(a)

When the imported bananas are infected with a deadly virus what happens to the demand and supply curve.

Explanation of Solution

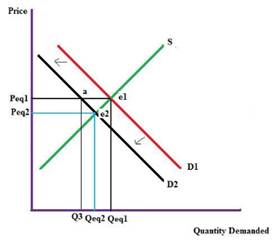

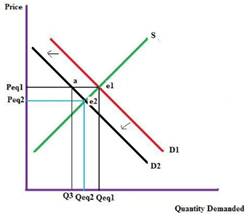

A report says that the bananas that have been imported are infected with a deadly virus, this will lead to the shift of consumers towards other fruits available in the market. Hence, the demand for the bananas will be less which will shift the demand curve towards left.

In the given graph, D1 is the initial demand curve, S is the initial supply curve, Peq1 is the initial price and Qeq1 is the initial quantity. Due to change in preferences of customers D1 shifts to D2 and S1 remains same. Price shifts from Peq1 to Peq2 creating a surplus in the market, hence, the price fall to a new equilibrium point e2, now the price is Peq2 and quantity is Qeq2.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(b)

When the consumers' income drops or decreases what happens to the demand and supply curve.

Explanation of Solution

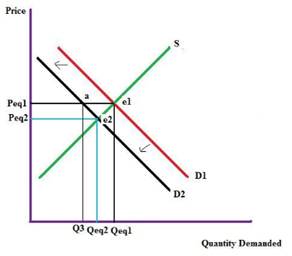

A fall in consumer income will reduce the demand as his disposable income, so demand curve shifts down, which in turn reduces the price of the product. In the given graph, D1 is the initial demand curve S is the initial supply curve, Peq1 is the initial price and Qeq1 is the initial quantity. Due to change in income demand curve shifts to the left to D2. Price Peq1 is same but demand come down i.e. Q3 which lower than Qeq1 creating a surplus in the market. This in turn shifts the price to a new equilibrium point e2 and price changes to Peq2.and quantity become Qeq2.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(c)

When the price of banana rises what happens to the demand and supply curve.

Explanation of Solution

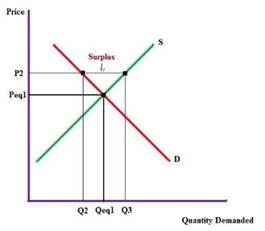

Demand is function of price and the quantity demanded. Hence, demand curve shifts when there is variation in the price and quantity demanded of the product. When price of banana rises quantity demanded will fall, which will create a surplus in the market.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(d)

When the price of oranges falls what happens to the demand and supply curve.

Explanation of Solution

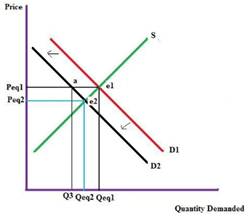

Oranges are a substitute to bananas. As the price of oranges fall, it causes a shift in the consumers preference. They start consuming more oranges than bananas. So, the quantity demanded for bananas fall and the demand curve of bananas shifts toward left reducing the price and consumption. Hence, at the new equilibrium point e2 price is reduced to Peq2 and quantity id reduced to Qeq2.

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

(e)

When the consumers assume the price of bananas to fall in future what happens to the demand and supply curve.

Explanation of Solution

When consumers feel the price of bananas would fall in future, they would stop the consumption of bananas at the current price creating a surplus in the market. This would lead to reduction in price of the bananas. At the new point of

Demand and supply are the basic concepts in economics, and they can vary depending on various factors. Demand can be defined as how much quantity of the product or service is demanded or can be availed by a customer.

Whereas Supply how much quantity of products or services is available in the market.

Want to see more full solutions like this?

Chapter 3 Solutions

Macroeconomics (MindTap Course List)

- In an analysis of the market for paint, an economist discovers the facts listed below. State whether each of these changes will affect supply or demand, and in what direction. There have recently been some important cost-saving inventions in the technology for making paint. Paint is lasting longer so that property owners need not repaint as often. Because of severe hailstorms, many people need to repaint now. The hailstorms damaged several factories that make paint, forcing them to close down for several months.arrow_forwardAs a group, discuss different factors that would affect the market for donuts. Now, suppose that the price of sugar has increased and at the same time, it is January and many people have just done their New Year's resolutions, one of which is to eat less sugar. What will the impact be on the market for donuts?arrow_forwardQuestion: Which of the following factors don’t affect the demand for a commodity?[A] Price of commodity[B] Income of individual consumer[C] Want of the consumer[D] Price of related goodPlease Dont use AI tool.arrow_forward

- Draw a supply and demand curve in which you label price axis, quantity axis, supply curve, demand curve, and equilibrium point. Upload your photo as an image to the discussion forum. Add a brief discussion about what the equilibrium point in economics means.arrow_forwardHow are quantity supplied and quantity demanded affected by changes in prices? Give an example of how these quantities might change if the price decreases.arrow_forwardPlot the supply curve and the demand curve for bicycles What is the equilibrium price of bicycles? What is the equilibrium quantity of bicycles? If the price of bicycles were €100, is there a surplus or a shortage? How many units of surplus or shortage are there? Will this cause the price to rise or fall ?arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning