Concept explainers

Videos

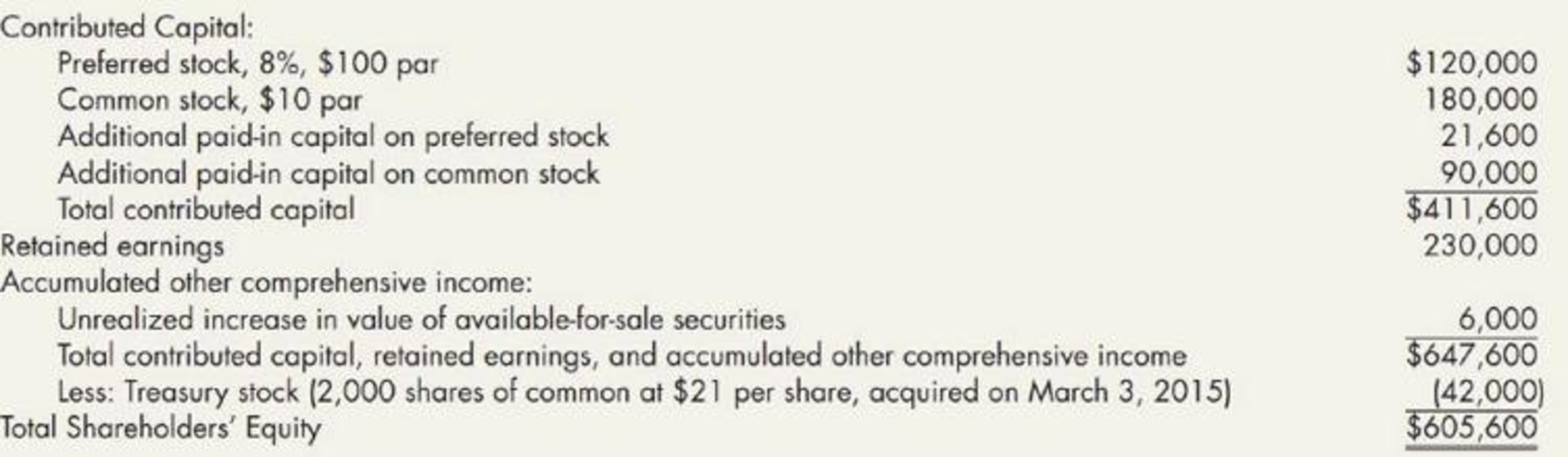

Gray Company lists the following shareholders’ equity items on its December 31, 2018, balance sheet:

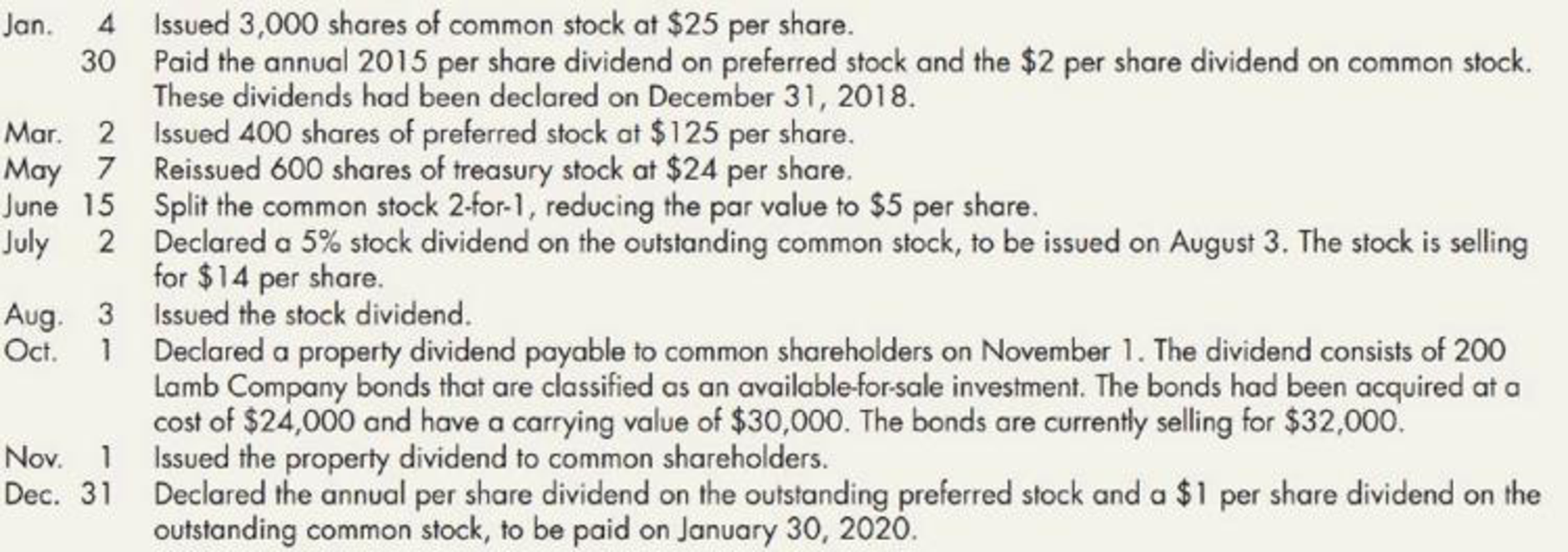

The following stock transactions occurred during 2019:

Required:

- 1. Prepare

journal entries to record the preceding transactions. - 2. Prepare the December 31, 2019, shareholders’ equity section (assume that 2019 net income was $225,000).

1.

Prepare necessary journal entry to record the given transactions.

Explanation of Solution

Stockholders’ Equity Section:

It is refers to the section of the balance sheet that shows the available balance stockholders’ equity as on reported date at the end of the financial year.

| Date | Account Titles and explanation | Debit ($) | Credit ($) |

| January 4, 2019 | Cash | 75,000 | |

| Common stock , at $10par | 10,000 | ||

|

Additional paid-in capital from stock dividend | 45,000 | ||

| ( To record the issuance of 1000 share of common stock at $40 per share) | |||

| January 30, 2019 | Dividend payable: Preferred | 9,600 | |

| Dividend payable: Common (1) | 32,000 | ||

| Cash | 41,600 | ||

| (To record declaration of preferred and common stock) | |||

| March 2, 2019 | Cash | 15,000 | |

| Preferred stock, $100 par | 1,500 | ||

|

Additional paid-in capital on preferred stock | 5,000 | ||

| ( To record issuance of preferred stock) | 11,500 | ||

| March 7, 2019 | Cash | 8,200 | |

| Treasury stock | 6,200 | ||

|

Additional paid-in capital on common stock | 2,000 | ||

| (To record the reissuance of treasury stock) | |||

| June 15, 2019 | No entry is required | ||

| June 15, 2019 | No entry is required | ||

|

July 2, 2019 | Retained earnings (2) | 27,440 | |

|

Common stock to be distributed | 9,800 | ||

|

Additional paid-in capital from stock dividend | 17,640 | ||

| (To record declaration of stock dividend) | |||

| August 3,2019 | Common stock to be distributed | 9,800 | |

| Common stock, $5 par | 9,800 | ||

| (To record the issuance of stock dividend) | |||

| October 1,2019 | Allowance for change in value of investment | 2,000 | |

| Unrealized increase in the value of available-for-sale of securities | 6,000 | ||

|

Gain on disposal of investment | 8,000 | ||

| (To record the declaration of property dividend) | |||

| Retained earnings | 32,000 | ||

| Property dividend payable | 32,000 | ||

| (To record the current value of the bond) | |||

| November 1,2019 | Property dividend payable | 32,000 | |

| Investment in Company L stock | 24,000 | ||

|

Allowance for change in value of investment | 8,000 | ||

| (To record the issuance of property dividend) | |||

| December 31, 2019 | Retained earnings | 53,960 | |

| Dividends payable: Preferred (3) | 12,800 | ||

| Dividends payable: Common (4) | 41,160 | ||

| (To record the declaration of annual per share dividend to the preferred and common stock) |

Table (1)

Note:

Note 1: On July 15 memorandum entry is made as the common stock split two for one and the par value is reduced from $10 to $5.

Note 2: On July 15 memorandum entry is made when treasury stock participates in the stock split. The treasury stock has 2,800 shares at a $6 par value per share costing $10.50 per share.

Working notes:

(1) Calculate the amount of dividend payable to the common stock:

(2) Calculate the amount of retained earnings:

| Particulars | Amount in $ |

| Shares issued | 42,000 |

| Less: Treasury shares (1,400 stock split for two for one) | 2,800 |

| Shares outstanding | 39,200 |

| Multiply: Stock dividend | 5% |

| Shares in stock dividend | 1,960 |

| Multiply: Current market price | $14 |

| Reduction in retained earnings | 27,440 |

Table (2)

(3) Calculate the amount of dividend payable to the preferred stock:

(4) Calculate the amount of dividend payable to the preferred stock:

2.

Prepare Company G’s statement of stockholder’s equity section for 2016.

Explanation of Solution

| Company G | |

| Shareholder's equity | |

| For the year ended December 31,2019 | |

| Particulars | Amount in $ |

| Contributed Capital: | |

| Preferred stock (8%, $100 par, 1,600 shares issued and outstanding) | 160,000 |

|

Common stock ($5 par, 43,960 shares issued of which 41,160 are outstanding and 2,800 shares are being held as treasury stock) | 219,800 |

| Additional paid-in capital on preferred stock | 31,600 |

| Additional paid-in capital on common stock | 93,000 |

| Additional paid-in capital from treasury stock | 1,800 |

| Additional paid-in capital from stock dividend | 17,640 |

| Total contributed capital | 523,840 |

|

Retained earnings (restricted in the amount of $29,400, the cost of the treasury shares) (5) | 341,600 |

| Total contributed capital, retained earnings, and donated capital | 865,440 |

| Less: Treasury stock (2,800 shares of common at $10.50 per share) | (29,400) |

| Total Shareholders’ Equity | 836,040 |

(Table 3)

(5) Calculate the amount of retained earnings:

Want to see more full solutions like this?

Chapter 16 Solutions

Intermediate Accounting: Reporting And Analysis

- Included in the December 31, 2018, Jacobi Company balance sheet was the following shareholders equity section: The company engaged in the following stock transactions during 2019: Required: 1. Prepare journal entries to record the preceding transactions. 2. Prepare the December 31, 2019, shareholders equity section (assume that 2019 net income was 270,000).arrow_forwardThe controller of Red Lake Corporation has requested assistance in determining income, basic earnings per share, and diluted earnings per share for presentation on the companys income statement for the year ended September 30, 2020. As currently calculated, Red Lakes net income is 540,000 for fiscal year 2019-2020. Your working papers disclose the following opening balances and transactions in the companys capital stock accounts during the year: 1. Common stock (at October 1, 2019, stated value 10, authorized 300,000 shares; effective December 1, 2019, stated value 5, authorized 600,000 shares): Balance, October 1, 2019issued and outstanding 60,000 shares December 1, 201960,000 shares issued in a 2-for-l stock split December 1, 2019280,000 shares (stated value 5) issued at 39 per share 2. Treasury stockcommon: March 3, 2020purchased 40,000 shares at 38 per share April 1, 2020sold 40,000 shares at 40 per share 3. Noncompensatory stock purchase warrants, Series A (initially, each warrant was exchangeable with 60 for 1 common share; effective December 1, 2019, each warrant became exchangeable for 2 common shares at 30 per share): October 1, 201925,000 warrants issued at 6 each 4. Noncompensatory stock purchase warrants, Series B (each warrant is exchangeable with 40 for 1 common share): April 1, 202020,000 warrants authorized and issued at 10 each 5. First mortgage bonds, 5%, due 2029 (nonconvertible; priced to yield 5% when issued): Balance October 1, 2019authorized, issued, and outstandingthe face value of 1,400,000 6. Convertible debentures, 7%, due 2036 (initially, each 1,000 bond was convertible at any time until maturity into 20 common shares; effective December 1, 2019, the conversion rate became 40 shares for each bond): October 1, 2019authorized and issued at their face value (no premium or discount) of 2,400,000 The following table shows the average market prices for the companys securities during 2019-2020: Adjusted for stock split Required: Prepare a schedule computing: 1. the basic earnings per share 2. the diluted earnings per share that should be presented on Red Lakes income statement for the year ended September 30, 2020 A supporting schedule computing the numbers of shares to be used in these computations should also be prepared. Assume an income tax rate of 30%.arrow_forwardAnoka Company reported the following selected items in the shareholders equity section of its balance sheet on December 31, 2019, and 2020: In addition, it listed the following selected pretax items as a December 31, 2019 and 2020: The preferred shares were outstanding during all of 2019 and 2020; annual dividends were declared and paid in each year. During 2019, 2,000 common shares were sold for cash on October 4. During 2020, a 20% stock dividend was declared and issued in early May. At the end of 2019 and 2020, the common stock was selling for 25.75 and 32.20, respectively. The company is subject to a 30% income tax rate. Required: 1. Prepare the comparative 2019 and 2020 income statements (multiple-step), and the related note that would appear in Anokas 2020 annual report. 2. Next Level Compute the price/earnings ratio for 2020. How does this compare to 2019? Why is it different?arrow_forward

- Comprehensive The shareholders equity section of Superior Corporations balance sheet as of December 31, 2018, is as follows: The following events occurred during 2019: Required: 1. Prepare journal entries for each of the above transactions. 2. Calculate the number of authorized, issued, and outstanding common shares as of December 31, 2019. 3. Calculate Superior's legal capital at December 31, 2019.arrow_forwardJumbo Corporation reported the following information about its stock on its December 31, 2018, balance sheet: Jumbo Corporation engaged in the following stock transactions during 2019: Required: 1. Does Jumbo Corporation have a simple or complex capital structure? 2. Calculate the number of shares that Jumbo would use to calculate basic EPS for its 2019 income statement.arrow_forwardMonona Company reported net income of 29,975 for 2019. During all of 2019, Monona had 1,000 shares of 10%, 100 par, nonconvertible preferred stock outstanding, on which the years dividends had been paid. At the beginning of 2019, the company had 7,000 shares of common stock outstanding. On April 2, 2019, the company issued another 2,000 shares of common stock so that 9,000 common shares were outstanding at the end of 2019. Common dividends of 17,000 had been paid during 2019. At the end of 2019, the market price per share of common stock was 17.50. Required: 1. Compute Mononas basic earnings per share for 2019. 2. Compute the price/earnings ratio for 2019.arrow_forward

- Comprehensive The following are Farrell Corporations balance sheets as of December 31, 2019, and 2018, and the statement of income and retained earnings for the year ended December 31, 2019: Additional information: a. On January 2, 2019, Farrell sold equipment costing 45,000, with a book value of 24,000, for 19,000 cash. b. On April 2, 2019, Farrell issued 1, 000 shares of common stock for 23,000 cash. c. On May 14, 2019, Farrell sold all of its treasury stock for 25,000 cash. d. On June 1, 2019, Farrell paid 50, 000 to retire bonds with a face value (and book value) of 50, 000. e. On July 2, 2019, Farrell purchased equipment for 63, 000 cash. f. On December 31, 2019, land with a fair market value of 150,000 was purchased through the issuance of a long-term note in the amount of 150,000. The note bears interest at the rate of 15% and is due on December 31, 2021. g. Deferred taxes payable represent temporary differences relating to the use of accelerated depreciation methods for income tax reporting and the straight-line method for financial statement reporting. Required: 1. Prepare a spreadsheet to support a statement of cash flows for Farrell for the year ended December 31, 2019, based on the preceding information. 2. Prepare the statement of cash flows. (Appendix 21.1) Spreadsheet and Statement Refer to the information for Farrell Corporation in P21-13. Required: 1. Using the direct method for operating cash flows, prepare a spreadsheet to support a 2019 statement of cash flows. (Hint: Combine the income statement and December 31, 2019, balance sheet items for the adjusted trial balance. Use a retained earnings balance of 291,000 in this adjusted trial balance.) 2. Prepare the statement of cash flows. (A separate schedule reconciling net income to cash provided by operating activities is not necessary.)arrow_forwardComprehensive The following are Farrell Corporations balance sheets as of December 31, 2019, and 2018, and the statement of income and retained earnings for the year ended December 31, 2019: Additional information: a. On January 2, 2019, Farrell sold equipment costing 45,000, with a book value of 24,000, for 19,000 cash. b. On April 2, 2019, Farrell issued 1,000 shares of common stock for 23,000 cash. c. On May 14, 2019, Farrell sold all of its treasury stock for 25,000 cash. d. On June 1, 2019, Farrell paid 50,000 to retire bonds with a face value (and book value) of 50,000. e. On July 2, 2019, Farrell purchased equipment for 63,000 cash. f. On December 31, 2019. land with a fair market value of 150,000 was purchased through the issuance of a long-term note in the amount of 150,000. The note bears interest at the rate of 15% and is due on December 31, 2021. g. Deferred taxes payable represent temporary differences relating to the use of accelerated depreciation methods for income tax reporting and the straight-line method for financial statement reporting. Required: 1. Prepare a spreadsheet to support a statement of cash flows for Farrell for the year ended December 31, 2019, based on the preceding information. 2. Prepare the statement of cash flows.arrow_forwardLyon Company shows the following condensed income statement information for the year ended December 31, 2019: Lyon declared dividends of 6,000 on preferred stock and 17,280 on common stock. At the beginning of 2019, 10,000 shares of common stock were outstanding. On May 1, 2019, the company issued 2,000 additional common shares, and on October 31, 2019, it issued a 20% stock dividend on its common stock. The preferred stock is not convertible. Required: 1. Compute the 2019 basic earnings per share. 2. Show the 2019 income statement disclosure of basic earnings per share. 3. Draft a related note to accompany the 2019 financial statements.arrow_forward

- Roseau Company is preparing its annual earnings per share amounts to be disclosed on its 2019 income statement. It has collected the following information at the end of 2019: 1. Net income: 120,400. Included in the net income is income from continuing operations of 130,400 and a loss from discontinued operations (net of income taxes) of 10,000. Corporate income tax rate: 30%. 2. Common stock outstanding on January 1, 2019: 20,000 shares. 3. Common stock issuances during 2019: July 6, 4,000 shares; August 24, 3,000 shares. 4. Stock dividend: On October 19, 2019, the company declared a 10% stock dividend that resulted in 2,700 additional outstanding shares of common stock. 5. Common stock prices: 2019 average market price, 30 per share; 2019 ending market price, 27 per share. 6. 7% preferred stock outstanding on January 1, 2019: 1,000 shares. Terms: 100 par, nonconvertible. Current dividends have been paid. No preferred stock issued during 2019. 7. 8% convertible preferred stock outstanding on January 1, 2019: 800 shares. The stock was issued in 2018 at 130 per share. Each 100 par preferred stock is currently convertible into 1.7 shares of common stock. Current dividends have been paid. To date, no preferred stock has been converted. 8. Bonds payable outstanding on January 1, 2019: 100,000 face value. These bonds were issued several years ago at 97 and pay annual interest of 9.6%. The discount is being amortized in the amount of 300 per year. Each 1,000 bond is currently convertible into 22 shares of common stock. To date, no bonds have been converted. 9. Compensatory share options outstanding: Key executives may currently acquire 3,000 shares of common stock at 20 per share. The options were granted in 2018. To date, none have been exercised. The unrecognized compensation cost (net of tax) related to the options is 4 per share. Required: 1. Compute the basic earnings per share. Show supporting calculations. 2. Compute the diluted earnings per share. Show supporting calculations. 3. Show how Roseau would report these earnings per share figures on its 2019 income statement. Include an explanatory note to the financial statements.arrow_forwardNet Income and Comprehensive Income At the beginning of 2019, JR Companys shareholders equity was as follows: During 2019, the following events and transactions occurred: 1. JR recognized sales revenues of 108,000. It incurred cost of goods sold of 62,000 and operating expenses of 12,000, 2. JR issued 1,000 shares of its 5 par common stock for 14 per share. 3. JR invested 30,000 in available-for-sale securities. At the end of the year, the securities had a fair value of 35,000. 4. JR paid dividends of 6,000. The income tax rate on all items of income is 30%. Required: 1. Prepare a 2019 income statement for JR which includes net income and comprehensive income ignore earnings per share). 2. For 2016 prepare a separate (a) income statement (ignore earnings per share) and (b) statement of comprehensive income.arrow_forwardOn January 1, 2019, Kittson Company had a retained earnings balance of 218,600. It is subject to a 30% corporate income tax rate. During 2019, Kittson earned net income of 67,000, and the following events occurred: 1. Cash dividends of 3 per share on 4,000 shares of common stock were declared and paid. 2. A small stock dividend was declared and issued. The dividend consisted of 600 shares of 10 par common stock. On the date of declaration, the market price of the companys common stock was 36 per share. 3. The company recalled and retired 500 shares of 100 par preferred stock. The call price was 125 per share; the stock had originally been issued for 110 per share. 4. The company discovered that it had erroneously recorded depreciation expense of 45,000 in 2018 for both financial reporting and income tax reporting. The correct depreciation for 2018 should have been 20,000. This is considered a material error. Required: 1. Prepare journal entries to record Items 1 through 4. 2. Prepare Kittsons statement of retained earnings for the year ended December 31, 2019.arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College