Videos

Financial Reporting of

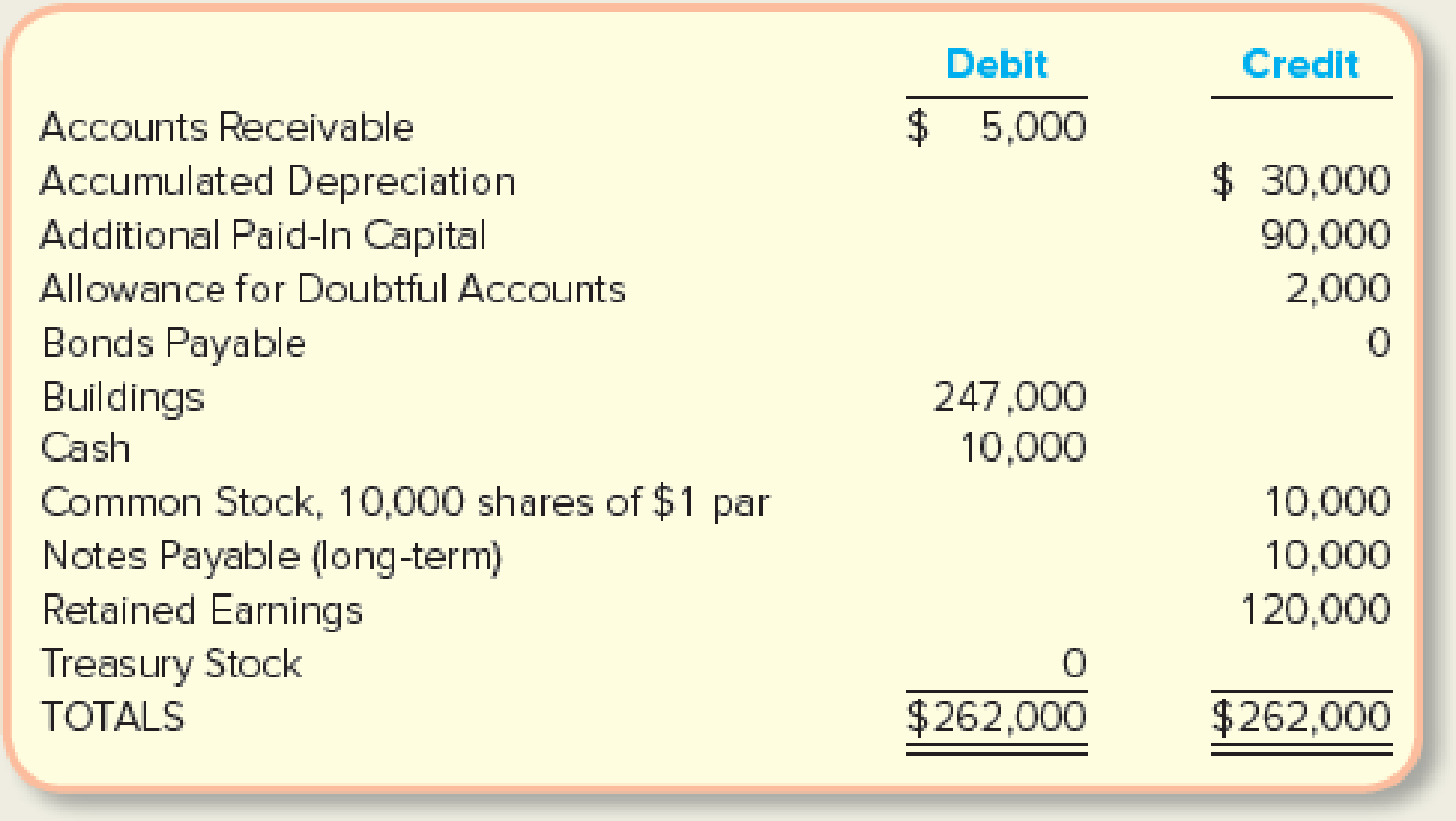

American Laser, Inc., reported the following account balances on January 1.

The company entered into the following transactions during the year.

| Jan. 15 | Issued 5,000 shares of $1 par common stock for $50,000 cash. |

| Jan. 31 | Collected $3,000 from customers on account. |

| Feb. 15 | Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. |

| Mar. 15 | Reissued 2,000 shares of |

| Aug. 15 | Reissued 600 shares of treasury stock for $4,600 cash. |

| Sept. 15 | Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. |

| Oct. 1 | Issued 100, 10-year, $1,000 bonds, at a quoted |

| Oct. 3 | Wrote off a $2,000 balance due from a customer who went bankrupt. |

| Dec. 29 | Recorded $230,000 of service revenue, all of which was collected in cash. |

| Dec. 30 | Paid $200,000 cash for this year’s wages through December 31. Ignore payroll taxes and payroll deductions. |

| Dec. 31 | Calculated $10,000 of depreciation for the year to be recorded. (Ignore accrual adjustments for interest and income taxes.) |

Required:

- 1. Analyze the effects of each transaction on total assets, liabilities, and stockholders’ equity.

- 2. Prepare journal entries to record each transaction.

- 3. Enter the January 1 balances into T-accounts,

post the journal entries from requirement 2, and determine ending balances. - 4. Prepare a closing

journal entry for the income statement accounts, assuming the events on December 29–31 were the only transactions to affect income statement accounts. - 5. Prepare the closing entry for Dividends.

- 6. Prepare a classified balance sheet at December 31.

- 7. Calculate the debt-to-assets ratio at January 1 and December 31. Does the company rely more (or less) on debt financing at the end of the year than at the beginning of the year?

1.

Analyze the effect of each transaction on total assets, liabilities and stockholder’s equity.

Explanation of Solution

Accounting equation:

Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

Analyze the effect of each transaction on total assets, liabilities and stockholder’s equity as follows:

| Date of Transaction | Balance Sheet | ||

| Assets ($) | Liabilities ($) | Stockholder’s Equity ($) | |

| January 15 | Cash | NE |

Common Stock Additional paid –in capital |

| January 31 |

Cash+3,000 AR-3,000 | NE | NE |

| February 15 | Cash | NE | Treasury stock ( |

| March 15 | Cash | NE |

Treasury stock ( Additional paid –in capital |

| August 15 | Cash | NE |

Treasury stock ( Additional paid –in capital |

| September 15 | NE |

Dividends payable | Dividends ( |

| October 1 | Cash |

Bonds payable Premium on bonds payable | |

| October 3 |

AR AFDA | NE | NE |

| December 29 | Cash +230,000 | NE | Service Revenue+230,000 |

| December 30 | Cash +230,000 | NE | Salaries and Wages Expense (+E) -200,000 |

| December 31 | Accumulated depreciation -10,000 | NE | Depreciation Expense (+E) -10,000 |

(Table 1)

Note:

- NE: Denotes increase in the value

- AR: Accounts Receivable

- AFDA: Allowance for Doubtful Accounts (

2.

Prepare journal entries to record each transaction.

Explanation of Solution

Prepare journal entries to record each transaction as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January 15 | Cash | 50,000 | |

| Common stock | 5,000 | ||

| Additional paid –in capital | 45,000 | ||

| (To record the issuance of common stock) | |||

| January 31 | Cash | 3,000 | |

| Accounts Receivable | 3,000 | ||

| (To record the cash received for customers) | |||

| February 15 | Treasury stock | 33,000 | |

| Cash | 33,000 | ||

| (To record the repurchase of common stock into treasury stock ) | |||

| March 15 | Cash | 24,000 | |

| Treasury Stock(2) | 22,000 | ||

| Additional paid –in capital | 2,000 | ||

| (To record the reissuance of treasury stock) | |||

| August 15 | Cash | 4,600 | |

| Additional paid-in capital | 2,000 | ||

| Treasury stock(3) | 6,600 | ||

| (To record the reissuance of 600 shares of treasury stock) | |||

| September 15 | Dividends (5) | 14,600 | |

| Dividends Payable | 14,600 | ||

| (To record the sale of merchandise on account) | |||

| October 1 | Cash(6) | 101,000 | |

| Bonds Payable (7) | 100,000 | ||

| Premium on bonds payable | 1,000 | ||

| (To record the issuance of bonds at a quoted bond price $101) | |||

| October 3 | Allowance for doubtful accounts | 2,000 | |

| Accounts Receivable | 2,000 | ||

| (To record the written off balance due from customer) | |||

| December 29 | Cash | 230,000 | |

| Service Revenue | 230,000 | ||

| (To record the service revenue earned) | |||

| December 30 | Salaries and Wages Expense | 200,000 | |

| Cash | 200,000 | ||

| (To record the payment of wages expenses) | |||

| December 31 | Depreciation Expense | 10,000 | |

| Accumulated Depreciation | 10,000 | ||

| (To record the depreciation expenses) | |||

Table (2)

Working notes (1):

Working notes (2):

Working notes (3):

Working notes (4):

Working notes (5):

Working notes (6):

Working notes (7):

3.

Record the January 1 balance in the T-accounts and post the journal entries to the T-accounts.

Explanation of Solution

Record the January 1 balance in the T-accounts and post the journal entries to the T-accounts as follows:

|

Cash (A) | |||

| Bal | 10,000 | ||

| 15-Jan | 50,000 | 33,000 | 15-Feb |

| 31-Jan | 3,000 | 200,000 | 30-Dec |

| 15-Mar | 24,000 | ||

| 15-Aug | 4,600 | ||

| 1- Oct | 101,000 | ||

| 29-Dec | 230,000 | ||

| 189,600 | |||

| Accounts Receivable (A) | |||

| Bal. | 5,000 | 3,000 | 31-Jan |

| 2,000 | 3-Oct | ||

| 0 | |||

| Buildings | |||

| Bal. | 247,000 | ||

| 247,000 | |||

| Allowance for Doubtful Accounts (xA) | |||

| 3-Oct | 2,000 | 2,000 | Bal. |

| 0 | |||

| Accumulated Dep.–Building(xA) | |||

| 30,000 | Bal. | ||

| 30,000 | |||

| Dividends Payable (L) | |||

| 0 | Bal. | ||

| 14,600 | 15-Sep | ||

| 14,600 | |||

| Notes Payable (L) | |||

| 10,000 | Bal. | ||

| 10,000 | |||

| Bonds Payable (L) | |||

| 0 | Bal. | ||

| 100,000 | 1-Oct | ||

| 100,000 | |||

| Premium on Bonds Payable (-L) | |||

| 0 | Bal. | ||

| 1,000 | 1-Oct | ||

| 1,000 | |||

| Common Stock (SE) | |||

| 10,000 | Bal. | ||

| 5,000 | 15-Jan | ||

| 15,000 | |||

| Additional Paid-In Capital (SE) | |||

| 90,000 | Bal. | ||

| 45,000 | 15-Jan | ||

| 15-Aug | 2,000 | 2,000 | 15-Mar |

| 135,000 | |||

| Treasury Stock (xSE) | |||

| Bal. | 0 | ||

| 15-Feb | 33,000 | 22,000 | 15-Mar |

| 6,600 | 15-Aug | ||

| 4,400 | |||

| Dividends (D) | |||

| Bal. | 0 | ||

| 15-Sep | 14,600 | ||

| 14,600 | |||

| Service Revenue (R) | |||

| 0 | Bal. | ||

| 230,000 | 29-Dec | ||

| 230,000 | |||

| Salaries and Wages Expense (E) | |||

| Bal. | 0 | ||

| 30-Dec | 200,000 | ||

| 200,000 | |||

| Depreciation Expense (E) | |||

| Bal. | 0 | ||

| 31-Dec | 10,000 | ||

| 10,000 | |||

| Retained Earnings (SE) | |||

| 120,000 | Bal. | ||

| 120,000 | |||

4.

Prepare a closing journal entry for the income statement accounts, assume that the events occurred on December 29 to 31 were the only transactions to affect income statement accounts.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare a closing journal entry for the income statement accounts, assume that the events occurred on December 29 to 31 were the only transactions to affect income statement accounts.

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31 | Service Revenue | 230,000 | |

| Salaries and Wages Expense | 200,000 | ||

| Depreciation Expense | 10,000 | ||

| Retained Earnings | 20,000 | ||

| (To record the closure of expense account to income summary) |

(Table 3)

Revenue account:

In this closing entry, service revenue account is closed by transferring the amount of service revenue to the retained earnings account in order to bring the revenue account balance to zero. Hence, debit the service revenue account and credit retained earnings account.

Expenses account:

In this closing entry, expenses account is closed by transferring the amount of expenses to the retained earnings in order to bring the expenses account balance to zero. Hence, debit the retained earnings account and credit all expenses account.

5.

Prepare the closing entry for dividends.

Explanation of Solution

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31 | Retained Earnings | 14,600 | |

| Dividends (5) | 14,600 | ||

| (To record the closing entry of dividends) |

(Table 4)

- Retained earnings are a component of stockholder’s equity and there is a decrease in the value of equity. Hence, it is debited.

- Dividend is a component of stockholder’s equity and there is an increase in the value of dividend. Hence, it is credited.

6.

Prepare a classified balance sheet at December 31.

Explanation of Solution

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare a classified balance sheet at December 31:

| Incorporation A | ||

| Classified Balance Sheet | ||

| At December 31 | ||

| Assets | ||

| Current Assets: | ||

| Cash | $189,600 | |

| Accounts Receivable | 0 | |

| Allowance for Doubtful Accounts | 0 | |

| Total Current Assets | 189,600 | |

| Buildings | 247,000 | |

| Less: Accumulated Depreciation | -40,000 | |

| 207,000 | ||

| Total Assets | $396,600 | |

| Liabilities and Stockholders’ Equity | ||

| Liabilities | ||

| Current Liabilities | ||

| Dividends Payable | $14,600 | |

| Total Current Liabilities | 14,600 | |

| Noncurrent Liabilities: | ||

| Notes Payable (long-term) | 10,000 | |

| Bonds Payable | 100,000 | |

| Premium on Bonds Payable | 1,000 | |

| Total Noncurrent Liabilities | 111,000 | |

| Total Liabilities (a) | 125,600 | |

| Stockholders’ Equity | ||

| Contributed Capital: | ||

| Common Stock, | 15,000 | |

| Additional Paid-in Capital | 135,000 | |

| Total Contributed Capital | 150,000 | |

| Retained Earnings (8) | 125,400 | |

| Less: Treasury Stock, at cost | -4,400 | |

| Total Stockholders’ Equity (b) | 271,000 | |

| Total Liabilities and Stockholders’ Equity | $396,600 | |

(Table 5)

Working notes (8):

7.

Calculate the debt-to-assets ratio at January 1 and December 31. Describe whether the company rely more (or less) on debt financing at the end of the year than at the beginning of the year.

Explanation of Solution

Calculate the debt-to-assets ratio at January 1:

Calculate the debt-to-assets ratio at December 31

Working notes (9):

Compute the total assets at January 1:

| Particulars | $ |

| Cash | $10,000 |

| Accounts Receivable | 5,000 |

| Less: Allowance for doubtful accounts | -2,000 |

| Buildings | 247,000 |

| Less: Accumulated Depreciation | -30,000 |

| Total | $230,000 |

(Table 6)

Want to see more full solutions like this?

Chapter 11 Solutions

Fundamentals Of Financial Accounting

- Entries for selected corporate transactions Nav-Go Enterprises Inc. produces aeronautical navigation equipment. The stockholders equity accounts of Nav-Go Enterprises Inc., with balances on January 1, 20Y3, are as follows: The following selected transactions occurred during the year: Jan. 15. Paid cash dividends of 0.06 per share on the common stock. The dividend had been properly recorded when declared on December 1 of the preceding fiscal year for 34,320. Mar. 15. Sold all of the treasury stock for 6.75 per share. Apr. 13. Issued 200,000 shares of common stock for 8 per share. June 14. Declared a 3% stock dividend on common stock, to be capitalized at the market price of the stock, which is 7.50 per share. July 16. Issued the certificates for the dividend declared on June 14. Oct. 30. Purchased 50,000 shares of treasury stock for 6 per share. Dec. 30. Declared a 0.08-per-share dividend on common stock. 31. Closed the two dividends accounts to Retained Earnings. Instructions 1. Enter the January 1 balances in T accounts for the stockholders equity accounts listed. Also prepare T accounts for the following: Paid-In Capital from Sale of Treasury Stock; Stock Dividends Distributable; Stock Dividends; Cash Dividends. 2. Journalize the entries to record the transactions and post to the eight selected accounts. 3. Prepare a retained earnings statement for the year ended December 31, 20Y3. 4. Prepare the Stockholders Equity section of the December 31, 20Y3, balance sheet Using Method 1 of Exhibit 8.arrow_forwardEntries for selected corporate transactions Nav-Go Enterprises Inc. produces aeronautical navigation equipment. Navo-Go Enterprises stockholders equity accounts, with balances on January 1, 20Y1, are as follows: The following selected transactions occurred during the year: Instructions 1. Enter the January 1 balances in T accounts for the stockholders equity accounts listed. Also prepare T accounts for the following: Paid-In Capital from Sale of Treasury Stock; Stock Dividends Distributable; Stock Dividends; Cash Dividends. 2. Journalize the entries to record the transactions, and post to the eight selected accounts. Assume that the closing entry for revenues and expenses has been made and post net income of 775,000 to the retained earnings account. 3. Prepare a statement of stockholders equity for the year ended December 31, 20Y1. Assume that net income was 775,000 for the year ended December 31, 20Y6. 4. Prepare the Stockholders Equity section of the December 31, 20Y1, balance sheet.arrow_forwardEntries for selected corporate transactions Morrow Enterprises Inc. manufactures bathroom fixtures. Morrow Enterprises stockholders equity accounts, with balances on January 1, 20Y6, are as follows: The following selected transactions occurred during the year: Instructions 1. Enter the January 1 balances in T accounts for the stockholders equity accounts listed. Also prepare T accounts for the following: Paid-In Capital from Sale of Treasury Stock; Stock Dividends Distributable; Stock Dividends; Cash Dividends. 2. Journalize the entries to record the transactions, and post to the eight selected accounts. Assume that the closing entry for revenues and expenses has been made and post net income of 1,125,000 to the retained earnings account. 3. Prepare a statement of stockholders equity for the year ended December 31, 20Y6. Assume that net income was 1,125,000 for the year ended December 31, 20Y6. 4. Prepare the Stockholders Equity section of the December 31, 20Y6, balance sheet.arrow_forward

