Concept explainers

Videos

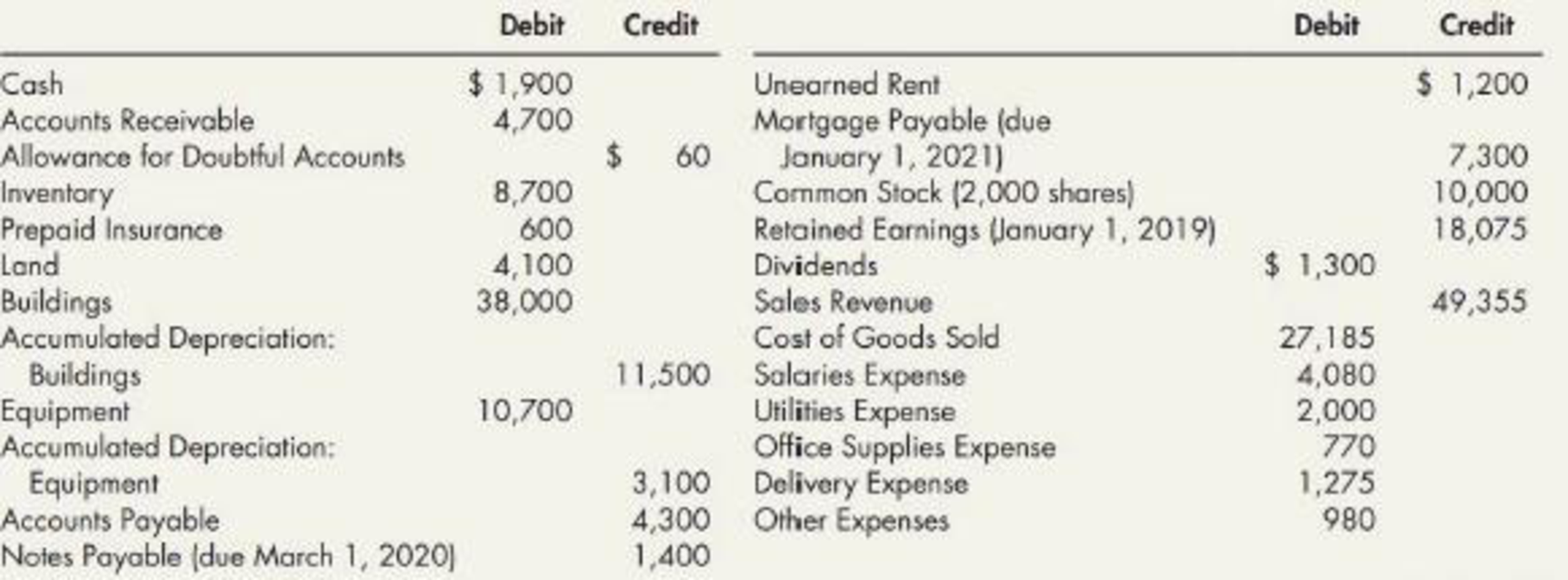

Worksheet Victoria Company has the following account balances on December 31, 2019, prior to any adjustments:

Additional adjustment information: (a)

Required:

- 1. Transfer the account balances to a 10-column worksheet and prepare a

trial balance . - 2. Prepare the

adjusting entries in the general journal and complete the worksheet. - 3. Prepare the company’s income statement,

retained earnings statement, andbalance sheet . - 4. Prepare closing entries in the general journal.

1 and 2

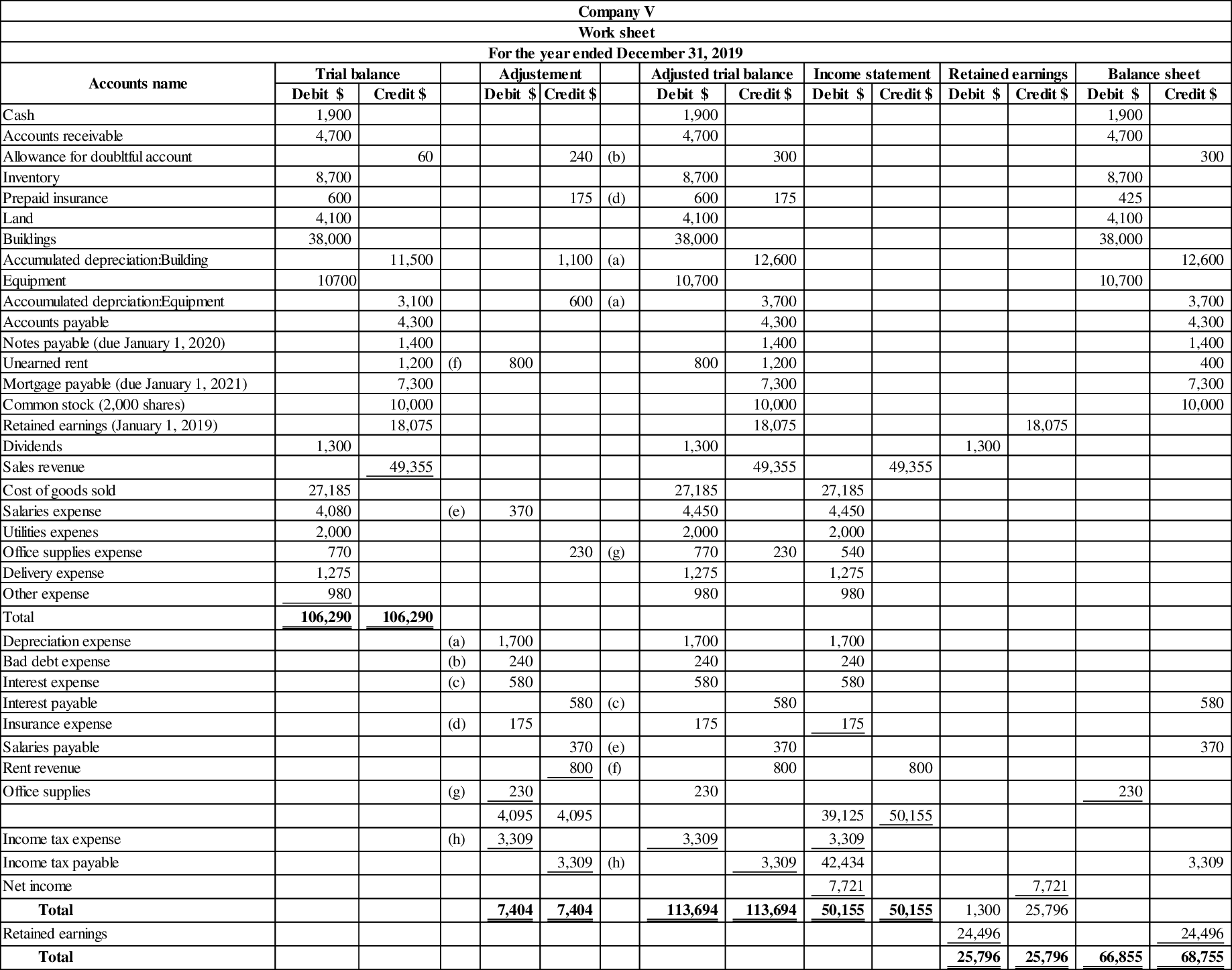

Prepare a 10 column worksheet for the given account balances, and prepare the adjusting entries of Company V.

Explanation of Solution

Trial balance: Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the ledger postings and helps preparing the final accounts.

Worksheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Prepare 10 column worksheet for the given account balances, and trial balance as follows:

Figure (1)

Adjusting entry:

| Date | Account Title & Explanation | Debit ($) | Credit($) |

| December 31, 2019 | Depreciation expense | 1,700 | |

| Accumulated depreciation - Buildings | 1,100 | ||

| Accumulated depreciation - Equipment | 600 | ||

| (To record the depreciation expense incurred at the end of the accounting year) | |||

| December 31, 2019 | Bad debts expense | 240 | |

| Allowance for doubtful accounts | 240 | ||

| (To record the bad debts expense estimated at the end of the accounting year) | |||

| December 31, 2019 | Interest expense | 580 | |

| Interest payable | 580 | ||

| (To record the interest expense incurred at the end of the accounting year) | |||

| December 31, 2019 | Insurance expense | 175 | |

| Prepaid insurance | 175 | ||

| (To record the insurance expense incurred at the end of the accounting year) | |||

| December 31, 2019 | Salaries expense | 370 | |

| Salaries payable | 370 | ||

| (To record the salaries expense accrued at the end of the accounting year) | |||

| December 31, 2019 | Unearned rent | 800 | |

| Rent revenue | 800 | ||

| (To record the rent revenue recognized) | |||

| December 31, 2019 | Office supplies expense | 230 | |

| Office supplies | 230 | ||

| (To record the supplies used during the year) | |||

| December 31, 2019 | Income tax expense (1) | 3,309 | |

| Income tax payable | 3,309 | ||

| (To record the income tax expense incurred at the end of the accounting year) |

Table (1)

Working note (1):

Calculate the value of income tax expense.

3.

Prepare income statement, retained earnings, and balance sheet of Company V.

Explanation of Solution

Financial statements: Financial statements are condensed summary of transactions communicated in the form of reports for the purpose of decision making. The financial statements are balance sheet, income statement, statement of retained earnings, and the cash flow statement.

Prepare income statement, retained earnings, and balance sheet of Company V as follows:

| Company V | ||

| Income statement | ||

| For the year ended December 31, 2019 | ||

| Particulars | Amount($) | Amount ($) |

| Service revenue | 49,355 | |

| Less: Cost of goods sold | (27,185) | |

| Gross profit | 22,170 | |

| Less: Operating expense | ||

| Salaries expense | 4,450 | |

| Utilities expense | 2,000 | |

| Office supplies expense | 540 | |

| Delivery expense | 1,275 | |

| Depreciation expense | 1,700 | |

| Bad debt expense | 240 | |

| Insurance expense | 175 | |

| Other expense | 980 | |

| Total operating expense | 11,360 | |

| Income from operations | 10,810 | |

| Other items: | ||

| Rent revenue | 800 | |

| Interest expense | (580) | 220 |

| Income before income taxes | 11,030 | |

| Income tax expense | (3,309) | |

| Net income (A) | 14,339 | |

| Number of shares (B) | 2,000 shares | |

| Earnings per share | $3.86 | |

Table (2)

| Company V | |

| Statement of retained earnings | |

| For the year end December 31, 2019 | |

| Particulars | Amount ($) |

| Retained earnings on January 1, 2019 | 18,075 |

| Add: Net income | 7,721 |

| 25,796 | |

| Less: Dividend for 2019 | (1,300) |

| Retained earnings on December 31, 2019 | 24,496 |

Table (3)

| Company V | ||

| Balance sheet | ||

| As at December 31, 2019 | ||

| Assets | Amount ($) | Amount ($) |

| Current assets: | ||

| Cash | 1,900 | |

| Accounts receivable | 4,700 | |

| Less: Allowance for doubtful accounts | (300) | 4,400 |

| Inventory | 8,700 | |

| Prepaid insurance | 425 | |

| Office supplies | 230 | |

| Total current assets (C) | 15,655 | |

| Property, plant and equipment: | ||

| Land | 4,100 | |

| Buildings | 38,000 | |

| Less: Accumulated depreciation | (12,600) | 25,400 |

| Equipment | 10,700 | |

| Less: Accumulated depreciation | (3,700) | 7,000 |

| Total property, plant and equipment (D) | 36,500 | |

| Total assets | 52,155 | |

| Liabilities | ||

| Current liabilities: | ||

| Accounts payable | 4,300 | |

| Notes payable | 1,400 | |

| Interest payable | 580 | |

| Salaries payable | 370 | |

| Unearned rent | 400 | |

| Income tax payable | 3,309 | |

| Total current liabilities | 10,359 | |

| Long-term liabilities: | ||

| Mortgage payable | 7,300 | |

| Total liabilities | 17,659 | |

| Shareholders' equity | ||

| Contributed capital: | ||

| Common stock | 10,000 | |

| Retained earnings | 24,496 | 34,496 |

| Total shareholder's equity | 52,155 | |

Table (4)

4.

Prepare closing entries of Company V for the current year.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare closing entries of Company V for the current year as follows:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| December 31, 2019 | Sales revenue | 49,355 | |

| Rent revenue | 800 | ||

| Income summary | 50,155 | ||

| (To close the sales revenue and rent revenue account) | |||

| December 31, 2019 | Income summary | 42,434 | |

| Cost of goods sold | 27,185 | ||

| Salaries expense | 4,450 | ||

| Utilities expense | 2,000 | ||

| Office supplies expense | 540 | ||

| Delivery expense | 1,275 | ||

| Other expense | 980 | ||

| Depreciation expense | 1,700 | ||

| Bad debt expense | 240 | ||

| Interest expense | 580 | ||

| Insurance expense | 175 | ||

| Income tax expense | 3,309 | ||

| (To close all expenses account) | |||

| December 31, 2019 | Income summary | 7,721 | |

| Retained earnings (2) | 7,721 | ||

| (To close the income summary account) | |||

| December 31, 2019 | Retained Earnings | 1,300 | |

| Dividends | 1,300 | ||

| (To close the dividends account.) |

Table (5)

Closing entry for revenue account:

In this closing entry, the sales revenue and rent revenue account is closed by transferring the amount of revenue to the income summary account in order to bring the revenue accounts balance to zero. Hence, debit all revenue account for $50,155, and credit the income summary account for $50,155.

Closing entry for expenses account:

In this closing entry, cost of goods sold, operating expense, and income tax expense are closed by transferring the amount of all expenses to the income summary account in order to bring all the expense accounts balance to zero. Hence, debit the income summary account for $42,434, and credit all the expenses account for $42,434.

Closing entry for income summary account:

In this closing entry, the income summary account is closed by transferring the amount of net income to the retained earnings account in order to bring the income summary balance to zero. Hence, debit the income summary account for $7,721, and credit the retained earnings for $7,721.

Closing entry for dividends account:

The dividends are paid to the shareholders out of the retained earnings. Thus, retained earnings are debited since the earnings are decreased on payment of dividend. Dividends are a component of shareholders’ equity account. It is credited because dividends are transferred to retained earnings account.

Working note (2):

Calculate the value of retained earnings.

Want to see more full solutions like this?

Chapter 3 Solutions

Intermediate Accounting: Reporting And Analysis

- At the end of 2019, Framber Company received 8,000 as a prepayment for renting a building to a tenant during 2020. The company erroneously recorded the transaction by debiting Cash and crediting Rent Revenue in 2019 instead of 2020. Upon discovery of this error in 2020, what correcting journal entry will Framber make? Ignore income taxes.arrow_forwardThe unadjusted trial balance of Recessive Interiors at January 31, 2019, the end of the year, follows: The data needed to determine year-end adjustments are as follows: a. Supplies on hand at January 31 are 2,850. b. Insurance premiums expired during the year are 3,150. c. Depreciation of equipment during the year is 5,250. d. Depreciation of trucks during the year is 4,000. e. Wages accrued but not paid at January 31 are 900. Instructions 1. For each account listed in the unadjusted trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark () in the Posting Reference column. 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed. 3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors chart of accounts should be used: Wages Payable, 22; Depreciation ExpenseEquipment, 54; Supplies Expense, 55; Depreciation ExpenseTrucks, 56; Insurance Expense, 57. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a statement of owners equity (no additional investments were made during the year), and a balance sheet. 6. Journalize and post the closing entries. Record the closing entries on Page 27 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 7. Prepare a post-closing trial balance.arrow_forwardReece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services accounting clerk prepared the following unadjusted trial balance at July 31, 2019: The data needed to determine year-end adjustments are as follows: Depreciation of building for the year, 6,400. Depreciation of equipment for the year, 2,800. Accrued salaries and wages at July 31, 900. Unexpired insurance at July 31, 1,500. Fees earned but unbilled on July 31, 10,200. Supplies on hand at July 31, 615. Rent unearned at July 31, 300. Instructions 1. Journalize the adjusting entries using the following additional accounts: Salaries and Wages Payable, Rent Revenue, Insurance Expense, Depreciation ExpenseBuilding, Depreciation ExpenseEquipment, and Supplies Expense. 2. Determine the balances of the accounts affected by the adjusting entries and prepare an adjusted trial balance.arrow_forward

- Prepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. supplies actual count at year end, $6,500 B. remaining unexpired insurance, $6,000 C. remaining unearned service revenue, $1,200 D. salaries owed to employees, $2,400 E. depreciation on property plant and equipment, $18,000arrow_forwardWorksheet for Service Company Whitaker Consulting Company has prepared a trial balance on the following partially completed worksheet for the year ended December 31, 2019: Additional information: (a) On January 1, 2019, the company had paid 2 years rent in advance at 100 a month for office space, (b) the office equipment is being depreciated on a straight-line basis over a 10-year life, and no residua! value is expected, (c) interest of 150 has accrued on the note payable but has not been paid, and (d) the income tax rate is 30% on current income and will be paid in the first quarter of 2020. Required: 1. Complete the worksheet. 2. Prepare financial statements for 2019.arrow_forwardReversing Entries On December 31, 2019, Kellams Company made the following adjusting entries for its annual accounting period: Required: Prepare whatever reversing entries are appropriate.arrow_forward

- Prepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. depreciation on buildings and equipment, $17,500 B. advertising still prepaid at year end, $2,200 C. interest due on notes payable, $4,300 D. unearned rental revenue, $6,900 E. interest receivable on notes receivable, $1,200arrow_forwardAt the beginning of 2020, Tanham Company discovered the following errors made in the preceding 2 years: Reported net income was 27,000 in 2018 and 35,000 in 2019. The allowance for doubtful accounts had a zero balance at the beginning of 2018. No accounts were written off during 2018 or 2019. Ignore income taxes. Required: 1. What is the correct net income for 2018 and 2019? 2. Prepare the adjusting journal entry in 2020 to correct the errors.arrow_forwardShannon Corporation began operations on January 1, 2019. Financial statements for the years ended December 31, 2019 and 2020, contained the following errors: In addition, on December 31, 2020, fully depreciated machinery was sold for 10,800 cash, but the sale was not recorded until 2021. There were no other errors during 2019 or 2020, and no corrections have been made for any of the errors. Refer to the information for Shannon Corporation above. Ignoring income taxes, what is the total effect of the errors on the amount of working capital (current assets minus current liabilities) at December 31, 2020? a. working capital overstated by 4,200 b. working capital understated by 5,800 c. working capital understated by 6,000 d. working capital understated by 9,800arrow_forward

- Soon after December 31, 2019, the auditor requested a depreciation schedule for trucks of Jarrett Trucking Company, showing the additions, retirements, depreciation, and other data affecting the income of the company in the 4-year period 2016 to 2019, inclusive. The following data were in the Trucks account as of January 1, 2016: The Accumulated DepreciationTrucks account, previously adjusted to January 1,2016, and duly entered in the ledger, had a balance on that date of 16,460. This amount represented the straight-line depreciation on the four trucks from the respective dates of purchase, based on a 5-year life and no residual value. No debits had been made to this account prior to January 1, 2016. Transactions between January 1,2017, and December 31, 2019, and their record in the ledger were as follows: 1. July 1, 2016: Truck no. 1 was sold for 1,000 cash. The entry was a debit to Cash and a credit to Trucks, 1,000. 2. January 1, 2017: Truck no. 3 was traded for a larger one (no. 5) with a 5-year life. The agreed purchase price was 12,000. Jarrett paid the other company 1,780 cash on the transaction. The entry was a debit to Trucks, 1,780, and a credit to Cash, 1,780. 3. July 1, 2018: Truck no. 4 was damaged in a wreck to such an extent that it was sold as junk for 50 cash. Jarrett received 950 from the insurance company. The entry made by the bookkeeper was a debit to Cash, 1,000, and credits to Miscellaneous Revenue, 50, and Trucks, 950, 4. July 1, 2018: A new truck (no. 6) was acquired for 20,000 cash and debited at that amount to the Trucks account. The truck has a 5-year life. Entries for depreciation had been made at the close of each year as follows: 2016, 8,840; 2017, 5,436; 2018, 4,896; 2019, 4,356. Required: 1. Next Level For each of the 4 years, calculate separately the increase or decrease in earnings arising from the companys errors in determining or entering depreciation or in recording transactions affecting trucks. 2. Prove your work by one compound journal entry as of December 31, 2019; the adjustment of the Trucks account is to reflect the correct balances, assuming that the books have not been closed for 2019.arrow_forwardSpreadsheet The following 2019 information is available for Payne Company: Partial additional information: The net income for 2019 totaled 1,600. During 2019, the company sold, for 390, equipment that cost 390 and had a book value of 300. The company sold land for 200, resulting in a loss of 40. The remaining change in the Land account resulted from the purchase of land through the issuance of common stock. Required: Making whatever additional assumptions that are necessary, prepare a spreadsheet to support the 2019 statement of cash flows for Payne.arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College