Financial And Managerial Accounting

15th Edition

ISBN: 9781337902663

Author: WARREN, Carl S.

Publisher: Cengage Learning,

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

thumb_up100%

Chapter 19, Problem 1PA

Support department cost allocation

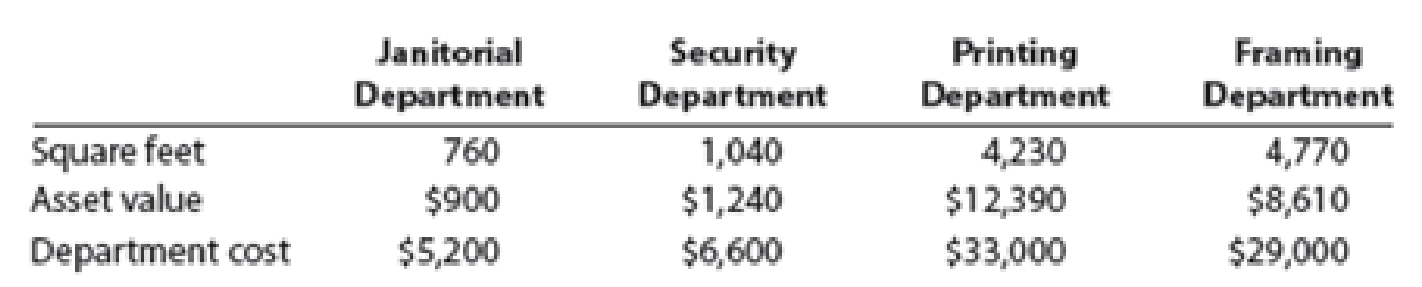

Blue Mountain Masterpieces produces pictures, paintings, and other home decor. The Printing and Framing production departments are supported by the Janitorial and Security departments. Janitorial costs are allocated to the production departments based on square feet, and security costs are allocated based on asset value. Information about these departments is detailed in the following table:

Management has experimented with different support department cost allocation methods in the past. The different allocation methods did not yield large differences of cost allocation to the production departments.

Instructions

- 1. Determine which support department cost allocation method Blue Mountain Masterpieces would most likely use to allocate its support department costs to the production departments.

- 2. Determine the total costs allocated from each support department to each production department using the method you determined in part (1).

- 3. Without doing calculations, consider and answer the following: If Blue Mountain Masterpieces decided to use square feet instead of asset value as the cost driver for security services, how would this change the allocation of Security Department costs?

Expert Solution & Answer

Trending nowThis is a popular solution!

Chapter 19 Solutions

Financial And Managerial Accounting

Ch. 19 - Why are support department costs difficult to...Ch. 19 - Why does support department cost allocation matter...Ch. 19 - What are some drawbacks of applying support...Ch. 19 - Why is the diect method of support department cost...Ch. 19 - How does management determine the order in which...Ch. 19 - Are large or small companies more likely to use...Ch. 19 - What is the main difference between the physical...Ch. 19 - When would management most likely use the net...Ch. 19 - What are the two most often used ways of...Ch. 19 - How can support department and joint cost...

Ch. 19 - Charlies Wood Works produces wood products (e.g.,...Ch. 19 - Bucknum Boys, Inc., produces hunting gear for buck...Ch. 19 - Brewster Toymakers Inc. produces toys for...Ch. 19 - Prob. 4BECh. 19 - Garys Grooves Co. produces two types of carving...Ch. 19 - Man OFort Inc. produces two different styles of...Ch. 19 - Yo-Down Inc. produces yogurt. Information related...Ch. 19 - Snowy River Stallion Inc. produces horse and...Ch. 19 - Blue Africa Inc. produces laptops and desktop...Ch. 19 - Christmas Timber, Inc., produces Christmas trees....Ch. 19 - Crystal Scarves Co. produces winter scarves. The...Ch. 19 - Davis Snowflake Co. produces Christmas stockings...Ch. 19 - Becker Tabletops has two support departments...Ch. 19 - Becker Tabletops has two support departments...Ch. 19 - Becker Tabletops has two support departments...Ch. 19 - Support department cost allocation comparison...Ch. 19 - Board-It, Inc., produces the following types of 2 ...Ch. 19 - Prob. 12ECh. 19 - Joint cost allocation market value at split-off...Ch. 19 - Joint cost allocation net realizable value method...Ch. 19 - Big Als Inc. produces and sells various cuts of...Ch. 19 - Gordons Smoothie Stand makes three types of...Ch. 19 - Joint cost allocation-market value at split-off...Ch. 19 - Joint cost allocation net realizable value method...Ch. 19 - Support department cost allocation Blue Mountain...Ch. 19 - Support activity cost allocation Jakes Gems mines...Ch. 19 - Joint cost allocation Lovely Lotion Inc. produces...Ch. 19 - Joint cost allocation Florissas Flowers jointly...Ch. 19 - Support department cost allocation Hooligan...Ch. 19 - Support activity cost allocation Kizzles Crepes...Ch. 19 - Joint cost allocation McKenzies Soap Sensations,...Ch. 19 - Joint cost allocation Rosies Roses produces three...Ch. 19 - Analyze Milkrageous, Inc. Milkragcous, Inc., a...Ch. 19 - Analyze Horsepower Hookup, Inc. Horsepower Hookup,...Ch. 19 - Prob. 3MADCh. 19 - Analyze Williams Ball Jersey Shop Williams Ball ...Ch. 19 - Prob. 1TIFCh. 19 - Prob. 3TIFCh. 19 - Logo Inc. has two data services departments...Ch. 19 - Adam Corporation manufactures computer tables and...Ch. 19 - Breegle Company produces three products (B-40,...Ch. 19 - Tucariz Company processes Duo into two joint...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Overhead Rates, Unit Costs Folsom Company manufactures specialty tools to customer order. There are three producing departments. Departmental information on budgeted overhead and various activity measures for the coming year is as follows: Currently, overhead is applied on the basis of machine hours using a plantwide rate. However, Janine, the controller, has been wondering whether it might be worthwhile to use departmental overhead rates. She has analyzed the overhead costs and drivers for the various departments and decided that Welding and Finishing should base their overhead rates on machine hours and that Assembly should base its overhead rate on direct labor hours. Janine has been asked to prepare bids for two jobs with the following information: The typical bid price includes a 35% markup over full manufacturing cost. Round all overhead rates to the nearest cent. Round all bid prices to the nearest dollar. Required: 1. Calculate a plantwide rate for Folsom Company based on machine hours. What is the bid price of each job using this rate? 2. Calculate departmental overhead rates for the producing departments. What is the bid price of each job using these rates?arrow_forwardActivity cost pools, activity rates, and product costs using activity-based costing Caldwell Home Appliances Inc. is estimating the activity cost associated with producing ovens and refrigerators. The indirect labor can be traced into four separate activity pools, based on time records provided by the employees. The budgeted activity cost and activity-base information are provided as follows: The estimated activity-base usage and unit information for two product lines was determined as follows: A. Determine the activity rate for each activity cost pool. B. Determine the activity-based cost per unit of each product.arrow_forwardCharlies Wood Works produces wood products (e.g., cabinets, tables, picture frames, and so on). Production departments include Cutting and Assembly. The Janitorial and Security departments support the Cutting and Assembly departments. The Assembly Department spans about 46,400 square feet and holds assets valued at about 60,000. The Cutting Department spans about 33,600 square feet and holds assets valued at about 140,000. Charlies Wood Works allocates support department costs using the direct method. If costs from the Janitorial Department are allocated based on square feet and costs from the Security Department are allocated based on asset value, determine (a) the percentage of Janitorial costs that should be allocated to the Assembly Department and (b) the percentage of Security costs that should be allocated to the Cutting Department.arrow_forward

- Tom Young, vice president of Dunn Company (a producer of plastic products), has been supervising the implementation of an activity-based cost management system. One of Toms objectives is to improve process efficiency by improving the activities that define the processes. To illustrate the potential of the new system to the president, Tom has decided to focus on two processes: production and customer service. Within each process, one activity will be selected for improvement: molding for production and sustaining engineering for customer service. (Sustaining engineers are responsible for redesigning products based on customer needs and feedback.) Value-added standards are identified for each activity. For molding, the value-added standard calls for nine pounds per mold. (Although the products differ in shape and function, their size, as measured by weight, is uniform.) The value-added standard is based on the elimination of all waste due to defective molds (materials is by far the major cost for the molding activity). The standard price for molding is 15 per pound. For sustaining engineering, the standard is 60 percent of current practical activity capacity. This standard is based on the fact that about 40 percent of the complaints have to do with design features that could have been avoided or anticipated by the company. Current practical capacity (the first year) is defined by the following requirements: 18,000 engineering hours for each product group that has been on the market or in development for five years or less, and 7,200 hours per product group of more than five years. Four product groups have less than five years experience, and 10 product groups have more. There are 72 engineers, each paid a salary of 70,000. Each engineer can provide 2,000 hours of service per year. There are no other significant costs for the engineering activity. For the first year, actual pounds used for molding were 25 percent above the level called for by the value-added standard; engineering usage was 138,000 hours. There were 240,000 units of output produced. Tom and the operational managers have selected some improvement measures that promise to reduce non-value-added activity usage by 30 percent in the second year. Selected actual results achieved for the second year are as follows: The actual prices paid per pound and per engineering hour are identical to the standard or budgeted prices. Required: 1. For the first year, calculate the non-value-added usage and costs for molding and sustaining engineering. Also, calculate the cost of unused capacity for the engineering activity. 2. Using the targeted reduction, establish kaizen standards for molding and engineering (for the second year). 3. Using the kaizen standards prepared in Requirement 2, compute the second-year usage variances, expressed in both physical and financial measures, for molding and engineering. (For engineering, explain why it is necessary to compare actual resource usage with the kaizen standard.) Comment on the companys ability to achieve its targeted reductions. In particular, discuss what measures the company must take to capture any realized reductions in resource usage.arrow_forwardBecker Tabletops has two support departments (Janitorial and Cafeteria) and two production departments (Cutting and Assembly). Relevant details for these departments are as follows: Allocate the support department costs to the production departments using the direct method.arrow_forwardClassify the following cost drivers as structural, executional, or operational. a. Number of plants b. Number of moves c. Degree of employee involvement d. Capacity utilization e. Number of product lines f. Number of distribution channels g. Engineering hours h. Direct labor hours i. Scope j. Product configuration k. Quality management approach l. Number of receiving orders m. Number of defective units n. Employee experience o. Types of process technologies p. Number of purchase orders q. Type and efficiency of layout r. Scale s. Number of functional departments t. Number of planning meetingsarrow_forward

- Refer to the data in Exercise 7.18. When the capacity of the HR Department was originally established, the normal usage expected for each department was 20,000 direct labor hours. This usage is also the amount of activity planned for the two departments in Year 1 and Year 2. Required: 1. Allocate the costs of the HR Department using the direct method and assuming that the purpose is product costing. 2. Allocate the costs of the HR Department using the direct method and assuming that the purpose is to evaluate performance.arrow_forwardPelder Products Company manufactures two types of engineering diagnostic equipment used in construction. The two products are based upon different technologies, X-ray and ultrasound, but are manufactured in the same factory. Pelder has computed the manufacturing cost of the X-ray and ultrasound products by adding together direct materials, direct labor, and overhead cost applied based on the number of direct labor hours. The factory has three overhead departments that support the single production line that makes both products. Budgeted overhead spending for the departments is as follows: Pelders budgeted manufacturing activities and costs for the period are as follows: The budgeted cost to manufacture one ultrasound machine using the activity-based costing method is: a. 225. b. 264. c. 293. d. 305.arrow_forwardThe actions listed next are associated with either an activity-based operational control system or a traditional operational control system: a. Budgeted costs for the maintenance department are compared with the actual costs of the maintenance department. b. The maintenance department manager receives a bonus for beating budget. c. The costs of resources are traced to activities and then to products. d. The purchasing department is set up as a responsibility center. e. Activities are identified and listed. f. Activities are categorized as adding or not adding value to the organization. g. A standard for a products material usage cost is set and compared against the products actual materials usage cost. h. The cost of performing an activity is tracked over time. i. The distance between moves is identified as the cause of materials handling cost. j. A purchasing agent is rewarded for buying parts below the standard price set by the company. k. The cost of the materials handling activity is reduced dramatically by redesigning the plant layout. l. An investigation is undertaken to find out why the actual labor cost for the production of 1,000 units is greater than the labor standard allowed. m. The percentage of defective units is calculated and tracked over time. n. Engineering has been given the charge to find a way to reduce setup time by 75 percent. o. The manager of the receiving department lays off two receiving clerks so that the fourth-quarter budget can be met. Required: Classify the preceding actions as belonging to either an activity-based operational control system or a traditional control system. Explain why you classified each action as you did.arrow_forward

- The controller of the South Charleston plant of Ravinia, Inc., monitored activities associated with materials handling costs. The high and low levels of resource usage occurred in September and March for three different resources associated with materials handling. The number of moves is the driver. The total costs of the three resources and the activity output, as measured by moves for the two different levels, are presented as follows: Required: 1. Determine the cost behavior formula of each resource. Use the high-low method to assess the fixed and variable components. 2. Using your knowledge of cost behavior, predict the cost of each item for an activity output level of 9,000 moves. 3. Construct a cost formula that can be used to predict the total cost of the three resources combined. Using this formula, predict the total materials handling cost if activity output is 9,000 moves. In general, when can cost formulas be combined to form a single cost formula?arrow_forwardActivity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loudspeakers. The factory overhead incurred is as follows: The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: The activity-base usage quantities and units produced for the two products follow: Instructions Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. Determine the total and per-unit cost assigned to each product under activity-based costing. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods. production department factory overhead rate and activity-based costing methods.arrow_forwardCommunication The controller of New Wave Sounds Inc. prepared the following product profitability report for management, using activity-based costing methods for allocating both the factory overhead and the marketing expenses. As such, the controller has confidence in the accuracy of this report. In addition, the controller interviewed the vice president of marketing, who provided the following insight into the companys three products: The home theater speakers are an older product that is highly recognized in the marketplace. The wireless speakers are a new product that was just recently launched. The wireless headphones are a new technology that has no competition in the marketplace, and it is hoped that they will become an important future addition to the companys product portfolio. Initial indications are that the product is well received by customers. The controller believes that the manufacturing costs for all three products are in line with expectations. Based on the information provided: 1. Calculate the ratio of gross profit to sales and the ratio of operating income to sales for each product. 2. Write a brief (one-page) memo using the product profitability report and the calculations in (a) to make recommendations to management with respect to strategies for the three products.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College PubFinancial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College PubFinancial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

What is Cost Allocation? Definition & Process; Author: FloQast;https://www.youtube.com/watch?v=hLhvvHvZ3JM;License: Standard Youtube License