Videos

Cost Allocations: Comparison of Dual and Single Rates

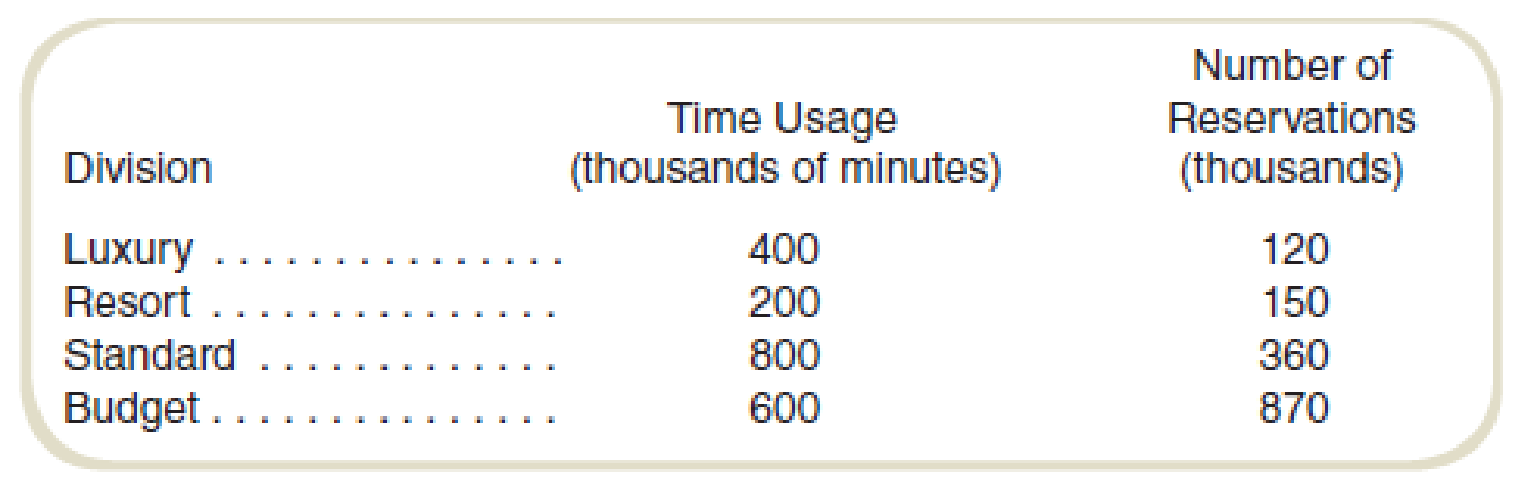

Pacific Hotels operates a centralized call center for the reservation needs of its hotels. Costs associated with use of the center are charged to the hotel group (luxury, resort, standard, and budget) based on the length of time of calls made (time usage). Idle time of the reservation agents, time spent on calls in which no reservation is made, and the fixed cost of the equipment are allocated based on the number of reservations made in each group. Due to recent increased competition in the hotel industry, the company has decided that it is necessary to better allocate its costs in order to price its services competitively and profitably. During the most recent period for which data are available, the use of the call center for each hotel group was as follows:

During this period, the cost of the call center amounted to $840,000 for personnel and $650,000 for equipment and other costs.

Required

- a. Determine the allocation to each of the divisions using the following:

- 1. A single rate based on time used.

- 2. Dual rates based on time used (for personnel costs) and number of reservations (for equipment and other cost).

- b. Write a short report to management explaining whether a single rate or dual rates should be used and why.

a.

Determine the allocation to each of the divisions using the following:

1. A single rate based on the time used.

2. Dual rates based on time used (for personnel costs) and some reservations (for equipment and other cost).

Explanation of Solution

Cost allocation:

Cost allocation is the process of distributing a common cost into the departments that have used the cost. The cost is allocated on the basis of the utilization of the resource.

1.

Allocation of total cost on the basis of a single rate based on time used:

| Particular |

The ratio of time usage (a) |

Amount |

| Luxury | 0.2 (1) | $298,000 |

| Resort | 0.1 (2) | $149,000 |

| Standard | 0.4 (3) | $596,000 |

| Budget | 0.3 (4) | $447,000 |

| Total cost | 1,490,000 |

Table: (1)

Thus, the total cost allocation for luxury, resort, standard and budget is $298,000, $149,000, $596,000 and $447,000.

Working note 1:

Calculate the ratio of time usage for luxury:

Working note 2:

Calculate the ratio of time usage for the resort:

Working note 3:

Calculate the ratio of time usage for standard:

Working note 4:

Calculate the ratio of time usage for luxury:

2.

Calculate the allocation of cost on Dual rates based on time used (for personnel costs) and some reservations (for equipment and other cost):

Allocation of cost for personnel costs:

| Particular |

The ratio of time usage (a) |

Amount |

| Luxury | 0.2 (1) | $168,000 |

| Resort | 0.1 (2) | $84,000 |

| Standard | 0.4 (3) | $336,000 |

| Budget | 0.3 (4) | $252,000 |

| Total cost | 840,000 |

Table: (2)

Thus, the personnel cost allocation for luxury, resort, standard and budget is $168,000, $84,000, $336,000 and $252,000.

Allocation of cost for equipment and other costs:

| Particular |

The ratio of the number of reservations (a) |

Amount |

| Luxury | 0.08 (1) | $52,000 |

| Resort | 0.1 (2) | $65,000 |

| Standard | 0.24 (3) | $156,000 |

| Budget | 0.58 (4) | $377,000 |

| Total cost | $650,000 |

Table: (3)

Thus, the personnel cost allocation for luxury, resort, standard and budget is $168,000, $84,000, $336,000 and $252,000.

Working note 5:

Calculate the ratio of the number of reservations for luxury:

Working note 6:

Calculate the ratio of the number of reservations for the resort:

Working note 7:

Calculate the ratio of the number of reservations for standard:

Working note 8:

Calculate the ratio of the number of reservations for luxury:

b.

Write a short report to management explaining whether a single rate or dual rates should be used and why.

Explanation of Solution

The cost should be allocated on the basis of the dual rate system.

In single rate allocation, the cost of equipment and other cost do not correlate with the time usage. So allocating the cost of equipment and other cost is not reasonable in this case.

Dual rate system has better correlation with the costs and usage. The cost of personnel’s is directly correlated with the time usage, and the cost of equipment and other cost are directly correlated with the number of reservations.

Thus, cost should be allocated on the basis of the dual rate system.

Want to see more full solutions like this?

Chapter 12 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Ohio Logistics manages the logistical activities for firms by matching companies that need products shipped with carriers that can provide the best rates and best service for the companies. Ohio Logistics is very concerned that its carriers deliver their customers material on time, so it carefully monitors the percentage of on-time deliveries. The following table contains a list of the carriers used by Ohio Logistics and the corresponding on-time percentages for the current and previous years. a. Sort the carriers in descending order by their current years percentage of on-time deliveries. Which carrier is providing the best service in the current year? Which carrier is providing the worst service in the current year? b. Calculate the change in percentage of on-time deliveries from the previous to the current year for each carrier. Use Excels conditional formatting to highlight the carriers whose on-time percentage decreased from the previous year to the current year. c. Use Excels conditional formatting tool to create data bars for the change in percentage of on-time deliveries from the previous year to the current year for each carrier calculated in part b. d. Which carriers should Ohio Logistics try to use in the future? Why?arrow_forwardRegression, activity-based costing, choosing cost drivers. Sleep Late, a large hotel chain, has been using activity-based costing to determine the cost of a night’s stay at their hotels. One of the activities, “Inspection,” occurs after a customer has checked out of a hotel room. Sleep Late inspects every 10th room and has been using “number of rooms inspected” as the cost driver for inspection costs. A signicant component of inspection costs is the cost of the supplies used in each inspection.arrow_forwardCost Drivers for Support Department Allocations For each of the following support departments, select the cost driver listed that is most appropriate for allocating support department costs to responsible units. Your answer should include the number of the cost driver only. Cost drivers to choose from: Number of conference attendees Number of computers Number of employees trained Number of cell phone minutes used Number of purchase requisitions Number of sales invoices Number of payroll checks Number of travel claims Support Department Cost Driver a. Accounts Receivable b. Central Purchasing c. Computer Support d. Conferences e. Employee Travel f. Payroll Accounting g. Telecommunications h. Trainingarrow_forward

- Departmental Cost Allocation in Profit Centers Elvis Wilbur owns two restaurants, the BeefBarn and the Fish Bowl. Each restaurant is treated as a profit center for performance evaluation.Although the restaurants have separate kitchens, they share a central baking facility. The principalcosts of the baking area include depreciation and maintenance on the equipment, materials, supplies,and labor.Required1. Elvis allocates the monthly costs of the baking facility to the two restaurants based on the number oftables served in each restaurant during the month. In April the costs were $24,000, of which $12,000is fixed cost. The Beef Barn and the Fish Bowl each served 3,000 tables. How much of the joint costshould be allocated to each restaurant?a. Beef Barn: $16,000; Fish Bowl: $8,000b. Beef Barn: $8,000; Fish Bowl: $16,000c. Beef Barn: $10,000; Fish Bowl: $14,000d. Beef Barn: $12,000; Fish Bowl: $12,000arrow_forwardWestern Services has three service departments: Information Systems (IS), Personnel, and Administration. There are two operating departments: Residential and Commercial. A summary of costs and other data for each department prior to allocation of service department costs for the latest period follows: IS Personnel Administration Residential Commercial Number of IS service tickets 130 160 115 1,410 940 Number of employees 75 80 67 138 162 Square footage occupied 3,900 8,000 3,800 16,100 69,500 The costs of the service departments and the allocation basis for each department follow. Department Direct Cost Allocation Base Information Systems (IS) $ 25,000 IS service tickets Personnel 32,000 Employees Administration 28,700 Square footage occupied d. Assuming that the company allocates service department costs to other departments using the step method (starting with Administration and then IS), What amount of IS Department costs is allocated to Administration?arrow_forwardWestern Services has three service departments: Information Systems (IS), Personnel, and Administration. There are two operating departments: Residential and Commercial. A summary of costs and other data for each department prior to allocation of service department costs for the latest period follows: IS Personnel Administration Residential Commercial Number of IS service tickets 130 160 115 1,410 940 Number of employees 75 80 67 138 162 Square footage occupied 3,900 8,000 3,800 16,100 69,500 The costs of the service departments and the allocation basis for each department follow. Department Direct Cost Allocation Base Information Systems (IS) $ 25,000 IS service tickets Personnel 32,000 Employees Administration 28,700 Square footage occupied Required: Assume that the company allocates service department costs to production departments using the direct method. What amount of Information Systems (IS) Department costs will be allocated to the Commercial…arrow_forward

- Western Services has three service departments: Information Systems (IS), Personnel, and Administration. There are two operating departments: Residential and Commercial. A summary of costs and other data for each department prior to allocation of service department costs for the latest period follows: IS Personnel Administration Residential Commercial Number of IS service tickets 125 155 110 1,410 940 Number of employees 70 75 62 138 162 Square footage occupied 3,900 8,000 3,800 16,100 69,500 The costs of the service departments and the allocation basis for each department follow. Department Direct Cost Allocation Base Information Systems (IS) $ 24,000 IS service tickets Personnel 31,000 Employees Administration 27,700 Square footage occupied Required: Assume that the company allocates service department costs to production departments using the direct method. What amount of Information Systems (IS) Department costs will be allocated to the Commercial…arrow_forwardRequired information Skip to question [The following information applies to the questions displayed below.] Zenon Computer competes at the retail level on the basis of customer service. It has invested significant resources in its customer service department. Recently, the company has installed a traditional activity-based costing (ABC) system to provide better cost information for pricing, decision making, and customer profitability analysis. Most of the costs of running the customer service department are considered committed (i.e., short-term fixed) costs (principally, personnel and equipment costs). The budgeted cost for the upcoming period is $832,000. Activity analysis, recently conducted when the ABC system was implemented, revealed the following information: Activities Percentage of Employee Time Estimated (Budgeted) Cost Driver Quantity Handling customer orders 75% 8,320 customer orders Processing customer complaints 10 416 customer complaints Conducting customer credit checks…arrow_forwardManning Systems is a commercial software vendor that sells billing and other financial software to companies around the globe. Manning operates a centralized call center for customer support calls. Costs associated with use of the center are charged to the division with primary responsibility for the client. There are four geographical divisions: North America (NA), Central and South America (SA), Europe, and Asia-Pacific (APAC). The allocation is based on the length of time of calls made (Minutes). Idle time of the reservation agents and the fixed cost of the equipment are allocated based on the number of calls received (Calls) from clients in each division. Due to recent increased competition in the commercial software business, Manning has decided that it is necessary to better allocate its costs in order to price its services competitively and profitably. During the most recent period for which data are available, the use of the call center for each division was as follows:…arrow_forward

- Support department cost allocation Blue Mountain Masterpieces produces pictures, paintings, and other home decor. The Printing and Framing production departments are supported by the Janitorial and Security departments. Janitorial costs are allocated to the production departments based on square feet, and security costs are allocated based on asset value. Information about these departments is detailed in the following table: Management has experimented with different support department cost allocation methods in the past. The different allocation methods did not yield large differences of cost allocation to the production departments. Instructions 1. Determine which support department cost allocation method Blue Mountain Masterpieces would most likely use to allocate its support department costs to the production departments. 2. Determine the total costs allocated from each support department to each production department using the method you determined in part (1). 3. Without doing calculations, consider and answer the following: If Blue Mountain Masterpieces decided to use square feet instead of asset value as the cost driver for security services, how would this change the allocation of Security Department costs?arrow_forwardSeveral costs incurred by Cape Cod Hotel and Restaurant are given in the following list. For each cost,indicate which of the following classifications best describe the cost. More than one classification mayapply to the same cost item.Cost Classificationsa. Direct cost of the food and beverage departmentb. Indirect cost of the food and beverage departmentc. Controllable by the kitchen managerd. Uncontrollable by the kitchen managere. Controllable by the hotel general managerf. Uncontrollable by the hotel general managerg. Differential costh. Marginal costi. Opportunity costj. Sunk costk. Out-of-pocket costCost Items1. The wages earned by table-service personnel.2. The salary of the kitchen manager.3. The cost of the refrigerator purchased 14 months ago. The unit was covered by a warranty for12 months, during which time it worked perfectly. It conked out after 14 months, despite an original estimate that it would last five years.4. The hotel has two options for obtaining fresh pies,…arrow_forwardSeveral costs incurred by Cape Cod Hotel and Restaurant are given in the following list. For each cost,indicate which of the following classifications best describe the cost. More than one classification mayapply to the same cost item.Cost Classificationsa. Direct cost of the food and beverage departmentb. Indirect cost of the food and beverage departmentc. Controllable by the kitchen managerd. Uncontrollable by the kitchen managere. Controllable by the hotel general managerf. Uncontrollable by the hotel general managerg. Differential costh. Marginal costi. Opportunity costj. Sunk costk. Out-of-pocket costCost Items1. The wages earned by table-service personnel.2. The salary of the kitchen manager.3. The cost of the refrigerator purchased 14 months ago. The unit was covered by a warranty for12 months, during which time it worked perfectly. It conked out after 14 months, despite an original estimate that it would last five years.4. The hotel has two options for obtaining fresh pies,…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning