Videos

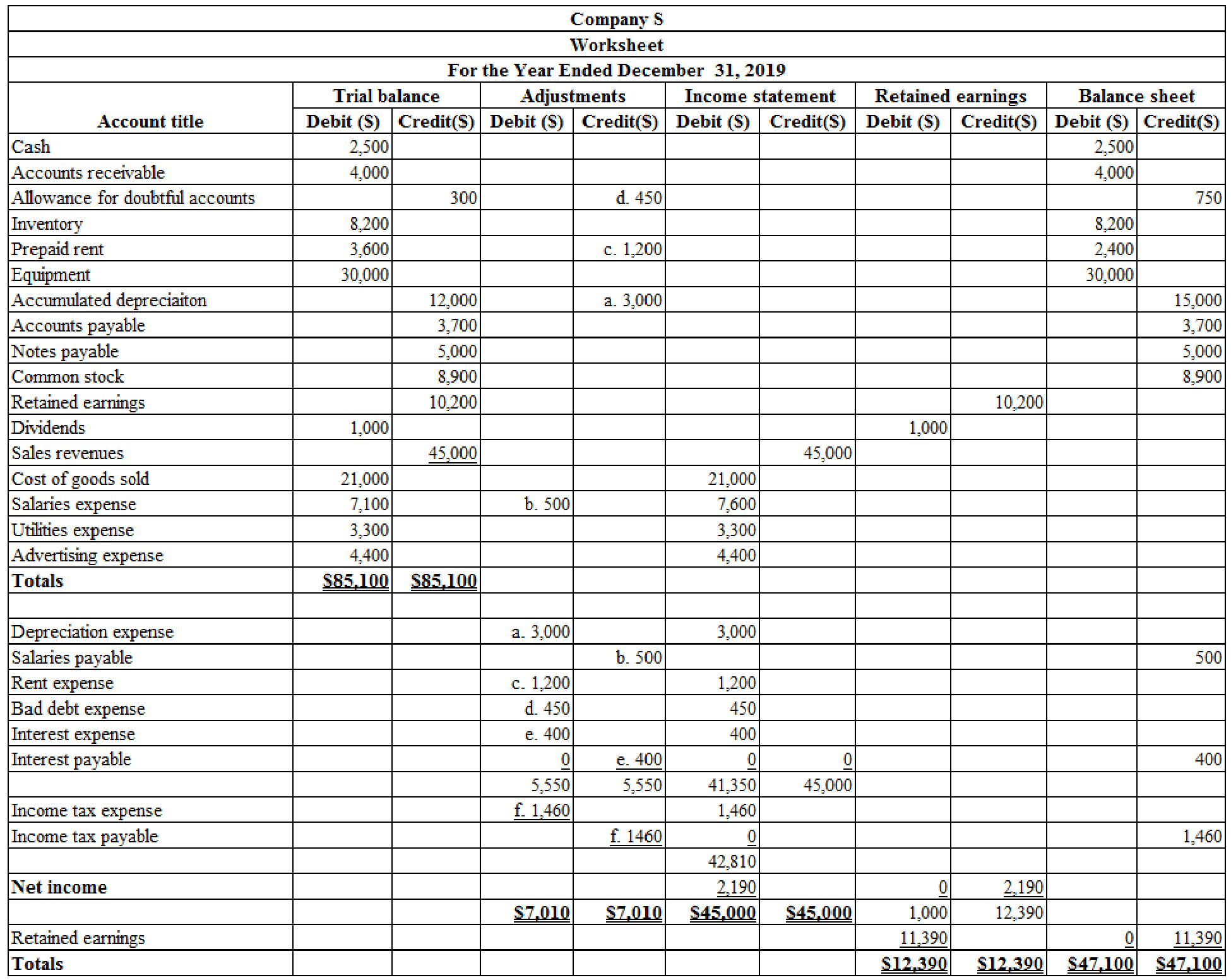

Worksheet, Including Inventory Surian Motors Company prepared a

Additional information: (a) The equipment is being

Required:

- 1. Complete the worksheet.

- 2. Prepare financial statements for 2019.

- 3. Prepare closing entries in the general journal.

1.

Prepare the worksheet for the year ended December 31, 2019.

Explanation of Solution

Worksheet: A worksheet is a tool that is used while preparing a financial statement. It is a type of form, having multiple columns and it is used in the adjustment process.

Prepare the worksheet for the year ended December 31, 2019:

Table (1)

2.

Prepare the financial statements of Company S for the year ended December 31, 2019.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement of Company S for the year ended December 31, 2019:

| Company S | ||

| Income statement | ||

| For the Year Ended December 31, 2019 | ||

| Particulars | Amount($) | Amount($) |

| Sales revenue | 45,000 | |

| Less: Cost of goods sold | (21,000) | |

| Gross profit | 24,000 | |

| Less: Operating expenses: | ||

| Salaries expense | 7,600 | |

| Utilities expense | 3,300 | |

| Advertising expense | 4,400 | |

| Depreciation expense | 3,000 | |

| Rent expense | 1,200 | |

| Bad debt expense | 450 | |

| Total operating expense | (19,950) | |

| Income from operations | 4,050 | |

| Other items: | ||

| Interest expense | (400) | |

| Income before income taxes | 3,650 | |

| Less: Income tax expense | (1,460) | |

| Net income | $2,190 | |

| Earnings per share (1,000 shares) | $2.19 | |

Table (2)

Working notes 1: Calculate the amount of salaries expense.

Working note 2: Calculate the amount of rent expense.

Working note 3: Calculate the amount of depreciation expense.

Working note 4: Calculate the amount of income tax expense.

Working note 5: Calculate the amount of bad debt expense.

Working note 6: Calculate earnings per share.

Statement of Retained Earnings: Statement of retained earnings shows, the changes in the retained earnings, and the income left in the company after payment of the dividends, for the accounting period.

Prepare statement of retained earnings of Company S for the year ended December 31, 2019:

| Company S | ||

| Statement of Retained Earnings | ||

| For the Year Ended December 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Retained earnings, January 1, 2019 | 10,200 | |

| Add: Net income | 2,190 | |

| Subtotal | 12,390 | |

| Less: Dividends | (1,000) | |

| Retained earnings at December 31, 2019 | $11,390 | |

Table (3)

Balance Sheet: Balance Sheet is one of the financial statements which summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare the balance sheet of Company S for the year ended December 31, 2019:

| Company S | ||

| Balance Sheet | ||

| As on December 31, 2019 | ||

| Assets | ||

| Current assets: | Amount ($) | Amount ($) |

| Cash | 2,500 | |

| Accounts receivable | 4,000 | |

| Less: Allowance for doubt accounts | (750) | 3,250 |

| Inventory | 8,200 | |

| Prepaid rent | 2,400 | |

| Total current assets | ||

| Property, plant and equipment: | ||

| Equipment | 30,000 | |

| Less: Accumulated depreciation | (15,000) | |

| Net property, plant and equipment | 15,000 | |

| Total assets | $31,350 | |

| Liabilities and Equity | ||

| Liabilities: | ||

| Current liabilities: | ||

| Accounts payable | 3,700 | |

| Notes payable | 5,000 | |

| Salaries payable | 500 | |

| Interest payable | 400 | |

| Income taxes payable | 1,460 | |

| Total liabilities | 11,060 | |

| Shareholders’ Equity | ||

| Contributed Capital: | ||

| Common stock | 8,900 | |

| Retained earnings | 11,390 | |

| Total shareholders’ equity | 20,290 | |

| Total liabilities and shareholders’ equity | $31,350 | |

Table (4)

3.

Prepare the closing entries for the year ended December 31, 2019 in the general journal.

Explanation of Solution

Prepare the closing entries:

| Date | Accounts title and explanation | Post Ref. | Debit | Credit |

| ($) | ($) | |||

| December 31, 2019 | Sales Revenue | 45,000 | ||

| Income Summary | 45,000 | |||

| (To close the revenue accounts) | ||||

| December 31, 2019 | Income Summary | 42,810 | ||

| Cost of Goods Sold | 21,000 | |||

| Salaries Expense | 7,600 | |||

| Utilities Expense | 3,300 | |||

| Advertising Expense | 4,400 | |||

| Depreciation Expense | 3,000 | |||

| Rent Expense | 1,200 | |||

| Bad Debt Expense | 450 | |||

| Interest Expense | 400 | |||

| Income Tax Expense | 1,460 | |||

| (To close the expense accounts) | ||||

| December 31, 2019 | Income Summary | 2,190 | ||

| Retained Earnings | 2,190 | |||

| (To close the income summary account) | ||||

| December 31, 2019 | Retained Earnings | 1,000 | ||

| Dividends | 1,000 | |||

| (To close the dividends account) | ||||

Table (5)

Want to see more full solutions like this?

Chapter 3 Solutions

Intermediate Accounting: Reporting And Analysis

- Worksheet for Service Company Whitaker Consulting Company has prepared a trial balance on the following partially completed worksheet for the year ended December 31, 2019: Additional information: (a) On January 1, 2019, the company had paid 2 years rent in advance at 100 a month for office space, (b) the office equipment is being depreciated on a straight-line basis over a 10-year life, and no residua! value is expected, (c) interest of 150 has accrued on the note payable but has not been paid, and (d) the income tax rate is 30% on current income and will be paid in the first quarter of 2020. Required: 1. Complete the worksheet. 2. Prepare financial statements for 2019.arrow_forwardDuring 2019, Ryel Companys controller asked you to prepare correcting journal entries for the following three situations: 1. Machine A was purchased for 50,000 on January 1, 2014. Straight-line depreciation has been recorded for 5 years, and the Accumulated Depreciation account has a balance of 25,000. The estimated residual value remains at 5,000, but the service life is now estimated to be 1 year longer than estimated originally. 2. Machine B was purchased for 40,000 on January 1, 2017. It had an estimated residual value of 5,000 and an estimated service life of 10 years. it has been depreciated under the double-declining-balance method for 2 years. Now, at the beginning of the third year, Ryel has decided to change to the straight-line method. 3. Machine C was purchased for 20,000 on January 1, 2018, Double-declining-balance depreciation has been recorded for 1 year. The estimated residual value of the machine is 2,000 and the estimated service life is 5 years. The computation of the depreciation erroneously included the estimated residual value. Required: Prepare any necessary correcting journal entries for each situation. Also prepare the journal entry necessary for each situation to record depreciation expense for 2019.arrow_forwardWorksheet Devlin Company has prepared the following partially completed worksheet for the year ended December 31, 2019: The following additional information is available: (a) salaries accrued but unpaid total 250; (b) the 80 heat and light bill for December has not been recorded or paid; (c) depreciation expense totals 810 on the buildings and equipment; (d) interest accrued on the note payable totals 380 (this will be paid when the note is repaid); (e) the company leases a portion of its floor space to KT Daniel Specialty Company for 50 per month, and KT Daniel has not yet paid its December rent; (f) interest accrued on the note receivable totals 80; (g) bad debts expense is 70; and (h) the income tax rate is 30% on current income and is payable in the first quarter of 2017. Required: 1. Complete the worksheet. (Round to the nearest dollar.) 2. Prepare the companys financial statements. 3. Prepare (a) adjusting and (b) closing entries in the general journal.arrow_forward

- At the end of 2020, while auditing Sandlin Companys books, before the books have been closed, you find the following items: a. A building with a 30-year life (no residual value, depreciated using the straight-line method) was purchased on January 1, 2020, by issuing a 90,000 non-interest-bearing, 4-year note. The entry made to record the purchase was a debit to Building and a credit to Notes Payable for 90,000; 12% is a fair rate of interest on the note. b. The inventory at the end of 2020 was found to be overstated by 15,000. At the same time, it was discovered that the inventory at the end of 2019 had been overstated by 35,000. The company uses the perpetual inventory system. c. For the last 3 years, the company has failed to accrue salaries and w-ages. The correct amounts at the end of each year were: 2018, 12,000; 2019, 18,000; and 2020, 10,000. Required: 1. Prepare journal entries to correct the errors. Ignore income taxes. 2. Assume, instead, that the company discovered the errors after it had closed the books. Prepare journal entries to correct the errors. Ignore income taxes.arrow_forwardDuring 2019, White Company determined that machinery previously depreciated over a 7-year life had a total estimated useful life of only 5 years. An accounting change was made in 2019 to reflect the change in estimate. If the change had been made in 2018, accumulated depreciation at December 31, 2018, would have been 1,600,000 instead of 1,200,000. As a result of this change, the 2019 depreciation expense was 100,000 greater than it would have been if no change were made. Ignoring income tax considerations, what is the proper amount of the adjustment to Whites January 1, 2019, balance of retained earnings? a. 0 b. 100,000 c. 280,000 d. 400,000arrow_forwardHathaway Company purchased a copying machine for 8,700 on October 1, 2019. The machines residual value was 500 and its expected service life was 5 years. Hathaway computes depreciation expense to the nearest whole month. Required: 1. Compute depredation expense (rounded to the nearest dollar) for 2019 and 2020 using the: a. straight-line method b. sum-of-the-years-digits method c. double-declining-balance method 2. Next Level Which method produces the highest book value at the end of 2020? 3. Next Level Which method produces the highest charge to income in 2020? 4. Next Level Over the life of the asset, which method produces the greatest amount of depreciation expense?arrow_forward

- Shannon Corporation began operations on January 1, 2019. Financial statements for the years ended December 31, 2019 and 2020, contained the following errors: In addition, on December 31, 2020, fully depreciated machinery was sold for 10,800 cash, but the sale was not recorded until 2021. There were no other errors during 2019 or 2020, and no corrections have been made for any of the errors. Refer to the information for Shannon Corporation above. Ignoring income taxes, what is the total effect of the errors on the amount of working capital (current assets minus current liabilities) at December 31, 2020? a. working capital overstated by 4,200 b. working capital understated by 5,800 c. working capital understated by 6,000 d. working capital understated by 9,800arrow_forwardAt the beginning of 2020, Holden Companys controller asked you to prepare correcting entries for the following three situations: 1. Machine X was purchased for 100,000 on January 1, 2015. Straight-line depreciation has been recorded for 5 years, and the Accumulated Depreciation account has a balance of 45,000. The estimated residual value remains at 10,000, but the service life is now estimated to be 1 year longer than originally estimated. 2. Machine Y was purchased for 40,000 on January 1, 2018. It had an estimated residual value of 4,000 and an estimated service life of 8 years. It has been depreciated under the sum-of-the-years-digits method for 2 years. Now, the company has decided to change to the straight-line method. 3. Machine Z was purchased for 80,000 on January 1, 2019. Double-declining-balance depreciation has been recorded for 1 year. The estimated residual value is 8,000 and the estimated service life is 5 years. The computation of the depreciation erroneously included the estimated residual value. Required: Prepare any necessary correcting journal entries for each situation. Also prepare the journal entry for each situation to record the depreciation for 2020. Ignore income taxes.arrow_forwardThe balance in Ashwood Companys accounts payable account at December 31, 2019, was 1,200,000 before any necessary year-end adjustment relating to the following: Goods were in transit from a vendor to Ashwood on December 31, 2019. The invoice cost was 85,000, and the goods were shipped FOB shipping point on December 29, 2019. The goods were received on January 2, 2020. Goods shipped FOB shipping point on December 20, 2019, from a vendor to Ashwood were lost in transit. The invoice cost was 40,000. On January 5, 2020, Ashwood filed a 40,000 claim against the common carrier. Goods shipped FOB destination on December 22, 2019, from a vendor to Ashwood were received on January 6, 2020. The invoice cost was 20,000, What amount should Ashwood report as accounts payable on its December 31,2019, balance sheet? a. 1,260,000 b. 1,285,000 c. 1,325,000 d. 1,345,000arrow_forward

- Kraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation. The following information was available from Krafts inventory records for the two most recent years: Required: Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.arrow_forwardCOMPLETION OF A WORK SHEET SHOWING A NET LOSS The trial balance for Cascade Bicycle Shop, a business owned by David Lamond, is shown below. Year-end adjustment information is as follows: (a and b) Merchandise inventory costing 22,000 is on hand as of December 31, 20--. (The periodic inventory system is used.) (c)Supplies remaining at the end of the year, 2,400. (d)Unexpired insurance on December 31, 1,750. (e)Depreciation expense on the building for 20--, 4,000. (f)Depreciation expense on the store equipment for 20--, 3,600. (g)Unearned storage revenue as of December 31, 1,950. (h)Wages earned but not paid as of December 31, 750. REQUIRED 1. Complete the Adjustments columns, identifying each adjustment with its corresponding letter. 2. Complete the work sheet. 3. Enter the adjustments in the general journal.arrow_forwardEthics and Sale of Operating Component It is the end of 2019, and, as an accountant for Newell Company, you are preparing its 2019 financial statements. On December 29, 2019, Newells management decided to sell one of its major divisions, subject to some legal work that is expected to be completed during the first week in April 2020 after the 2019 financial statements have been issued). During 2019, the division earned a small operating income that is just enough for the company to report record earnings for the year. However, the estimated fair value of the division at the end of 2019 is less than its net book value, so that management anticipates the component will be sold at a loss. Newells president stops by your office and says, You have been doing a fine job. Keep up the good work because you are heading for a promotion in early 2021. Once we report the record earnings for 2019, our shareholders and creditors will be happy. Then I think our earnings for 2020 will be high enough so that the loss we expect to report in 2020 on the sale of the division will not look so bad. After the president leaves your office, you continue preparing the 2019 financial statements. Required: From financial reporting and ethical perspectives, what information, if any, will you include about the upcoming sale of the division in the 2019 financial statements?arrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning