Videos

Find Data for Profit

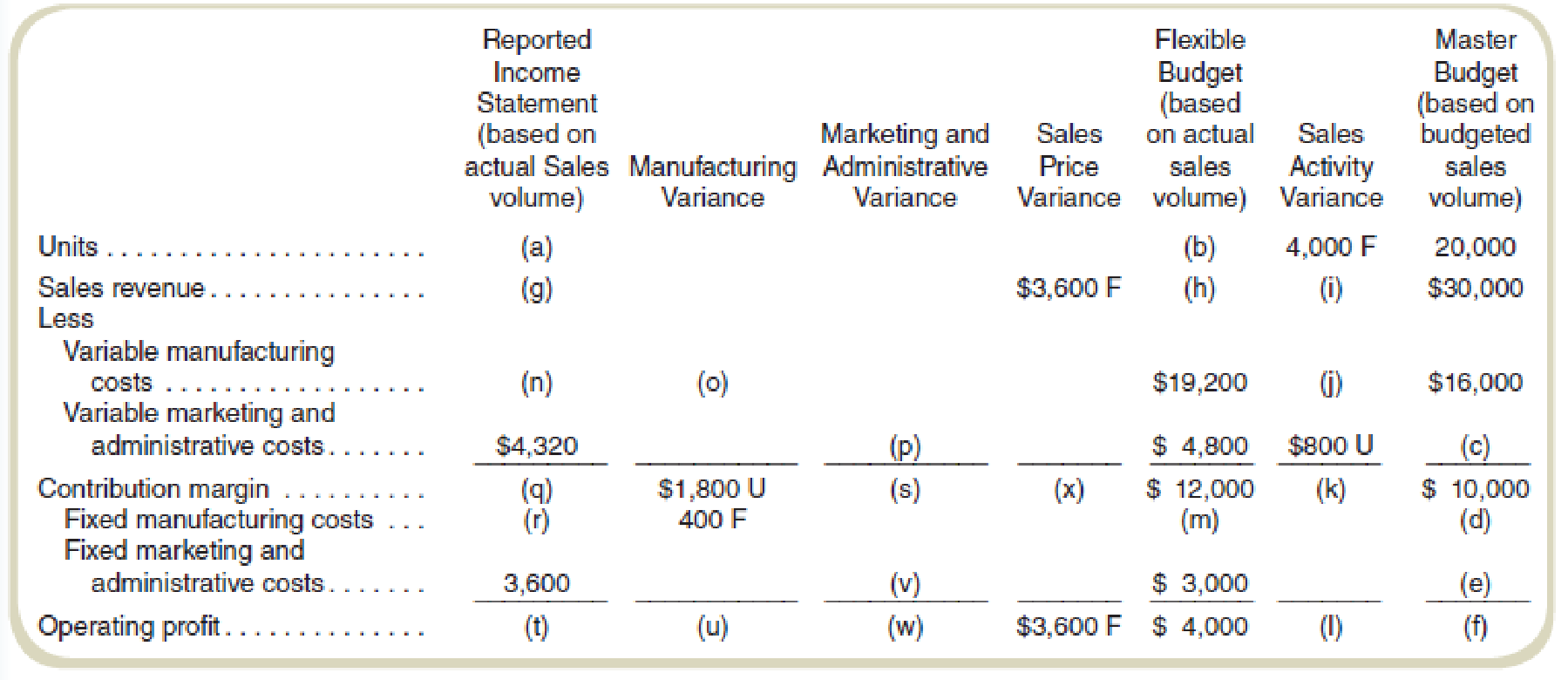

Required

Find the values of the missing items (a) through (x). Assume that actual sales volume equals actual production volume. (There are no inventory level changes.)

Find the missing data to prepare profit variance analysis.

Explanation of Solution

Profit variance analysis:

The analysis that studies the difference between the actual operating profit and the standard operating profit is called the profit variance analysis.

Prepare profit variance analysis:

| Actual Revenue & Costs | Manufacturing variance | Marketing and administrative variance | Sales price variance | Flexible budget | Sales Activity Variance | Master budget | |

| Units Produced | 24,000(1) | 24,000 | 4,000F(2) | 20,000 | |||

| Sales revenue | $39,600(7) | $3,600F | $36,000(6) | $6,000F(8) | $30,000 | ||

| Less: Variable costs | |||||||

| Manufacturing | $21,000(10) | $1,800U(9) | $19,200 | $3,200U | $16,000 | ||

| Marketing &administrative costs | $4,320 | $480F(11) | $4,800 | $800U | $4,000 | ||

| Contribution margin | $14,280(12) | $1,800U | $480F | $3,600F | $12,000 | $2,000F | $10,000 |

| Less: Fixed Costs | |||||||

| Manufacturing | $4,600(13) | $400F | $5,000(3) | $5,000 | |||

| Marketing &administrative costs | $3,600 | $600U(16) | $3,000(4) | $3,000 | |||

| Operating Profits | $6,080(14) | $1,400U(15) | $120U(17) | $3,600F | $4,000 | $2,000F | $2,000(5) |

Table: (1)

Working Note 1:

Actual units and fixed budget units:

Working Note 2:

Budgeted variable marketing and administrative cost:

Working Note 3:

Flexible budget fixed manufacturing cost:

Working Note 4:

Master budget fixed marketing and administrative cost:

Fixed cost in the master budget will be the same as given in the flexible budget which is $3,000.

Working Note 5:

Master budget operating profit:

Working Note 6:

Flexible budget sales revenue:

Working Note 7:

Actual sales revenue:

Working Note 8:

Sales activity variance:

Working Note 9:

Manufacturing variance will be equal to the total manufacturing variance which is $1,800U.

Working Note 10:

Actual variable manufacturing cost:

Working Note 11:

Marketing and administrative variance:

Working Note 12:

Contribution margin:

Working Note 13:

Actual fixed manufacturing cost:

Working Note 14:

Operating profit:

Working Note 15:

Total manufacturing variance:

Working Note 16:

Fixed marketing and administrative variance:

Working Note 17:

Total marketing and administrative variance:

Want to see more full solutions like this?

Chapter 16 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Data for Torleson Company are as follows: Required: 1. Calculate the sales price variance. 2. Calculate the sales volume variance. 3. Suppose that the product is in the introductory stage of the product life cycle. What information do these two variances provide to Torlesons managers?arrow_forwardWhat are some possible reasons for a material price variance? A. substandard material B. labor rate increases C. labor rate decreases D. labor efficiencyarrow_forwardIn comparing actual sales revenue to flexible budget sales revenue, would it be possible to have a favorable variance and still not have met revenue expectations?arrow_forward

- When is the direct labor time variance unfavorable? A. when the actual quantity used is greater than the standard quantity B. when the actual quantity used is less than the standard quantity C. when the actual price paid is greater than the standard price D. when the actual price is less than the standard pricearrow_forwardWhen is the labor rate variance unfavorable? A. when the actual quantity used is greater than the standard quantity B. when the actual quantity used is less than the standard quantity C. when the actual price paid is greater than the standard price D. when the actual price is less than the standard pricearrow_forwardWhat are some possible reasons for a labor rate variance? A. hiring of less qualified workers B. an excess of material usage C. material price increase D. utilities usage changearrow_forward

- A flexible budget______. A. predicts estimated revenues and costs at varying levels of production B. gives actual figures for selling price C. gives actual figures for variable and fixed overhead D. is not used in overhead variance calculationsarrow_forwardWhich of the following is a possible cause of an unfavorable material quantity variance? A. purchasing substandard material B. hiring higher-quality workers C. paying more than should have for workers D. purchasing too much materialarrow_forwardWhen is the labor rate variance favorable? A. when the actual quantity used is greater than the standard quantity B. when the actual quantity used is less than the standard quantity C. when the actual price paid is greater than the standard price D. when the actual price is less than the standard pricearrow_forward

- When is the direct labor time variance favorable? A. when the actual quantity used is greater than the standard quantity B. when the actual quantity used is less than the standard quantity C. when the actual price paid is greater than the standard price D. when the actual price is less than the standard pricearrow_forwardProduct costs under variable costing are typically: A. higher than under absorption costing B. lower than under absorption costing C. the same as with absorption costing D. higher than absorption costing when inventory increasesarrow_forwardWhen is the material price variance unfavorable? A. when the actual quantity used is greater than the standard quantity B. when the actual quantity used is less than the standard quantity C. when the actual price paid is greater than the standard price D. when the actual price is less than the standard pricearrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning