Financial And Managerial Accounting

15th Edition

ISBN: 9781337902663

Author: WARREN, Carl S.

Publisher: Cengage Learning,

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 23, Problem 2MAD

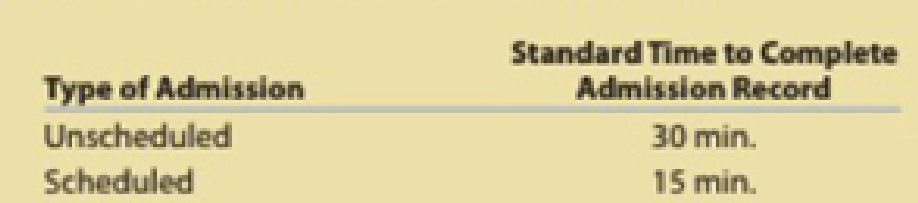

Admissions time variance

Valley Hospital began using standards to evaluate its Admissions Department. The standard was broken into two types of admissions as follows:

The unscheduled admission took longer because name, address, and insurance information needed to be determined and verified at the time of admission. Information was collected on scheduled admissions prior to admitting the patient, thus requiring less time in admissions.

The Admissions Department employs four full-time people for 40 hours per week at $15 per hour. For the most recent week, the department handled 140 unscheduled and 340 scheduled admissions.

- a. How much was actually spent on labor for the week?

- b. What are the standard hours for the actual volume of work for the week?

- c. Compute the direct labor time variance, and report how well the department performed for the week.

- d. What are some factors that may cause an unfavorable direct labor time variance for the Admissions Department?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Critique a Variance Report

The Terminator Inc. provides on-site residential pest extermination services. The company bas several mobile teams who are dispatched from a central location in company-owned trucks. The company uses the number of jobs to measure activity. At the beginning of April, the company budgeted for 100 jobs, but the actual number of jobs turned out to be 105. A report comparing the budgeted revenues and costs to the actual revenues and costs appears below:

Required:

Is the above variance report useful for evaluating how well revenues and costs were controlled during April? Why or Why not?

determine the enrollment variance for a month

determine the utilization variance for the month

determine the efficiency variance for the month

the dermatology clinic expects to contract with an HMO tof an estimated 80000 enrollee. the HMO expecys 1 in 4 of its enrolled members to use the dermatology services per month.

at the end of he year the clinic saw monthly figures that the number of enrolled members had increased by 5% over the budgeted amount and that 1 in 3 total HMO members had used services per month

budgeted

actual

enrollees

80000

84000

usage rate

0.25

0.333

visits

20000

28000

cost

200000

270000

cost per visit

10

9.643

Variance Analysis In a Hospital

John Fleming, chief administrator for Valley View Hospital, is concerned about the costs for tests in the hospital’s lab. Charges for lab tests are consistently higher at Valley View than at other hospitals and have resulted in many complaints. Also, because of strict regulations on amounts reimbursed for lab tests, payments received from insurance companies and governmental units have not been high enough to cover lab costs.

Mr. Fleming has asked you to evaluate costs in the hospital’s lab for the past month. The following information is available:

a. Two types of tests are performed in the lab—blood tests and smears. During the past month, 1,800 blood tests and 2,400 smears were performed in the lab.

b. Small glass plates are used in both types of tests. During the past month, the hospital purchased 12,000 plates at a cost of $56,400. 1,500 of these plates were unused at the end of the month: no plates were on hand at the beginning of the month.

c.…

Chapter 23 Solutions

Financial And Managerial Accounting

Ch. 23 - What are the basic objectives in the use of...Ch. 23 - What is meant by reporting by the principle of...Ch. 23 - Prob. 3DQCh. 23 - Prob. 4DQCh. 23 - A. What are the two variances between the actual...Ch. 23 - A new assistant controller recently was heard to...Ch. 23 - Would the use of standards be appropriate in a...Ch. 23 - Prob. 8DQCh. 23 - At the end of the period, the factory overhead...Ch. 23 - If variances are recorded in the accounts at the...

Ch. 23 - Direct materials variances Bellingham Company...Ch. 23 - Direct labor variances Bellingham Company produces...Ch. 23 - Factory overhead controllable variance Bellingham...Ch. 23 - Factory overhead volume variance Bellingham...Ch. 23 - Standard cost journal entries Bellingham Company...Ch. 23 - Income statement with variances Prepare an income...Ch. 23 - Crazy Delicious Inc. produces chocolate bars. The...Ch. 23 - Atlas Furniture Company manufactures designer home...Ch. 23 - Salisbury Bottle Company manufactures plastic...Ch. 23 - The following data relate to the direct materials...Ch. 23 - De Soto Inc. produces tablet computers. The...Ch. 23 - Standard direct materials cost per unit from...Ch. 23 - H.J. Heinz Company uses standards to control its...Ch. 23 - Direct labor variances The following data relate...Ch. 23 - Glacier Bicycle Company manufactures commuter...Ch. 23 - Ada Clothes Company produced 40,000 units during...Ch. 23 - Mexicali On the Go Inc. owns and operates food...Ch. 23 - Direct materials and direct labor variances At the...Ch. 23 - Flexible overhead budget Leno Manufacturing...Ch. 23 - Flexible overhead budget Wiki Wiki Company has...Ch. 23 - Factory overhead cost variances The following data...Ch. 23 - Thomas Textiles Corporation began November with a...Ch. 23 - Prob. 17ECh. 23 - Factory overhead cost variance report Tannin...Ch. 23 - Recording standards in accounts Cioffi...Ch. 23 - Prob. 20ECh. 23 - Income statement indicating standard cost...Ch. 23 - Rockport Industries Inc. gathered the following...Ch. 23 - Dickinsen Company gathered the following data for...Ch. 23 - Rosenberry Company computed the following revenue...Ch. 23 - Lowell Manufacturing Inc. has a normal selling...Ch. 23 - Shasta Fixture Company manufactures faucets in a...Ch. 23 - Flexible budgeting and variance analysis I Love My...Ch. 23 - Direct materials, direct labor, and factory...Ch. 23 - Factory overhead cost variance report Tiger...Ch. 23 - CodeHead Software Inc. does software development....Ch. 23 - Direct materials and direct labor variance...Ch. 23 - Flexible budgeting and variance analysis Im Really...Ch. 23 - Direct materials, direct labor, and factory...Ch. 23 - Factory overhead cost variance report Feeling...Ch. 23 - Prob. 5PBCh. 23 - Prob. 1COMPCh. 23 - Advent Software uses standards to manage the cost...Ch. 23 - Admissions time variance Valley Hospital began...Ch. 23 - United States Postal Service: Mail sorting time...Ch. 23 - Direct labor time variance Maywood City Police...Ch. 23 - Ethics in action Dash Riprock is a cost analyst...Ch. 23 - Variance interpretation Vanadium Audio Inc. is a...Ch. 23 - MinnOil performs oil changes and other minor...Ch. 23 - Prob. 2CMACh. 23 - Frisco Company recently purchased 108,000 units of...Ch. 23 - JoyT Company manufactures Maxi Dolls for sale in...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- United States Postal Service: Mail sorting time variance One of the operations in the United States Postal Service is a mechanical mail sorting operation. In this operation, handwritten letter mail is sorted at a rate of 1.5 letters per second. An operator sitting at a keyboard mechanically sorts the letter from a three-digit code. The manager of the mechanical sorting operation wishes to determine the number of temporary employees to hire for December. The manager estimates that there will be an additional 24,192,000 pieces of mail in December, due to the upcoming holiday season. Assume that the sorting operators are temporary employees. The union contract requires that temporary employees be hired for one month at a time. Each temporary employee is hired to work 160 hours in the month. A. How many temporary employees should the manager hire for December? B. If each temporary employee earns a standard 17 per hour, what would be the direct labor time variance if the actual number of additional letters sorted in December was 23,895,000?arrow_forwardFactory overhead cost variance report Feeling Better Medical Inc., a manufacturer of disposable medical supplies, prepared the following factory overhead cost budget for the Assembly Department for October of the current year. The company expected to operate the department at 100% of normal capacity of 30,000 hours. During October, the department operated at 28,500 hours, and the factory overhead costs incurred were indirect factory wages, 234,000; power and light, 178,500; indirect materials, 50,600; supervisory salaries, 126,000; depreciation of plant and equipment, 70,000; and insurance and property taxes, 44,000. Instructions Prepare a factory overhead cost variance report for October. To be useful for cost control, the budgeted amounts should be based on 28,500 hours.arrow_forwardFactory overhead cost variance report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 20,000 hours for production: Tannin has available 25,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 22,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Construct a factory overhead cost variance report for the Trim Department for July.arrow_forward

- Calculating factory overhead: two variances Monrovia Manufacturing Inc. normally produces 10,000 units of product A each month. Each unit requires 4 hours of direct labor, and factory overhead is applied on a direct labor hour basis. Fixed costs and variable costs in factory overhead at the normal capacity are 10 and 5 per unit, respectively. Cost and production data for June follow: a. Calculate the flexible-budget variance. b. Calculate the production-volume variance. c. Was the total factory overhead under- or overapplied? By what amount?arrow_forwardDirect labor time variance Maywood City Police uses variance analysis to monitor police staffing. The following table identifies three common police activities, the standard time to perform each activity, and their actual frequency to establish the expected cost to serve these activities. The police are paid 25 per hour. The actual amount of hours per activity for the year were as follows: A. Determine the total budgeted cost to perform the three police activities. B. Determine the total actual cost to perform the three police activities. C. Determine the direct labor time variance. D. What does the time variance suggest?arrow_forwardCalculating factory overhead: two variances Munoz Manufacturing Co. normally produces 10,000 units of product X each month. Each unit requires 2 hours of direct labor, and factory overhead is applied on a direct labor hour basis. Fixed costs and variable costs in factory overhead at the normal capacity are 2.50 and 1.50 per direct labor hour, respectively. Cost and production data for May follow: a. Calculate the flexible-budget variance. b. Calculate the production-volume variance. c. Was the total factory overhead under- or overapplied? By what amount?arrow_forward

- Materials and labor variances Branca Inspections Inc. specializes in determining whether a building or houses drainpipes are properly tied into the citys sewer system. The company pours colored chemical through the pipes and collects an inspection sample from each outlet, which is then analyzed. Each job should take 15 hours for each of four inspectors, at a standard rate of 18 per hour. Each job requires a standard quantity of 5 gallons of Glow (a colored chemical), which should cost 25 per gallon. Data from the companys most recent job (a building) follow: Required: Compute the following variances, using the formulas on pages 421422 and 424: 1. Materials price and quantity variances. 2. Labor rate and efficiency variances.arrow_forwardDirect labor time variance Maywood City Police uses variance analysis to monitor police staffing. The following table identifies three common police activities, the standard time to perform each activity, and their actual frequency to establish the expected cost to serve these activities. Police Activity Standard Hours per Activity Actual Activities for Year Total Employee Hours Theft 0.60 7,000 4,200 Arrest 1.50 18,000 27,000 Patrol activities 0.30 9,000 2,700 33,900 The police are paid 25 per hour. The actual amount of hours per activity for the year were as follows: Police Activity Actual Hours per Activity Theft 0.75 Arrest 2.00 Patrol activities 0.40 A. Determine the total budgeted cost to perform the three police activities. B. Determine the total actual cost to perform the three police activities. C. Determine the direct labor time variance. D. What does the time variance suggest?arrow_forwardStatic budget versus flexible budget The production supervisor of the Machining Department for Hagerstown Company agreed to the following monthly static budget for the upcoming year: The actual amount spent and the actual units produced in the first three months in the Machining Department were as follows: The Machining Department supervisor has been very pleased with this performance because actual expenditures for May-July have been significantly less than the monthly static budget of2,358,000. However, the plant manager believes that the budget should not remain fixed for every month but should flex or adjust to the volume of work that is produced in the Machining Department. Additional budget information for the Machining Department is as follows: a. Prepare a flexible budget for the actual units produced for May, June, and July in the MachiningDepartment. Assume depreciation is a fixed cost. b. Compare the flexible budget with the actual expenditures for the first three months.What does this comparison suggest?arrow_forward

- Calculating amount of factory overhead applied to work in process The overhead application rate for a company is 2.50 per unit, made up of 1.00 for fixed overhead and 1.50 for variable overhead. Normal capacity is 10,000 units. In one month, there was an unfavorable flexible budget variance of 200. Actual overhead for the month was 27,000. What was the amount of the budgeted overhead for the actual level of production?arrow_forwardDetermining Budgeted Overhead The overhead application rate for a company is 10 per unit, made up of 6 per unit of fixed overhead and 4 per unit of variable overhead. Normal capacity is 10,000 units. In one month there was a favorable flexible budget variance of 2,500. Actual overhead for the month was 110,000 and actual units produced were 13,125. Based on this information, determine the amount of the budgeted overhead for the actual level of production.arrow_forwardFactory overhead cost variance report Tiger Equipment Inc., a manufacturer of construction equipment, prepared the following factory overhead cost budget for the Welding Department for May of the current year. The company expected to operate the department at 100% of normal capacity of 8,400 hours. During May, the department operated at 8,860 hours, and the factory overhead costs incurred were indirect factory wages, 32,400; power and light, 21,000; indirect materials, 18,250; supervisory salaries, 20,000; depreciation of plant and equipment, 36,200; and insurance and property taxes, 15,200. Instructions Prepare a factory overhead cost variance report for May. To be useful for cost control, the budgeted amounts should be based on 8,860 hours.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College PubFinancial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College PubFinancial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Financial & Managerial Accounting

Accounting

ISBN:9781337119207

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Operating segments; Author: The Finance Storyteller;https://www.youtube.com/watch?v=8IDQtBn902Q;License: Standard Youtube License