Videos

The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year’s appropriation.

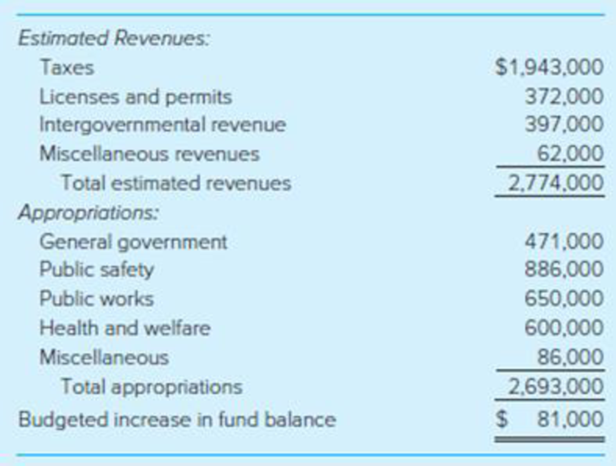

- 1. The budget prepared for the fiscal year 2020 was as follows:

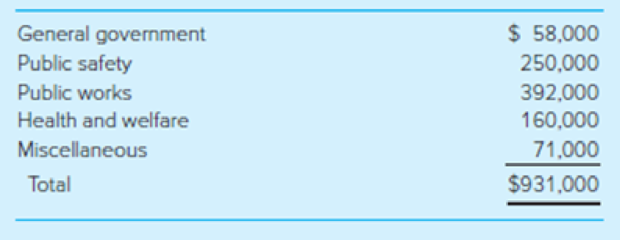

- 2. Encumbrances issued against the appropriations during the year were as follows:

- 3. The current year’s tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.

- 4. Tax collections of the current year’s levy totaled $1,459,000. The City also collected $132,000 in taxes from the prior year’s levy in the first 60 days after year end. (These delinquent collections had been anticipated prior to year-end.)

- 5. Personnel costs during the year were charged to the following appropriations in the amounts indicated. Encumbrances were not recorded for personnel costs. Because no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings. (Expenditures charged to Miscellaneous should be treated as General Government expenses in the governmental activities general journal at the government-wide level.)

- 6. Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470. Encumbrances had been recorded in the prior year for these items in the amount of $14,000. The amount chargeable to each year’s appropriations should be charged to the Public Safety appropriation.

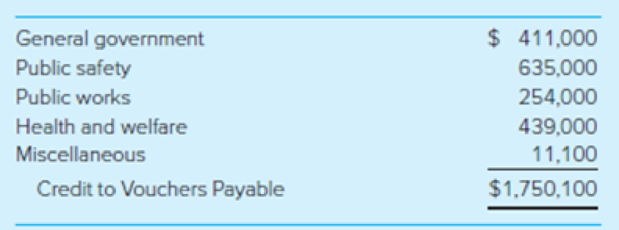

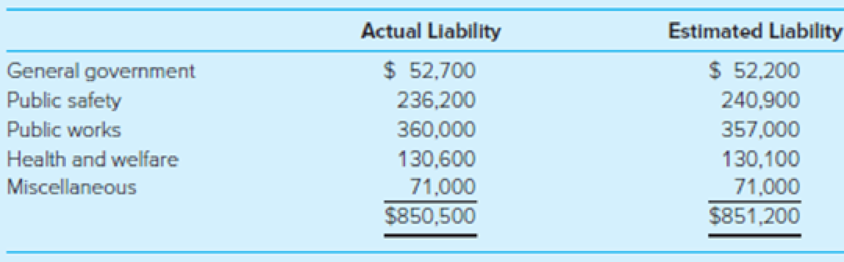

- 7. Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem. The following appropriations were affected.

- 8. Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues. For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function. Miscellaneous revenues are not identifiable with any function and, therefore, are recorded as General Revenues at the government-wide level.

- 9. Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance—Unassigned account had a credit balance of $96,900 as of December 31, 2019; no entries have been made in the Fund Balance—Unassigned account during 2020.

Required

- a. Record the preceding transactions in general journal form for fiscal year 2020 in both the General Fund and governmental activities general journals.

