Videos

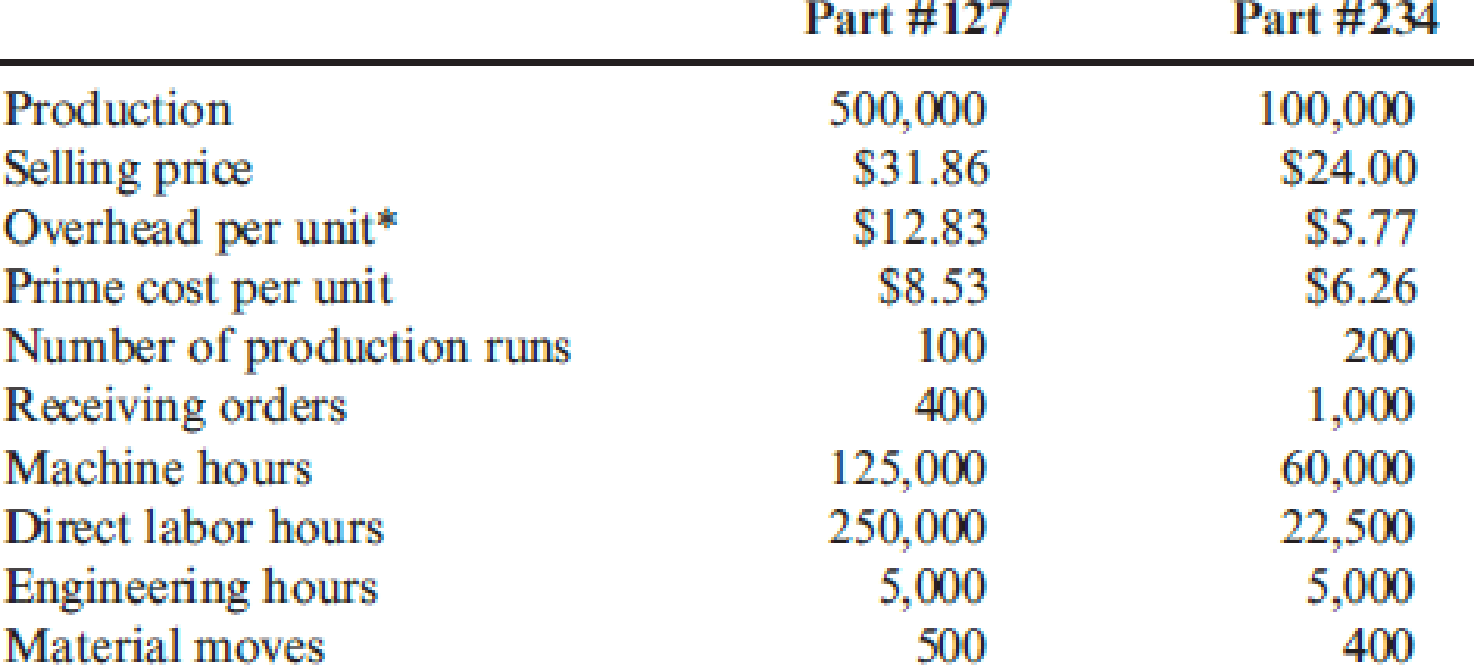

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234. Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after the addition of the new product. In the last two years, however, the plant faced intense competition, and its sales of Part #127 dropped. In fact, the plant showed a small loss in the most recent reporting period. Much of the competition was from foreign sources, and the plant manager was convinced that the foreign producers were guilty of selling the part below the cost of producing it. The following conversation between Patty Goodson, plant manager, and Joseph Fielding, divisional marketing manager, reflects the concerns of the division about the future of the plant and its products.

JOSEPH: You know, Patty, the divisional manager is real concerned about the plant’s trend. He indicated that in this budgetary environment, we can’t afford to carry plants that don’t show a profit. We shut one down just last month because it couldn’t handle the competition.

PATTY: Joe, you and I both know that Part #127 has a reputation for quality and value. It has been a mainstay for years. I don’t understand what’s happening.

JOSEPH: I just received a call from one of our major customers concerning Part #127. He said that a sales representative from another firm offered the part at $20 per unit—$11 less than what we charge. It’s hard to compete with a price like that. Perhaps the plant is simply obsolete.

PATTY: No. I don’t buy that. From my sources, I know we have good technology. We are efficient. And it’s costing a little more than $21 to produce that part. I don’t see how these companies can afford to sell it so cheaply. I’m not convinced that we should meet the price. Perhaps a better strategy is to emphasize producing and selling more of Part #234. Our margin is high on this product, and we have virtually no competition for it.

JOSEPH: You may be right. I think we can increase the price significantly and not lose business. I called a few customers to see how they would react to a 25 percent increase in price, and they all said that they would still purchase the same quantity as before.

PATTY: It sounds promising. However, before we make a major commitment to Part #234, I think we had better explore other possible explanations. I want to know how our production costs compare to those of our competitors. Perhaps we could be more efficient and find a way to earn our normal return on Part #127. The market is so much bigger for this part. I’m not sure we can survive with only Part #234. Besides, my production people hate that part. It’s very difficult to produce.

After her meeting with Joseph, Patty requested an investigation of the production costs and comparative efficiency. She received approval to hire a consulting group to make an independent investigation. After a three-month assessment, the consulting group provided the following information on the plant’s production activities and costs associated with the two products:

* Calculated using a plantwide rate based on direct labor hours. This is the current way of assigning the plant’s

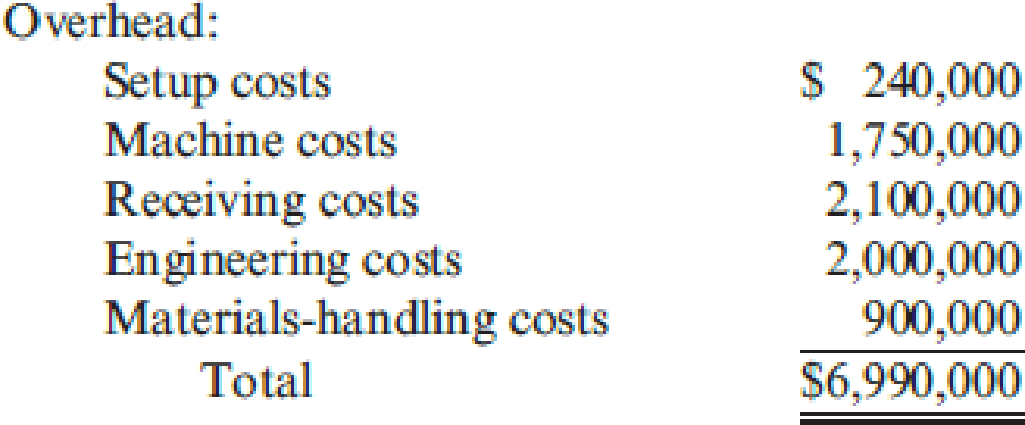

The consulting group recommended switching the overhead assignment to an activity-based approach. It maintained that activity-based cost assignment is more accurate and will provide better information for decision making. To facilitate this recommendation, it grouped the plant’s activities into homogeneous sets with the following costs:

Required:

- 1. Verify the overhead cost per unit reported by the consulting group using direct labor hours to assign overhead. Compute the per-unit gross margin for each product.

- 2. After learning of activity-based costing, Patty asked the controller to compute the product cost using this approach. Recompute the unit cost of each product using activity-based costing. Compute the per-unit gross margin for each product.

- 3. Should the company switch its emphasis from the high-volume product to the low-volume product? Comment on the validity of the plant manager’s concern that competitors are selling below the cost of making Part #127.

- 4. Explain the apparent lack of competition for Part #234. Comment also on the willingness of customers to accept a 25 percent increase in price for Part #234.

- 5. Assume that you are the manager of the plant. Describe what actions you would take based on the information provided by the activity-based unit costs.

Trending nowThis is a popular solution!

Chapter 4 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Wright Plastic Products is a small company that specialized in the production of plastic dinner plates until several years ago. Although profits for the company had been good, they have been declining in recent years because of increased competition. Many competitors offer a full range of plastic products, and management felt that this created a competitive disadvantage. The output of the companys plants was exclusively devoted to plastic dinner plates. Three years ago, management made a decision to add additional product lines. They determined that existing idle capacity in each plant could easily be adapted to produce other plastic products. Each plant would produce one additional product line. For example, the Atlanta plant would add a line of plastic cups. Moreover, the variable cost of producing a package of cups (one dozen) was virtually identical to that of a package of plastic plates. (Variable costs referred to here are those that change in total as the units produced change. The costs include direct materials, direct labor, and unit-based variable overhead such as power and other machine costs.) Since the fixed expenses would not change, the new product was forecast to increase profits significantly (for the Atlanta plant). Two years after the addition of the new product line, the profits of the Atlanta plant (as well as other plants) had not improvedin fact, they had dropped. Upon investigation, the president of the company discovered that profits had not increased as expected because the so-called fixed cost pool had increased dramatically. The president interviewed the manager of each support department at the Atlanta plant. Typical responses from four of those managers are given next. Materials handling: The additional batches caused by the cups increased the demand for materials handling. We had to add one forklift and hire additional materials handling labor. Inspection: Inspecting cups is more complicated than plastic plates. We only inspect a sample drawn from every batch, but you need to understand that the number of batches has increased with this new product line. We had to hire more inspection labor. Purchasing: The new line increased the number of purchase orders. We had to use more resources to handle this increased volume. Accounting: There were more transactions to process than before. We had to increase our staff. Required: 1. Explain why the results of adding the new product line were not accurately projected. 2. Could this problem have been avoided with an activity-based cost management system? If so, would you recommend that the company adopt this type of system? Explain and discuss the differences between an activity-based cost management system and a traditional cost management system.arrow_forwardBasuras Waste Disposal Company has a long-term contract with several large cities to collect garbage and trash from residential customers. To facilitate the collection, Basuras places a large plastic container with each household. Because of wear and tear, growth, and other factors, Basuras places about 200,000 new containers each year (about 20% of the total households). Several years ago, Basuras decided to manufacture its own containers as a cost-saving measure. A strategically located plant involved in this type of manufacturing was acquired. To help ensure cost efficiency, a standard cost system was installed in the plant. The following standards have been established for the products variable inputs: During the first week in January, Basuras had the following actual results: The purchasing agent located a new source of slightly higher-quality plastic, and this material was used during the first week in January. Also, a new manufacturing process was implemented on a trial basis. The new process required a slightly higher level of skilled labor. The higher- quality material has no effect on labor utilization. However, the new manufacturing process was expected to reduce materials usage by 0.25 pound per container. Required: 1. CONCEPTUAL CONNECTION Compute the materials price and usage variances. Assume that the 0.25 pound per container reduction of materials occurred as expected and that the remaining effects are all attributable to the higher-quality material. Would you recommend that the purchasing agent continue to buy this quality, or should the usual quality be purchased? Assume that the quality of the end product is not affected significantly. 2. CONCEPTUAL CONNECTION Compute the labor rate and efficiency variances. Assuming that the labor variances are attributable to the new manufacturing process, should it be continued or discontinued? In answering, consider the new processs materials reduction effect as well. Explain. 3. CONCEPTUAL CONNECTION Refer to Requirement 2. Suppose that the industrial engineer argued that the new process should not be evaluated after only one week. His reasoning was that it would take at least a week for the workers to become efficient with the new approach. Suppose that the production is the same the second week and that the actual labor hours were 9,000 and the labor cost was 99,000. Should the new process be adopted? Assume the variances are attributable to the new process. Assuming production of 6,000 units per week, what would be the projected annual savings? (Include the materials reduction effect.)arrow_forwardBienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.arrow_forward

- Otero Fibers, Inc., specializes in the manufacture of synthetic fibers that the company uses in many products such as blankets, coats, and uniforms for police and firefighters. Otero has been in business since 1985 and has been profitable every year since 1993. The company uses a standard cost system and applies overhead on the basis of direct labor hours. Otero has recently received a request to bid on the manufacture of 800,000 blankets scheduled for delivery to several military bases. The bid must be stated at full cost per unit plus a return on full cost of no more than 10 percent after income taxes. Full cost has been defined as including all variable costs of manufacturing the product, a reasonable amount of fixed overhead, and reasonable incremental administrative costs associated with the manufacture and sale of the product. The contractor has indicated that bids in excess of 30 per blanket are not likely to be considered. In order to prepare the bid for the 800,000 blankets, Andrea Lightner, cost accountant, has gathered the following information about the costs associated with the production of the blankets. Direct machine costs consist of items such as special lubricants, replacement of needles used in stitching, and maintenance costs. These costs are not included in the normal overhead rates. Otero recently developed a new blanket fiber at a cost of 750,000. In an effort to recover this cost, Otero has instituted a policy of adding a 0.50 fee to the cost of each blanket using the new fiber. To date, the company has recovered 125,000. Lightner knows that this fee does not fit within the definition of full cost, as it is not a cost of manufacturing the product. Required: 1. Calculate the minimum price per blanket that Otero Fibers could bid without reducing the companys operating income. 2. Using the full-cost criteria and the maximum allowable return specified, calculate Otero Fibers bid price per blanket. 3. Without prejudice to your answer to Requirement 2, assume that the price per blanket that Otero Fibers calculated using the cost-plus criteria specified is greater than the maximum bid of 30 per blanket allowed. Discuss the factors that Otero Fibers should consider before deciding whether or not to submit a bid at the maximum acceptable price of 30 per blanket. (CMA adapted)arrow_forwardPaladin Company manufactures plain-paper fax machines in a small factory in Minnesota. Sales have increased by 50 percent in each of the past three years, as Paladin has expanded its market from the United States to Canada and Mexico. As a result, the Minnesota factory is at capacity. Beryl Adams, president of Paladin, has examined the situation and developed the following alternatives. 1. Add a permanent second shift at the plant. However, the semiskilled workers who assemble the fax machines are in short supply, and the wage rate of 15 per hour would probably have to be increased across the board to 18 per hour in order to attract sufficient workers from out of town. The total wage increase (including fringe benefits) would amount to 125,000. The heavier use of plant facilities would lead to increased plant maintenance and small tool cost. 2. Open a new plant and locate it in Mexico. Wages (including fringe benefits) would average 3.50 per hour. Investment in plant and equipment would amount to 300,000. 3. Open a new plant and locate it in a foreign trade zone, possibly in Dallas. Wages would be somewhat lower than in Minnesota, but higher than in Mexico. The advantages of postponing tariff payments on parts imported from Asia could amount to 50,000 per year. Required: Advise Beryl of the advantages and disadvantages of each of her alternatives.arrow_forwardSteve Hausmann, a production engineer at Euro Fashion-USA, a European-style furniture company, was considering replacing a 1,000 lb capacity industrial forklift truck, which was purchased three years ago for $18,000. The truck was being used to move assembled furniture from the finishing department to the warehouse. Recently, the truck had not been dependable and had been frequently out of service while awaiting repairs, a situation that eventually cost the company $3,000. Maintenance expenses were rising steadily. When the truck was not available, the company had to rent one. In addition, the forklift truck was diesel operated, and workers in the plant were complaining about the air pollution. If retained, the truck would have required an immediate engine overhaul to keep it in operablecondition. The overhaul would have neither extended the originally estimated service life nor increased the value of the truck. Steve has found that the current truck has a book value of $0 (fully…arrow_forward

- TufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,000 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,000 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 149.00 Cost per drum: Direct materials $52.10 Direct labor ($18 per hour) 3.60 Manufacturing overhead 4.50 Selling and administrative expense 29.80 90.00 Margin per drum $ 59.00 Management…arrow_forwardTufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,000 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,000 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 149.00 Cost per drum: Direct materials $52.10 Direct labor ($18 per hour) 3.60 Manufacturing overhead 4.50 Selling and administrative expense 29.80 90.00 Margin per drum $ 59.00 Management…arrow_forwardTufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,000 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,000 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 149.00 Cost per drum: Direct materials (Variable) $52.10 Direct labor (Variable) 3.60 VariableManufacturing overhead…arrow_forward

- TufStuff, Inc., sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,000 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,000 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 149.00 Cost per drum: Direct materials $52.10 Direct labor ($18 per hour) 3.60 Manufacturing overhead 4.50 Selling and administrative expense 29.80 90.00 Margin per drum $ 59.00 Management…arrow_forwardTufStuff, Incorporated, sells a wide range of drums, bins, boxes, and other containers that are used in the chemical industry. One of the company’s products is a heavy-duty corrosion-resistant metal drum, called the WVD drum, used to store toxic wastes. Production is constrained by the capacity of an automated welding machine that is used to make precision welds. A total of 2,140 hours of welding time is available annually on the machine. Because each drum requires 0.4 hours of welding machine time, annual production is limited to 5,350 drums. At present, the welding machine is used exclusively to make the WVD drums. The accounting department has provided the following financial data concerning the WVD drums: WVD Drums Selling price per drum $ 177.00 Cost per drum: Direct materials $ 52.10 Direct labor ($25 per hour) 5.00 Manufacturing overhead 8.70 Selling and administrative expense 31.20 97.00 Margin per drum $ 80.00 Management believes 6,275…arrow_forwardTidwell, Inc., has two plants that manufacture a line of wheelchairs. One is located in Dallas, and the other in Oklahoma City. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for $1,782. Sales volume averages 20,000 units per year in each plant. Recently, the Dallas plant reduced the price of the tilt model to $1,584. Discussion with the Dallas manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called “non-value-added costs.” The Dallas manufacturing and selling costs for the tilt model were $1,386 per unit. The Dallas manager offered to loan the Oklahoma City plant his cost accounting manager to help it achieve similar results. The Oklahoma City plant manager readily agreed, knowing that his plant must keep pace—not only with the Dallas plant but also with competitors. A local competitor had also reduced its price on a similar model,…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College- Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College