- Selected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 2016, were as follows: a. Issued 15,000 shares of 20 par common stock at 30, receiving cash. b. Issued 4, 000 shares of 80 par preferred 5% stock at 100, receiving cash. c. Issued 500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of 0.50 per share on common stock and 1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held, and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at 40 per share, plus a 150 brokerage commission. The investment is classified as an available-for-sale investment. g. Purchased 8,000 shares of treasury common stock at 33 per share. h. Purchased 40,000 shares of Pinkberry Co. stock directly from the founders for 24 per share. Pinkberry has 125,000 shares issued and outstanding. Equinox Products Inc. treated the investment as an equity method investment. i. Declared a 1.00 quarterly cash dividend per share on preferred stock. On the date of record, 20,000 shares of preferred stock had been issued. j. Paid the cash dividends to the preferred stockholders. k. Received 27,500 dividend from Pinkberry Co. investment in (h). l. Purchased 90,000 of Dream Inc. 10-year, 5% bonds, directly from the issuing company, at their face amount plus accrued interest of 37 5. The bonds are classified as a held-to-maturity long -term investment. m. Sold, at 38 per share, 2,600 shares of treasury common stock purchased in (g). n. Received a dividend of 0 .60 per share from the Solstice Corp. investment in (f). o. Sold 1,000 shares of Solstice Corp. at 45, including commission. p. Recorded the payment of semiannual interest on the bonds issue d in (c) and the amortization of the premium for six months. The amortization is determined using the straight-line method . q. Accrued interest for three months on the Dream Inc. bonds purchased in (I). r. Pinkberry Co. recorded total earnings of 240 ,000. Equinox Products recorded equity earnings for its share of Pinkberry Co. net income. s. The fair value for Solstice Corp. stock was 39. 02 per share on December 31, 2016. The investment is adjusted to fair value , using a valuation allowance account. Assume Valuation Allowance for Available-for-Sale Investments h ad a beginning balance of zero. Instructions 1. Journalize the selected transactions. 2. After all of the transaction s for the year ended December 31, 201 6, had been poste d [including the transactions recorded in part (1) and all adjusting entries), the data that follows were taken from the records of Equinox Products Inc. a. Prepare a multiple-step in come statement for the year ended December 31, 201 6, concluding with earnings per share . In computing earnings per share, assume that the average number of common shares outstanding was 100,000 and preferred dividends were 100,000. ( Round earnings per share to the nearest cent.) b. Prepare a retained earnings statement for the year ended December 31, 20 6. c. Prepare a balance sheet in report form as of December 31, 2016.arrow_forwardNutritious Pet Food Companys board of directors declares a cash dividend of $1.00 per common share on November 12. On this date, the company has issued 12,000 shares but 2,000 shares are held as treasury shares. The company pays the dividend on December 14. What is the journal entry to record the payment of the dividend?arrow_forwardThe following selected accounts appear in the ledger of EJ Construction Inc. at the beginning of the current fiscal year: During the year, the corporation completed a number of transactions affecting the stockholders equity. They are summarized as follows: a. Issued 500,000 shares of common stock at 8, receiving cash. b. Issued 10,000 shares of preferred 1% stock at 60. c. Purchased 50,000 shares of treasury common for 7 per share. d. Sold 20,000 shares of treasury common for 9 per share. e. Sold 5,000 shares of treasury common for 6 per share. f. Declared cash dividends of 0.50 per share on preferred stock and 0.08 per share on common stock. g. Paid the cash dividends. Instructions Journalize the entries to record the transactions. Identify each entry by letter.arrow_forward

- Selected stock transactions The following selected accounts appear in the ledger of Parks Construction Inc. at the beginning of the current year: During the year, the corporation completed a number of transactions affecting the stockholders equity. They are summarized as follows: a. Issued 400,000 shares of common stock at 11, receiving cash. b. Issued 5,000 shares of preferred 2% stock at 90. c. Purchased 150,000 shares of treasury common for 10 per share. d. Sold 80,000 shares of treasury common for 13 per share. e. Sold 20,000 shares of treasury common for 9 per share. f. Declared cash dividends of 1.50 per share on preferred stock and 0.06 per share on common stock. g. Paid the cash dividends. Instructions Journalize the entries to record the transactions. Identify each entry by letter.arrow_forwardStockholders' Equity section of balance sheet The following accounts and their balances appear in the ledger of Goodale Properties Inc. on June 30 of the current year: Prepare the Stockholders Equity section of the balance sheet as of June 30. Eighty thousand shares of common stock are authorized, and 9,000 shares have been reacquired.arrow_forwardCommon stock transactions on the statement of cash flows Jones Industries received 600,000 from issuing shares of its common stock and 400,000 from issuing bonds. During the year, Jones Industries also paid dividends of 60,000. How are the effects of these transactions reported on the statement of cash flows?arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,