- b. Prepare a budgetary comparison schedule for the General Fund of the City of Evergreen for the fiscal year ending December 31, 2020, as shown in Illustration 4-6. Do not prepare a government-wide statement of activities because other governmental funds would affect that statement.

a.

Journalize the given transactions for the fiscal year 2020 in General Fund and governmental activities general journals.

Explanation of Solution

General Fund: The chief operating fund of state and local government used to record the departmental operating activities and government support services is referred to as General Fund, or General Operating Fund, or General Revenue Fund. The activities recorded in General Funds are police, fire, public works, recreation, education, culture, social services, city office, finance, personnel, and data processing.

Journalize the given transactions for the fiscal year 2020 in General Fund and governmental activities general journals.

1.

Entry to record the budget:

| General Ledger | Subsidiary Ledger | |||||

| Debits | Credits | Debits | Credits | |||

| General Fund: | ||||||

| Estimated Revenues | $2,774,000 | |||||

| Budgetary Fund Balance | $81,000 | |||||

| Appropriations | 2,693,000 | |||||

| Estimated Revenues Ledger: | ||||||

| Taxes | $1,943,000 | |||||

| Licenses and Permits | 372,000 | |||||

| Internalgovernmental Revenue | 397,000 | |||||

| Miscellaneous Revenues | 62,000 | |||||

| Appropriations Ledger: | ||||||

| General Government | $471,000 | |||||

| Public Safety | 886,000 | |||||

| Public Works | 650,000 | |||||

| Health and Welfare | 600,000 | |||||

| Miscellaneous | 86,000 | |||||

Table (1)

2.

Entry to record the encumbrances against appropriations:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances–2020 | $931,000 | ||||

| Encumbrances Outstanding–2020 | $931,000 | ||||

| Encumbrances Ledger: | |||||

| General Government | $58,000 | ||||

| Public Safety | 250,000 | ||||

| Public Works | 392,000 | ||||

| Health and Welfare | 160,000 | ||||

| Miscellaneous | 71,000 | ||||

Table (2)

3.

Entries to record property tax levy:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Taxes Receivable–Current | $2,005,000 | ||||

| Allowance for Uncollectible Current Taxes | $65,000 | ||||

| Revenues | 1,940,000 | ||||

| Revenues Ledger: | |||||

| Property Taxes | $1,940,000 | ||||

| Governmental Activities: | |||||

| Taxes Receivable–Current | $2,005,000 | ||||

| Allowance for Uncollectible Current Taxes | $65,000 | ||||

| General Revenues–Property Taxes | 1,940,000 | ||||

Table (3)

4.

Entry to record collection of delinquent taxes:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund and Governmental Activities: | |||||

| Cash | $1,591,000 | ||||

| Taxes Receivable–Delinquent | $132,000 | ||||

| Taxes Receivable–Current | 1,459,000 | ||||

Table (4)

5.

Entry to charge costs to appropriations:

| General Ledger | Subsidiary Ledger | |||||

| Debits | Credits | Debits | Credits | |||

| General Fund: | ||||||

| Expenditures | $1,750,100 | |||||

| Vouchers Payable | $1,750,100 | |||||

| Expenditures Ledger: | ||||||

| General Government | $411,000 | |||||

| Public Safety | 635,000 | |||||

| Public Works | 254,000 | |||||

| Health and Welfare | 439,000 | |||||

| Miscellaneous | 11,100 | |||||

| Governmental Activities: | ||||||

| Expenses–General Government | $422,100 | |||||

| Expenses–Public Safety | 635,000 | |||||

| Expenses–Public Works | 254,000 | |||||

| Expenses–Health and Welfare | 439,000 | |||||

| Vouchers Payable | $1,750,100 | |||||

Table (5)

6.

Entry for the receipt of invoice for the goods ordered in prior year and payment approval:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances Outstanding–2019 | $14,000 | ||||

| Encumbrances–2019 | $14,000 | ||||

| Encumbrances Ledger–2019: | |||||

| Public Safety | $14,000 | ||||

| Expenditures–2019 | 14,000 | ||||

| Expenditures–2019 | 470 | ||||

| Vouchers Payable | 14,470 | ||||

| Expenditures Ledger–2020: | |||||

| Public Safety | $470 | ||||

| Expenditures Ledger–2019: | |||||

| Public Safety | 14,000 | ||||

| Governmental Activities: | |||||

| Expenses–Public Safety | 14,470 | ||||

| Vouchers Payable | 14,470 | ||||

Table (6)

7.

Entry for the receipt of invoice for the goods ordered in 2020:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances Outstanding–2020 | $851,200 | ||||

| Encumbrances–2020 | $851,200 | ||||

| Encumbrances Ledger–2020: | |||||

| General Government | $52,200 | ||||

| Public Safety | 240,900 | ||||

| Public Works | 367,000 | ||||

| Health and Welfare | 130,100 | ||||

| Miscellaneous | 71,000 | ||||

| Expenditures–2020 | 850,500 | ||||

| Vouchers Payable | 850,500 | ||||

| Expenditures Ledger–2020: | |||||

| General Government | $52,700 | ||||

| Public Safety | 236,200 | ||||

| Public Works | 360,000 | ||||

| Health and Welfare | 130,600 | ||||

| Miscellaneous | 71,000 | ||||

| Governmental Activities: | |||||

| Expenses–General Government | 123,700 | ||||

| Expenses–Public Safety | 236,200 | ||||

| Expenses–Public Works | 360,000 | ||||

| Expenses–Health and Welfare | 130,600 | ||||

| Vouchers Payable | 850,500 | ||||

Table (7)

8.

Entry to record revenues collected:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Cash | $839,000 | ||||

| Revenues | $839,000 | ||||

| Revenues Ledger: | |||||

| Licenses and Permits | $373,000 | ||||

| Intergovernmental Revenue | 400,000 | ||||

| Miscellaneous Revenues | 66,000 | ||||

| Governmental Activities: | |||||

| Cash | |||||

| Program Revenues–General Government–Charges for Services | $373,000 | ||||

| Program Revenues–Public Safety–Operating Grants and Contributions | 400,000 | ||||

| General Revenues–Miscellaneous | 66,000 | ||||

Table (8)

9.

Entry to record the payment of vouchers:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund and Governmental Activities: | |||||

| Vouchers Payable | $2,505,000 | ||||

| Cash | $2,505,000 | ||||

Table (9)

b.

Prepare the budgetary comparison schedule for the General Fund of the City E for the year ending December 31, 2020.

Explanation of Solution

Budgetary comparison schedule: The schedule that shows the actual revenues, expenditures, outstanding encumbrances in comparison with the budgeted revenues, and appropriations as on a particular date, is referred to as budgetary comparison schedule.

Prepare the budgetary comparison schedule for the General Fund of the City E for the year ending December 31, 2020.

| City E | |||

| General Fund | |||

| Budgetary Comparison Schedule | |||

| For the Year Ended December 31, 2020 | |||

| Budgeted Amounts (Original and Final) | Actual Amounts | Variance with Final Budget Over (Under) | |

| Revenues: | |||

| Taxes | $1,943,000 | $1,940,000 | $(3,000) |

| Licenses and permits | 372,000 | 373,000 | 1,000 |

| Intergovernmental revenue | 397,000 | 400,000 | 3,000 |

| Miscellaneous revenues | 62,000 | 66,000 | 4,000 |

| Total Revenues | 2,774,000 | 2,779,000 | 5,000 |

| Expenditures and Encumbrances: | |||

| General government | $471,000 | 469,500 | (1,500) |

| Public safety | 886,000 | 880,770 | (5,230) |

| Public works | 650,000 | 649,000 | (1,000) |

| Health and welfare | 600,000 | 599,500 | (500) |

| Miscellaneous | 86,000 | 82,100 | (3,900) |

| Total Expenditures | 2,693,000 | 2,680,870 | (12,130) |

| Excess of Revenues over Expenditures | 81,000 | 98,130 | 17,130 |

| Increase in Encumbrances Outstanding | 0 | 65,800 | 65,800 |

| Increase in Fund Balances for Year | 81,000 | 163,930 | 82,930 |

| Fund Balances, January 1, 2020 | 96,900 | 96,900 | 0 |

| Fund Balances, December 31, 2020 | $177,900 | $260,830 | $82,930 |

Table (10)

Want to see more full solutions like this?

Chapter 4 Solutions

Accounting For Governmental & Nonprofit Entities

- The following transactions relate to the general fund of the city of Lost Angels for the year ending December 31, 2020. Prepare a statement of revenues, expenditures, and other changes in fund balance for the general fund for the period to be included in the fund financial statements. Assume that the fund balance at the beginning of the year was $180,000. Assume also that the city applies the purchases method to supplies. Receipt within 60 days serves as the definition of available resources. Collects property tax revenue of $700,000. A remaining assessment of $100,000 will be collected in the subsequent period. Half of that amount should be received within 30 days, and the remainder approximately five months after the end of the year. Spends $200,000 on three new police cars with 10-year lives. The anticipated price was $207,000 when the cars were ordered. The city calculates all depreciation using the straight-line method with no expected residual value. The city applies the…arrow_forwardThe following transactions relate to the general fund of the city of Lost Angels for the year ending December 31, 2020. Prepare a statement of revenues, expenditures, and other changes in fund balance for the general fund for the period to be included in the fund financial statements. Assume that the fund balance at the beginning of the year was $180,000. Assume also that the city applies the purchases method to supplies. Receipt within 60 days serves as the definition of available resources. Collects property tax revenue of $700,000. A remaining assessment of $100,000 will be collected in the subsequent period. Half of that amount should be received within 30 days, and the remainder approximately five months after the end of the year. Spends $200,000 on three new police cars with 10-year lives. The anticipated price was $207,000 when the cars were ordered. The city calculates all depreciation using the straight-line method with no expected residual value. The city applies the…arrow_forwardThe following information was available for the General Fund of the City of Clinton for the Year Ended December 31, 2012: (a) Revenues for the year included property taxes in the amount of $1,500,000, fines and forfeits in the amount of $600,000, and miscellaneous in the amount of$100,000. (b) Expenditures from current appropriations included: general government, $500,000; public safety, $1,300,000; culture and recreation, $300,000. (c) In addition to (b) above, expenditures related to prior year appropriations (encumbered last year) amounted to $40,000 (public safety). Encumbrances issued this year but not filled amounted to $60,000 (general government). (d) A transfer was made from the General Fund to a debt service fund in the amount of $400,000. A transfer was made from an enterprise fund to the General Fund in the amount of$100,000. (e) A sale of park land was made during the year, which was considered infrequent but not unusual and under the control of management. The proceeds…arrow_forward

- The City of Greystone maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: The City levied property taxes for the current fiscal year in the amount of $8,000,000. At year-end, $720,000 of the taxes had not been collected. It was estimated that $330,000 of that amount would be collected during the 60 days after the end of the fiscal year and that $360,000 would be collected after that time and the balance would be uncollectible. The City had recognized the maximum of property taxes allowable under modified accrual accounting. $255,000 of property taxes had been deferred at the end of the previous year and was recognized under modified accrual as revenue in the current year. In addition to the expenditures reported under modified accrual accounting, the city computed that an additional $104,000…arrow_forwardA city issues a 60-day tax anticipation note to fund operations until taxes have been collected. What recording should it make? The liability should be reported in the government-wide financial statements; an other financing source should be shown in the fund financial statements. A liability should be reported in the government-wide financial statements and in the fund financial statements. An other financing source should be shown in the government-wide financial statements and in the fund financial statements. An other financing source should be shown in the government-wide financial statements; a liability is reported in the fund financial statements.arrow_forwardIn 2019, a state government collected income taxes of $8,000,000 for the benefit of one of its cities that imposes an income tax on its residents. The state periodically remitted these collections to the city. The state should account for the $8,000,000 in the a. general fund. b. agency funds. c. internal service funds. d. special assessment funds.arrow_forward

- The following transactions relate to the general fund of the city of buffalo falls for the year ended december 31, 2020: 1. Begining Balances were: Cash, $80,000; Taxes receivable, $185,000; Accounts Payable, $50,000; and Fund Balance, $215,000. 2. The budget was passed. Estimated revenues amount to $1,200,000 and appropriations totaled $1,196,000. All expemditures are classifed as General Government. 3. property taxes were levied in the amount of $902,000. Alll of the taxes are expected to be collected before Febuary 2021. 4. Cash reciepts totaled $870,000 for property taxes and $275,000 from other revenue. 5. contracts were issued for contracted servies in the amount of $90,000. 6. Contracted services were preformed relating to $82,000 of the contracts with invoices ammounting to $80,000. 7. Other expenditures amounted to $950,000. 8. accounts payable were paid in the amount of $1,070,000. 9. The books were closed. Required: a. Prepare Jounal entries for the above tranactions. b.…arrow_forwardA city issues a 60-day tax anticipation note to fund operations until taxes have been collected. What recording should it make? Choose the correct.a. The liability should be reported in the government-wide financial statements; an other financing source should be shown in the fund financial statements.b. A liability should be reported in the government-wide financial statements and in the fund financial statements.c. An other financing source should be shown in the government-wide financial statements and in the fund financial statements.d. An other financing source should be shown in the government-wide financial statements; a liability is reported in the fund financial statements.arrow_forwardUnlike Illinois, the Village of Maple Park is located in a state in which property taxes are levied and collected in the same fiscal year. The information below pertains to the Village’s general fund for the year ended December 31, 2022: $9,819,000 of property tax revenue was included in the estimated revenues budget for 2022; Property taxes were levied in February, 2022, and $171,000 of the levy was expected to be uncollectible; On the two property tax collection dates, a total of $9,600,000 was collected; At December 31, 2022, the Village expected property tax collections during the first 60 days of 2023 to be $38,000. Required: 1. On the December 31, 2022, balance sheet for the Village’s general fund, what is the amount reported under assets for property taxes receivable(net)? 2. On the Village’s general fund statement of revenues, expenditures, and changes in fund balance for the year ended December 31, 2022, what is the amount reported for property…arrow_forward

- The City of Lynnwood was recently incorporated and had the following transactions for the fiscal year ended December 31. The city council adopted a General Fund budget for the fiscal year. Revenues were estimated at $2,000,000 and appropriations were $1,990,000. Property taxes in the amount of $1,940,000 were levied. It is estimated that $9,000 of the taxes levied will be uncollectible. A General Fund transfer of $25,000 in cash and $300,000 in equipment (with accumulated depreciation of $65,000) was made to establish a central duplicating internal service fund. A citizen of Lynnwood donated marketable securities with a fair value of $800,000. The donated resources are to be maintained in perpetuity with the city using the revenue generated by the donation to finance an after-school program for children, which is sponsored by the culture and recreation function. Revenue earned and received as of December 31 was $40,000. The city’s utility fund billed the city’s General Fund…arrow_forwardThe following transactions relate to the General Fund of the city of Lost Angels for the year ending December 31, 2017. Prepare a statement of revenues, expenditures, and other changes in fund balance for the general fund for the period to be included in the fund financial statements. Assume that the fund balance at the beginning of the year was $180,000. Assume also that the purchases method is applied to the supplies and that receipt within 60 days is used as the definition of avail-able resources.a. Collected property tax revenue of $700,000. A remaining assessment of $100,000 will be collected in the subsequent period. Half of that amount should be collected within 30 days, and the remainder will be received in about five months after the end of the year.b. Spent $200,000 on four new police cars with 10-year lives. A price of $207,000 had been anticipated when the cars were ordered. The city calculates all depreciation using the straight-line method with no salvage value. The…arrow_forwardThe City of Jonesboro engaged in the following transactions during the fiscal year ended September 30, 2018. Record the following transactions related to interfund transfers. Be sure to indicate in which fund the entry is being made. a. The city transferred $400,000 from the general fund to a debt service fund to make the interest payments due during the fiscal year. The payments due during the fiscal year were paid. The city also transferred $200,000 from the general fund to a debt service fund to advance-fund the $200,000 interest payment due October 15, 2019. b. The city transferred $75,000 from the Air Operations Special Revenue Fund to the general fund to close out the operations of that fund. c. The city transferred $150,000 from the general fund to the city’s Electric Utility Enterprise Fund to pay for the utilities used by the general and administrative offices during the year. d. The city transferred the required pension contribution of $2 million from the general fund to the…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education