Videos

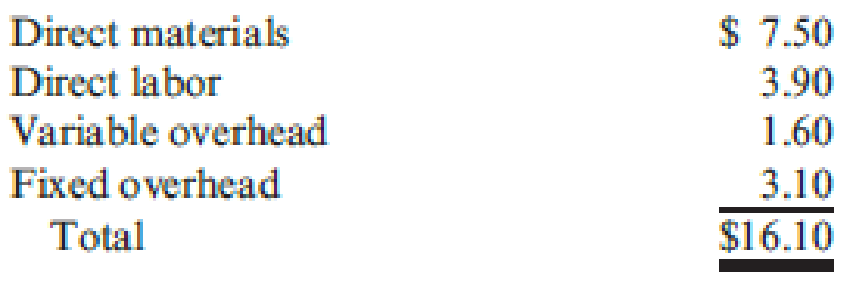

Feinan Sports, Inc., manufactures sporting equipment, including weight-lifting gloves. A national sporting goods chain recently submitted a special order for 4,600 pairs of weight-lifting gloves. Feinan Sports was not operating at capacity and could use the extra business. Unfortunately, the order’s offering price of $12.80 per pair was below the cost to produce them. The controller was opposed to taking a loss on the deal. However, the personnel manager argued in favor of accepting the order even though a loss would be incurred; it would avoid the problem of layoffs and would help maintain the community image of the company. The full cost to produce a pair of weight-lifting gloves is presented below.

No variable selling or administrative expenses would be associated with the order. Non-unit-level activity costs are a small percentage of total costs and are therefore not considered.

Required:

- 1. Assume that the company would accept the order only if it increased total profits. Should the company accept or reject the order? Provide supporting computations.

- 2. Suppose that Feinan Sports has negotiated with the potential customer, and has determined that it can substitute cheaper materials, reducing direct materials cost by $0.95 per unit. In addition, the company’s engineers have found a way to reduce direct labor cost by $0.50 per unit. Should the company accept or reject the order? Provide supporting computations.

- 3. Consider the personnel manager’s concerns. Discuss the merits of accepting the order even if it decreases total profits.

Trending nowThis is a popular solution!

Chapter 17 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Bienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.arrow_forwardBoston Executive. Inc., produces executive limousines and currently manufactures the mini-bar inset at these costs: The company received an offer from Elite Mini-Bars to produce the insets for $2,100 per Unit and supply 1,000 mini-bars for the coming years estimated production. If the company accepts this offer and shuts down production of this part of the business, production workers and supervisors will be reassigned to other areas. Assume that for the short-term decision-making process demonstrated in this problem, the companys total labor costs (direct labor and supervisor salaries) will remain the same if the bar inserts are purchased. The specialized equipment cannot be used and has no market value. However, the space occupied by the mini bar production can be used by a different production group that will lease it for $55,000 per year. Should the company make or buy the mini-bar insert?arrow_forwardTania Company manufactures watches. A national sporting goods chain recentlysubmitted a special order for 4,000 sport watches. Tania was not operating at capacityand could use the extra business. Unfortunately, the order’s offering price of RM17 perwatch was below the cost to produce the watches. The controller did not agree to take aloss on the deal. However, the personnel manager argued in favor of accepting theorder even though a loss would be incurred: it would avoid the problems of layoff andwould help maintain the community image of the company. The following informationis the full cost to produce a sport watch:Table 6: Production CostsDetails Unit CostRMDirect materials 6.50Direct labor 5.00Variable overhead 3.25Fixed overhead 2.50Total 17.25 List the relevant costs of the two alternatives of the special order. (ii) Propose whether operating income increase or decrease if the order is acceptedarrow_forward

- Intercontinental Chemical Company, located in Buenos Aires, Argentina, recently received an order for a product it does not normally produce. Since the company has excess production capacity, management is considering accepting the order. In analyzing the decision, the assistant controller is compiling the relevant costs of producing the order. Production of the special order would require 8,000 kilograms of theolite. Intercontinental does not use theolite for its regular product, but the firm has 8,000 kilograms of the chemical on hand from the days when it used theolite regularly. The theolite could be sold to a chemical wholesaler for 14,500 p. The book value of the theolite is 2.00 p per kilogram. Intercontinental could buy theolite for 2.40 p per kilogram. (p denotes the peso, Argentina’s national monetary unit. Many countries use the peso as their unit of currency. On the day this exercise was written, Argentina’s peso was worth 0.104 U.S. dollar.) Required: 1-a. What is the…arrow_forwardIntercontinental Chemical Company, located in Buenos Aires, Argentina, recently received an order for a product it does not normally produce. Since the company has excess production capacity, management is considering accepting the order. In analyzing the decision, the assistant controller is compiling the relevant costs of producing the order. Production of the special order would require 8,000 kilograms of theolite. Intercontinental does not use theolite for its regular product, but the firm has 8,000 kilograms of the chemical on hand from the days when it used theolite regularly. The theolite could be sold to a chemical wholesaler for 14,500 p. The book value of the theolite is 2.00 p per kilogram. Intercontinental could buy theolite for 2.40 p per kilogram. ( p denotes the peso, Argentina’s national monetary unit. Many countries use the peso as their unit of currency. On the day this exercise was written, Argentina’speso was worth .104 U.S. dollar.) Required:1. What is the relevant…arrow_forwardNorton Industries, a manufacturer of electronic parts, has recently received an invitation to bid on a special order for 20,000 units of one of its most popular products. Norton currently manufactures 40,000 units of this product in its Loveland, Ohio, plant. The plant is operating at 50% capacity. There will be no marketing costs on the special order. The sales manager of Norton wants to set the bid at $7 per unit because she is sure that Norton will get the business at that price. Others on the executive committee of the firm object, saying that Norton would lose money on the special order at that price. Units 40,000Manufacturing CostsDirect Materials $ 90,000Direct Labor 100,000Factory Overhead 260,000*Total Manufacturing Cost $ 450,000Unit Cost…arrow_forward

- McAfee Industries, a manufacturer of electronic parts, has recently received an invitation to bid on a special order for 20,000 units of one of its most popular products. McAfee currently manufactures 40,000 units of this product in its Boston, Massachusets, plant. The plant is operating at 50% capacity. There will be no marketing costs on the special order. The sales manager of McAfee wants to set the bid at $7 per unit because she is sure that McAfee will get the business at that price. Others on the executive committee of the firm object, saying that McAfee would lose money on the special order at that price. Table attached Required Should McAfee accept the invitation to bid? Explain What would be the impact on short- term operating income if the order is accepted at the price recommended by the sales manager? Suppose that McAfee’s distribution center at the warehouse is operating at full capacity and would need to add capacity (leasing additional warehouse) costing $6,000 for…arrow_forwardCapitol, Incorporated has received a special order for 2,000 units of its product at a special price of $195. The product normally sells for $260 and has the following manufacturing costs: Cost per Unit Direct materials $ 78 Direct labor 52 Variable manufacturing overhead 39 Fixed manufacturing overhead 65 Total unit cost $ 234 Assume that Capitol has sufficient capacity to fill the order without harming normal production and sales. Required: If Capitol accepts the order, what effect will the order have on the company’s short-term profit? What minimum unit price should Capitol charge to achieve a $65,000 incremental profit? Now, assume Capitol is currently operating at full capacity and cannot fill the order without harming normal production and sales. If Capitol accepts the order, what effect will the order have on the company’s short-term profit?arrow_forwardBefore Coronado could give Langston's Landscape Company an answer, the company received a special order from Benson Building & Supply for 13,500 fireplaces. Benson is willing to pay $67 per fireplace but it wants a special design imbedded into the fireplace that increases cost of goods sold by $55,350. The special design also requires the purchase of a part that costs $5,500 and will have no future use for Coronado Company. Benson Building & Supply will pick up the fireplaces so no shipping costs are involved. Due to capacity limitations, Coronado cannot accept both special orders. Which order should be accepted? Document your decision by preparing an incremental analysis for Benson's order. (Enter loss using either a negative sign preceding the number e.g. -2,945 or parentheses e.g. (2,945).)arrow_forward

- Jireh Limited also manufactures prefab components for the housing industry. They have just been offered a new four year contract to supply a component, subject to them meeting certain quality requirements set by GREDA Ghana. The production manager is concerned that the current machine, which has been fully depreciated, will not be able to meet the stringent quality controls that will be required because the technology is obsolete, and the machine is unreliable. The company currently spends £50,000 per year to maintain and operate this machine which has no secondhand market value. On the basis of the production managerʼs recommendation, management has decided to replace the current machine. It is estimated that the replacement machine will cost £1 million with a four-year useful life. The companyʼs depreciation policy is to use a 20% reducing balance method over the life of the asset. As part of the purchase agreement for the new machine, the suppliers are offering a special maintenance…arrow_forwardFusion Metals Company is considering the elimination of its Packaging Department. Management has received an offer from an outside firm to supply all Fusion’s packaging needs. To help her in making the decision, Fusion’s president has asked the controller for an analysis of the cost of running Fusion’s Packaging Department. Included in that analysis is $9,100 of rent, which represents the Packaging Department’s allocation of the rent on Fusion’s factory building. If the Packaging Department is eliminated,the space it used will be converted to storage space. Currently Fusion rents storage space in a nearby warehouse for $11,000 per year. The warehouse rental would no longer be necessary if the Packaging Department were eliminated. Required:1. Discuss each of the figures given in the exercise with regard to its relevance in the departmentclosing decision.2. What type of cost is the $11,000 warehouse rental, from the viewpoint of the costs of the Packaging Department?arrow_forwardThe company has an offer from Duvall Valves to produce the part for $2,000 per unit and supply 1,000 valves (the number needed in the coming year). If the company accepts this offer and shuts down production of valves, production workers and supervisors will be reassigned to other areas. The equipment cannot be used elsewhere in the company, and it has no market value. However, the space occupied by the production of the valve can be used by another production group that is currently leasing space for $55,000 per year. What is the incremental savings of buying the valves? (The answer should be stated in a per-unit format and is a positive number)arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College