Concept explainers

Videos

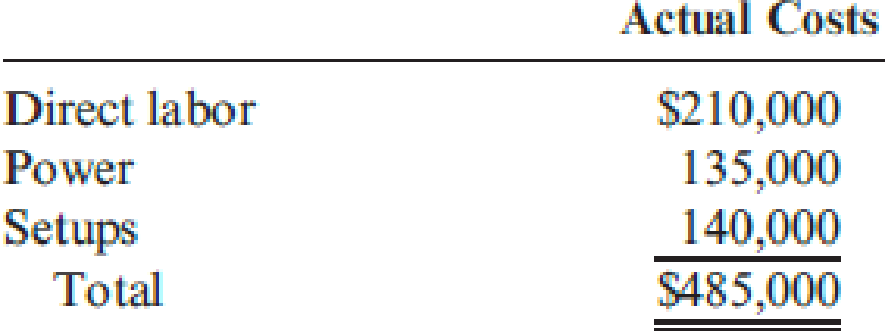

Kelly Gray, production manager, was upset with the latest performance report, which indicated that she was $100,000 over budget. Given the efforts that she and her workers had made, she was confident that they had met or beat the budget. Now, she was not only upset but also genuinely puzzled over the results. Three items—direct labor, power, and setups—were over budget. The actual costs for these three items follow:

Kelly knew that her operation had produced more units than originally had been budgeted, so more power and labor had naturally been used. She also knew that the uncertainty in scheduling had led to more setups than planned. When she pointed this out to John Huang, the controller, he assured her that the budgeted costs had been adjusted for the increase in productive activity. Curious, Kelly questioned John about the methods used to make the adjustment.

JOHN: If the actual level of activity differs from the original planned level, we adjust the budget by using budget formulas—formulas that allow us to predict what the costs will be for different levels of activity.

KELLY: The approach sounds reasonable. However, I’m sure something is wrong here. Tell me exactly how you adjusted the costs of labor, power, and setups.

JOHN: First, we obtain formulas for the individual items in the budget by using the method of least squares. We assume that cost variations can be explained by variations in productive activity where activity is measured by direct labor hours. Here is a list of the cost formulas for the three items you mentioned. The variable X is the number of direct labor hours:

Labor cost = $10X

Power cost = $5,000 + $4X

Setup cost = $100,000

KELLY: I think I see the problem. Power costs don’t have a lot to do with direct labor hours. They have more to do with machine hours. As production increases, machine hours increase more rapidly than direct labor hours. Also, ...

JOHN: You know, you have a point. The coefficient of determination for power cost is only about 50 percent. That leaves a lot of unexplained cost variation. The coefficient for labor, however, is much better—it explains about 96 percent of the cost variation. Setup costs, of course, are fixed.

KELLY: Well, as I was about to say, setup costs also have very little to do with direct labor hours. And I might add that they certainly are not fixed—at least not all of them. We had to do more setups than our original plan called for because of the scheduling changes. And we have to pay our people when they work extra hours. It seems as if we are always paying overtime. I wonder if we simply do not have enough people for the setup activity. Supplies are used for each setup, and these are not cheap. Did you build these extra costs of increased setup activity into your budget?

JOHN: No, we assumed that setup costs were fixed. I see now that some of them could vary as the number of setups increases. Kelly, let me see if I can develop some cost formulas based on better explanatory variables. I’ll get back with you in a few days.

Assume that after a few days’ work, John developed the following cost formulas, all with a coefficient of determination greater than 90 percent:

Labor cost = $10X; where X = Direct labor hours

Power cost = $68,000 + 0.9Y; where Y = Machine hours

Setup cost = $98,000 + $400Z; where Z = Number of setups

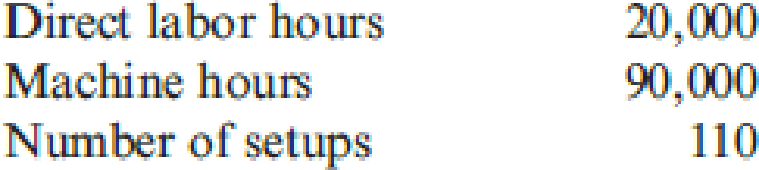

The actual measures of each of the activity drivers are as follows:

Required:

- 1. Prepare a performance report for direct labor, power, and setups using the direct-labor-based formulas.

- 2. Prepare a performance report for direct labor, power, and setups using the multiple cost driver formulas that John developed.

- 3. Of the two approaches, which provides the most accurate picture of Kelly’s performance? Why?

- 4. After reviewing the approach to performance measurement, a consultant remarked that non-value-added cost trend reports would be a much better performance measurement approach than comparing actual costs with budgeted costs—even if activity flexible budgets were used. Do you agree or disagree? Explain.

Trending nowThis is a popular solution!

Chapter 12 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Jane Erickson, manager of an electronics division, was not pleased with the results that had recently been reported concerning the divisions activity-based management implementation project. For one thing, the project had taken eight months longer than projected and had exceeded the budget by nearly 35 percent. But even more vexatious was the fact that after all was said and done, about three-fourths of the plants were reporting that the activity-based product costs were not much different for most of the products than those of the old costing system. Plant managers were indicating that they were continuing to use the old costs as they were easier to compute and understand. Yet, at the same time, they were complaining that they were having a hard time meeting the bids of competitors. Reliable sources were also revealing that the divisions product costs were higher than many competitors. This outcome perplexed plant managers because their control system still continued to report favorable materials and labor efficiency variances. They complained that ABM had failed to produce any significant improvement in cost performance. Jane decided to tour several of the plants and talk with the plant managers. After the tour, she realized that her managers did not understand the concept of non-value-added costs nor did they have a good grasp of the concept of kaizen costing. No efforts were being made to carefully consider the activity information that had been produced. One typical plant manager threw up his hands and said: This is too much data. Why should I care about all this detail? I do not see how this can help me improve my plants performance. They tell me that inspection is not a necessary activity and does not add value. I simply cant believe that inspecting isnt value-added and necessary. If we did not inspect, we would be making and sending more bad products to customers. Required: Explain why Janes division is having problems with its ABM implementation.arrow_forwardThe controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardHandbrain Inc. is considering a change to activity-based product costing. The company produces two products, cell phones and tablet PCs, in a single production department. The production department is estimated to require 2,000 direct labor hours. The total indirect labor is budgeted to be 200,000. Time records from indirect labor employees revealed that they spent 30% of their time setting up production runs and 70% of their time supporting actual production. The following information about cell phones and tablet PCs was determined from the corporate records: a. Determine the indirect labor cost per unit allocated to cell phones and tablet PCs under a single plantwide factory overhead rate system using the direct labor hours as the allocation base. b. Determine the budgeted activity costs and activity rates for the indirect labor under activity-based costing. Assume two activitiesone for setup and the other for production support. c. Determine the activity cost per unit for indirect labor allocated to each product under activity-based costing. d. Why are the per-unit allocated costs in (a) different from the per-unit activity cost assigned to the products in (c)?arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardDouglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)arrow_forwardJackie Iverson was furious. She was about ready to fire Tom Rich, her purchasing agent. Just a month ago, she had given him a salary increase and a bonus for his performance. She had been especially pleased with his ability to meet or beat the price standards. But now, she found out that it was because of a huge purchase of raw materials. It would take months to use that inventory, and there was hardly space to store it. In the meantime, space had to be found for the other materials supplies that would be ordered and processed on a regular basis. Additionally, it was a lot of capital to tie up in inventorymoney that could have been used to help finance the cash needs of the new product just coming online. Her interview with Tom was frustrating. He was defensive, arguing that he thought she wanted those standards met and that the means were not that important. He also pointed out that quantity purchases were the only way to meet the price standards. Otherwise, an unfavorable variance would have been realized. Required: 1. CONCEPTUAL CONNECTION Why did Tom Rich purchase the large quantity of raw materials? Do you think that this behavior was the objective of the price standard? If not, what is the objective(s)? 2. CONCEPTUAL CONNECTION Suppose that Tom is right and that the only way to meet the price standards is through the use of quantity discounts. Also, assume that using quantity discounts is not a desirable practice for this company. What would you do to solve this dilemma? 3. CONCEPTUAL CONNECTION Should Tom be fired? Explain.arrow_forward

- Recently, Ulrich Company received a report from an external consulting group on its quality costs. The consultants reported that the companys quality costs total about 21 percent of its sales revenues. Somewhat shocked by the magnitude of the costs, Rob Rustin, president of Ulrich Company, decided to launch a major quality improvement program. For the coming year, management decided to reduce quality costs to 17 percent of sales revenues. Although the amount of reduction was ambitious, most company officials believed that the goal could be realized. To improve the monitoring of the quality improvement program, Rob directed Pamela Golding, the controller, to prepare monthly performance reports comparing budgeted and actual quality costs. Budgeted costs and sales for the first two months of the year are as follows: The following actual sales and actual quality costs were reported for January: Required: 1. Reorganize the monthly budgets so that quality costs are grouped in one of four categories: appraisal, prevention, internal failure, or external failure. (Essentially, prepare a budgeted cost of quality report.) Also, identify each cost as variable (V) or fixed (F). (Assume that no costs are mixed.) 2. Prepare a performance report for January that compares actual costs with budgeted costs. Comment on the companys progress in improving quality and reducing its quality costs.arrow_forwardCassara, Inc., had the following quality costs for the years ended December 31, 20X1 and 20X2: At the end of 20X1, management decided to increase its investment in control costs by 40% for each categorys items, with the expectation that failure costs would decrease by 25% for each item of the failure categories. Sales were 12,000,000 for both 20X1 and 20X2. Required: 1. Calculate the budgeted costs for 20X2, and prepare an interim quality performance report. 2. Comment on the significance of the report. How much progress has Cassara made?arrow_forwardAnderson Company has the following departmental manufacturing structure for one of its products: After some study, the production manager of Anderson recommended the following revised cellular manufacturing approach: Required: 1. Calculate the total time it takes to produce a batch of 20 units using Andersons traditional departmental structure. 2. Using cellular manufacturing, how much time is saved producing the same batch of 20 units? Assuming the cell operates continuously, what is the production rate? Which process controls this production rate? 3. What if the processing times of molding, welding, and assembly are all reduced to six minutes each? What is the production rate now, and how long will it take to produce a batch of 20 units?arrow_forward

- Young Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forwardTonya Martin, CMA and controller or the Parts Division of Gunderson Inc., was meeting with Doug Adams, manager of the division. The topic of discussion was the assignment of overhead costs to jobs and their impact on the divisions pricing decisions. Their conversation was as follows: Tonya: Doug, as you know, about 25% of our business is based on government contracts, with the other 75% based on jobs from private sources won through bidding. During the last several years, our private business has declined. We have been losing more bids than usual. After some careful investigation, I have concluded that we are overpricing some jobs because of improper assignment of overhead costs. Some jobs are also being underpriced. Unfortunately, the jobs being overpriced are coming from our higher-volume, labor-intensive products, so we are losing business. Dong: I think I understand. Jobs associated with our high-volume products are being assigned more overhead than they should be receiving. Then when we add our standard 40% markup, we end up with a higher price than our competitors, who assign costs more accurately. Tonya: Exactly. We have two producing departments, one labor-intensive and the other machine-intensive. The labor-intensive department generates much less overhead than the machine-intensive department. Furthermore, virtually all of our high-volume jobs are labor-intensive. We have been using a plantwide rate based on direct labor hours to assign overhead to all jobs. As a result, the high-volume, labor-intensive jobs receive a greater share of the machine-intensive departments overhead than they deserve. This problem can be greatly alleviated by switching to departmental overhead rates. For example, an average high-volume job would be assigned 100,000 of overhead using a plantwide rate and only 70,000 using departmental rates. The change would lower our bidding price on high-volume jobs by an average of 42,000 per job. By increasing the accuracy of our product costing, we can make better pricing decisions and win back much of our private-sector business. Doug: Sounds good. When can you implement the change in overhead rates? Tonya: It wont take long. I can have the new system working within four to six weekscertainly by the start of the new fiscal year. Doug: Hold it. I just thought of a possible complication. As I recall, most of our government contract work is done in the labor-intensive department. This new overhead assignment scheme will push down the cost on the government jobs, and we will lose revenues. They pay us full cost plus our standard markup. This business is not threatened by our current costing procedures, but we cant switch our rates for only the private business. Government auditors would question the lack of consistency in our costing procedures. Tonya: You do have a point. I thought of this issue also. According to my estimates, we will gain more revenues from the private sector than we will lose from our government contracts. Besides, the costs of our government jobs are distorted. In effect, we are overcharging the government. Doug: They dont know that and never would unless we switch our overhead assignment procedures. I think I have the solution. Officially, lets keep our plantwide overhead rate. All of the official records will reflect this overhead costing approach for both our private and government business. Unofficially. I want you to develop a separate set of books that can be used to generate the information we need to prepare competitive bids for our private-sector business. Required: 1. Do you believe that the solution proposed by Doug is ethical? Explain. 2. Suppose that Tonya decides that Dougs solution is not right and objects strongly. Further suppose that, despite Tonyas objections, Doug insists strongly on implementing the action. What should Tonya do?arrow_forwardIn 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality costs were 31% of sales. Faced with increasing pressures from imported goods. Don resolved to take measures to improve the overall quality of the companys products. After hiring a consultant in 20X1, the company began an aggressive program of total quality control. At the end of 20X5, Don requested an analysis of the progress the company had made in reducing and controlling quality costs. The accounting department assembled the following data: Required: 1. Compute the quality costs as a percentage of sales by category and in total for each year. 2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain. 3. Using the 20X1 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 20X4. By how much did profits increase in 20X4 because of the quality improvement program? Repeat for 20X5.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning