan should follow in setting his standards for materials and labor.arrow_forward

- Larsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardYou are a management accountant for Time Treasures Company, whose company has recently signed an outsourcing agreement with Spotless. Inc., a janitorial service company. Spotless will provide all of Time Treasures janitorial services, including sweeping floors, hauling trash, washing windows, stocking restrooms, and performing minor repairs. Time Treasures will be billed at an hourly rate based on the type of service performed. The work of common laborers (sweeping, hauling trash) is to be billed at $8 per hour. More skilled (repairs) and more dangerous work (washing outside windows on the 23rd floor) are to be billed at $18 per hour. Supervisory time is to be billed at $20 per hour. Spotless will submit monthly invoices, which will show the number and types of hours for which Time Treasures is being charged. The outsourcing contract is simple and straightforward. A. What are some of the internal control problems you foresee as a result of our sourcing the janitorial service with this contract? B. Explain recommendations to control risk that would you suggest after reviewing the contract.arrow_forwardCommunication The controller of New Wave Sounds Inc. prepared the following product profitability report for management, using activity-based costing methods for allocating both the factory overhead and the marketing expenses. As such, the controller has confidence in the accuracy of this report. In addition, the controller interviewed the vice president of marketing, who provided the following insight into the companys three products: The home theater speakers are an older product that is highly recognized in the marketplace. The wireless speakers are a new product that was just recently launched. The wireless headphones are a new technology that has no competition in the marketplace, and it is hoped that they will become an important future addition to the companys product portfolio. Initial indications are that the product is well received by customers. The controller believes that the manufacturing costs for all three products are in line with expectations. Based on the information provided: 1. Calculate the ratio of gross profit to sales and the ratio of operating income to sales for each product. 2. Write a brief (one-page) memo using the product profitability report and the calculations in (a) to make recommendations to management with respect to strategies for the three products.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning