(a)

Economic rent and transfer earning

Explanation of Solution

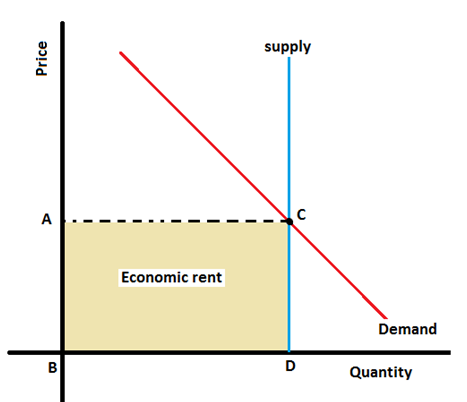

The given demand supply curve is perfectly inelastic; hence, when the supply is totally inelastic, the transfer earning would be zero. Hence, there would be only economics rent and no transfer earnings.

Graph showing the Economic rent in the perfectly inelastic supply demand curve.

The area ABCD represents the All Economic rent; there are no transfer earnings since the same amount would be supplied at a price of 0is supplied at market price.

Introduction:

Economic rent is the amount paid to the factor of production which is excess of what is economically or socially necessary.

Transfer earning is the minimum amount which is to be paid so that labour do not move to other occupation.

(b)

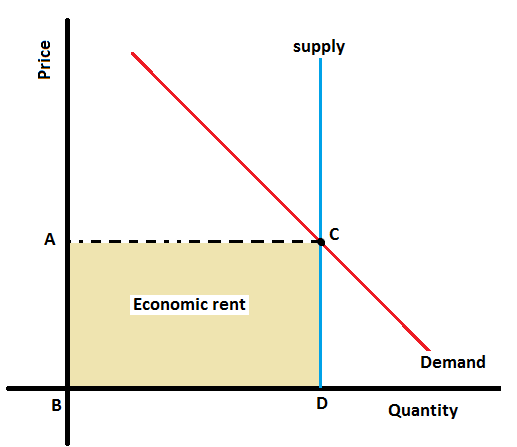

Impact on economic rent and transfer earning when demand increases.

Economic rent and transfer earning

Explanation of Solution

If the demand increased, there would be a shift in the demand curve to the right resulting the price increased from $ A to $ E.

The price in increase therefore results in the increase of economic rent.

Introduction:

Economic rent is the amount paid to the factor of production which is excess of what is economically or socially necessary.

Transfer earning is the minimum amount which is to be paid so that labour do not move to other occupation.

Want to see more full solutions like this?

- How does a market reach equilibrium without any outside intervention? Explain using the supply and demand concept. Please use proper graph.Thank you sir.arrow_forwardYou have learned that the Law of Supply and Demand determines prices in a free-market system. Using a concrete example, describe how the Law of supply and demand works. (Hint: think about seasonal items or holiday-specific popular items, for instance).arrow_forwardPlease answer D, E, & F. Demand, Supply, consumer surplus, Market Equilibrium Price floor. The following relations describe monthly demand and supply conditions in the metropolitan area for recyclable aluminum. QD = 80,000 – 20,000Px (Demand) QS = - 20,000 + 20,000Px (Supply) where Q is quantity measured in pounds of scrap aluminum and P is price in dollars. Answer the following questions: A. What is the condition for market equilibrium? B Calculate the market equilibrium price and equilibrium output? C. What is the inverse demand curve P = f (QD)? D. Compute the consumer surplus at the equilibrium price. E. What is the inverse supply curve P = f (Qs)? F. Compute the producer surplus at the equilibrium price.arrow_forward

- Who’s in the flow? By understanding the following image ans the following question: the role of the person: buyer OR seller; the market: resource OR product the sector: household OR firm the sector receiving the money payment: household OR firmarrow_forwardThe image attatchded shows a supply and demand curve for a product. (a) Find a price where the supply and demand curve would predict a surplus in the marketplace for the produce. Explain how you know there would be a surplus using using data from the supply and demand curve. (b) Estimate the price where the consumers would completely stop buying the product. Explain how you found your answers by referring to the above graph. (c) Estimate the price where the free market would eventually settle according to the supply and demand curve.arrow_forwardIdentify which side of the market for new automobiles is affected (demand or supply), how is it affected (increase or decrease), what happens to equilibrium price and quantity exchanged due to each of the following changes separately. (You don’t need to draw a graph unless it really makes your life easier) a. Car insurance rates increase. b. Price of steel increases. c. Price of public transportation increases.arrow_forward

- use diagramsa. What is the effect on the equilibrium price and quantity traded in market of theintroduction of a new technology that reduces costs of production for all firms?b. What is the effect on the equilibrium price and quantity traded in a market of a changein tastes that reduces the demand for the product?c. What is the effect on the equilibrium price and quantity traded in a market of theimposition of a tax per unit sold on suppliers?d. What is the effect on the equilibrium price and quantity traded in a market of thepayment of a subsidy per unit sold paid to suppliers?arrow_forwardconsumers demand for goods and services, which drives production, is the main element of _____ economy? a) command style demand-side b) fee market demand-side c) free market supply-side d) command style supply-sidearrow_forwardAssume that as the economy booms, the demand for business and consumer loans rises significantly, while the supply of funds and loans remains constant. As a result, the market interest rate for business and consumer loans rises to 20% per year. The government implements a ceiling on interest rates of 15% a year and as a result... Group of answer choices The quantity demanded of business and consumer loans rises, while the quantity supplied falls and a surplus occurs A greater number of business and consumer loans are made at a lower interest rate than previously. The demand of business and consumer loans rises, while the supply falls and a shortage occurs The quantity demanded of business and consumer loans rises, while the quantity supplied falls and a shortage occursarrow_forward

- 17. is a schedule that shows various amounts of a good or service a seller is willing and able to sell at each possible price during a particular period. A. Production possibilities curve B. Capacity utilization C. Demand D. Supplyarrow_forward. Assume the following data describe the gasoline market: (a) Graph the demand and supply curves. (b) What is the equilibrium price? (c) If supply at every price is reduced by 6 gallons, what will the new equilibrium price be? (d) If the government freezes the price of gasoline at its initial equilibrium price, how much of a surplus or shortage will exist when supply is reduced as described in part (c)?arrow_forwardIllustrate the market demand and market supply curves.arrow_forward

Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc

Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc