Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN: 9781305970663

Author: Don R. Hansen, Maryanne M. Mowen

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 4, Problem 35P

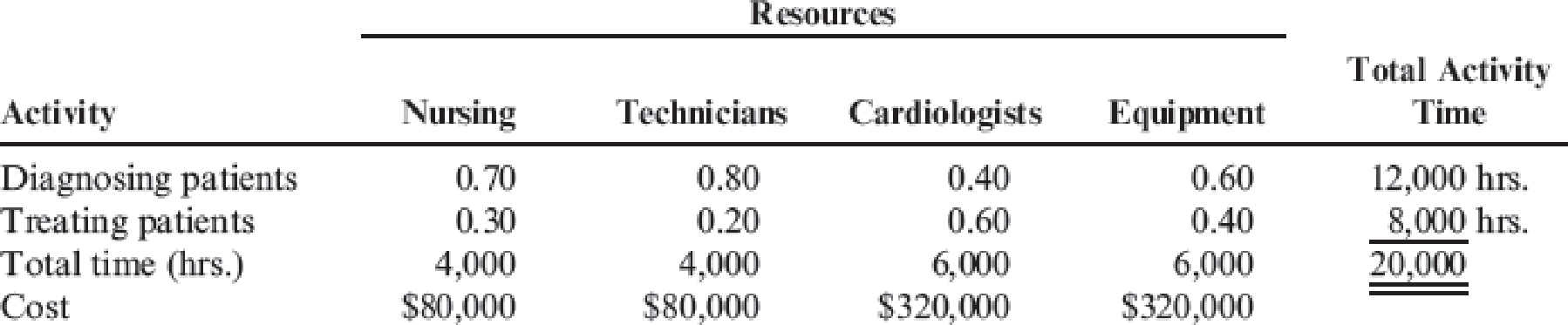

The Bienestar Cardiology Clinic has two major activities: diagnostic and treatment. The two activities use four resources: nursing, medical technicians, cardiologists, and equipment. Detailed interviews have provided the work distribution matrix shown below.

The total time estimated corresponds to practical capacity (interviewers adjusted the total time to about 80 percent of the available time). The equipment time is measured in machine hours. Thus, the total time (at practical capacity) in the system is 20,000 hours. In considering the implementation of a TDABC model, the following unit times and transaction information are also provided:

Required:

- 1. Calculate the cost of each activity using the indicated values of the resource drivers.

- 2. Calculate the capacity cost rate for TDABC. Using the capacity cost rate, calculate the cost of each activity under TDABC. Compare these values with those obtained in Requirement 1 and discuss possible reasons for any differences.

- 3. Suppose that the actual activity driver quantities are 3,500 and 9,000. Calculate the cost of unused capacity.

- 4. Suppose that the clinic acquires new equipment that reduces the total time required for the two activities from 6,000 to 4,000 hours. The equipment cost remains the same. Explain how the ABC system would be updated and then describe how TDABC would provide updates.

- 5. Suppose that diagnosing patients without any cardiac disease takes two hours while diagnosing patients with mildly diseased hearts takes an additional 1.5 hours and those with more severe problems takes an additional two hours. Prepare a time equation and, using the capacity cost rate from Requirement 2, calculate the activity rate for each of the three types of patients.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Elmo Clinic has identified three activities for daily maternity care: occupancy and feeding, nursing, and nursing supervision. The nursing supervisor oversees 150 nurses, 25 of whom are maternity nurses (the other nurses are located in other care areas such as the emergency room and intensive care). The nursing supervisor has three assistants, a secretary, several offices, computers, phones, and furniture. The three assistants spend 75% of their time on the supervising activity and 25% of their time as surgical nurses. They each receive a salary of $60,000. The nursing supervisor has a salary of $80,000. She spends 100% of her time supervising. The secretary receives a salary of $35,000 per year. Other costs directly traceable to the supervisory activity (depreciation, utilities, phone, etc.) average $170,000 per year.

Daily care output is measured as "patient days." The clinic has traditionally assigned the cost of daily care by using a daily rate (a rate per patient day). Daily rates…

The Vest School of Vocational Technology has organized the school training programs into three departments. Each department provides training in a different area as follows: nursing assistant, dental hygiene, and office technology. The school's owner, Candice Vest, wants to know how much it cost to operate each of the three departments. To accumulate the total cost for each department, the accountant has identified several indirect costs that must be allocated to each. These costs are $10,080 of telephone expense, $2,016 of supplies expense, $720,000 of office rent, $144,000 of janitorial services, and $150,000 of salary paid to the dean of students. To provide a reasonably accurate allocation of costs, the accountant has identified several possible cost drivers. These drivers and their association with each department follow.

Cost Driver Department 1 Department 2 Department 3

Number of telephone 28 16 19

Number of faculty members 20 16 12

Square footage of office space 28,000 16,800…

Jordan Company has identified three cost pools to allocate overhead costs. The following estimates are provided for the coming year:

Cost Pool Overhead Costs Cost driver Activity level

Supervision of direct labor $326,000 Direct labor-hours 900,000

Machine maintenance $132,000 Machine-hours 960,000

Facility rent $217,000 Square feet of area 100,000

Total overhead costs $675,000

The accounting records show the Mossman Job consumed the following resources:

Cost driver Actual level

Direct labor-hours 200

Machine-hours 1,500

Square feet of area 70

If direct labor-hours are considered the only overhead cost driver, what is the single cost driver rate for Jordan?

Chapter 4 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Ch. 4 - What is a predetermined overhead rate? Explain why...Ch. 4 - Describe what is meant by under- and overapplied...Ch. 4 - Explain how a plantwide overhead rate, using a...Ch. 4 - What are non-unit-related overhead activities?...Ch. 4 - What is an overhead consumption ratio?Ch. 4 - Overhead costs are the source of product cost...Ch. 4 - What is activity-based product costing?Ch. 4 - What are the six steps that define the design of...Ch. 4 - Explain how the cost of resources is assigned to...Ch. 4 - Prob. 10DQ

Ch. 4 - Identify and define two types of activity drivers.Ch. 4 - What are unit-level activities? Batch-level...Ch. 4 - Prob. 13DQCh. 4 - Prob. 14DQCh. 4 - Prob. 15DQCh. 4 - Prob. 1CECh. 4 - Warner Company has the following data for the past...Ch. 4 - Lansing. Inc., provided the following data for its...Ch. 4 - Larsen, Inc., produces two types of electronic...Ch. 4 - Roberts Company produces two weed eaters: basic...Ch. 4 - Golding Bank provided the following data about its...Ch. 4 - Golding Bank provided the following data about its...Ch. 4 - Electan Company produces two types of printers....Ch. 4 - Patterson Company produces wafers for integrated...Ch. 4 - Selected activities and other information are...Ch. 4 - Ripley, Inc., costs products using a normal...Ch. 4 - Predetermined Overhead Rate, Application of...Ch. 4 - Craig Company uses a predetermined overhead rate...Ch. 4 - Departmental Overhead Rates Mariposa, Inc.,...Ch. 4 - McCourt Company produces two types of leather...Ch. 4 - Deoro Company has identified the following...Ch. 4 - Prob. 17ECh. 4 - Secondary Activities Refer to the interview in...Ch. 4 - Bob Randall, cost accounting manager for Hemple...Ch. 4 - Prob. 20ECh. 4 - Bob Randall, cost accounting manager for Hemple...Ch. 4 - Silven Company has identified the following...Ch. 4 - Silven Company has identified the following...Ch. 4 - Gee Manufacturing produces two models of camshafts...Ch. 4 - Cushing, Inc., costs products using a normal...Ch. 4 - Nonunit-level drivers are prominent in...Ch. 4 - Plata Company has identified the following...Ch. 4 - Assume that the inspection activity has an...Ch. 4 - Consider the information given on two products and...Ch. 4 - Primera Company produces two products and uses a...Ch. 4 - Fisico Company produces exercise bikes. One of its...Ch. 4 - Prob. 32PCh. 4 - Glencoe First National Bank operated for years...Ch. 4 - Autotech Manufacturing is engaged in the...Ch. 4 - The Bienestar Cardiology Clinic has two major...Ch. 4 - Reducir, Inc., produces two different types of...Ch. 4 - Refer to the data given in Problem 4.36 and...Ch. 4 - Escuha Company produces two type of calculators:...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- A dedicated pharmaceutical plant uses the theory of constraints and has three processes: Mixing, Encapsulating, and Packaging. For Mixing, sufficient materials are released to produce 4,000 packages of product per day. Encapsulating has a buffer inventory of 8,000 units (work in process from Mixing). Packaging produces 4,000 units per day. Which of the three processes sets the production rate of 4,000 units per day? a. The Mixing Department b. The Encapsulating Department c. The Packaging Department d. Cannot be determinedarrow_forwardCorazon Manufacturing Company has a purchasing department staffed by five purchasing agents. Each agent is paid 28,000 per year and is able to process 4,000 purchase orders. Last year, 17,800 purchase orders were processed by the five agents. Required: 1. Calculate the activity rate per purchase order. 2. Calculate, in terms of purchase orders, the: a. total activity availability b. unused capacity 3. Calculate the dollar cost of: a. total activity availability b. unused capacity 4. Express total activity availability in terms of activity capacity used and unused capacity. 5. What if one of the purchasing agents agreed to work half time for 14,000? How many purchase orders could be processed by four and a half purchasing agents? What would unused capacity be in purchase orders?arrow_forwardCarsen Company produces handcrafted pottery that uses two inputs: materials and labor. During the past quarter, 24,000 units were produced, requiring 96,000 pounds of materials and 48,000 hours of labor. An engineering efficiency study commissioned by the local university revealed that Carsen can produce the same 24,000 units of output using either of the following two combinations of inputs: The cost of materials is 8 per pound; the cost of labor is 12 per hour. Required: 1. Compute the output-input ratio for each input of Combination F1. Does this represent a productivity improvement over the current use of inputs? What is the total dollar value of the improvement? Classify this as a technical or an allocative efficiency improvement. 2. Compute the output-input ratio for each input of Combination F2. Does this represent a productivity improvement over the current use of inputs? Now, compare these ratios to those of Combination F1. What has happened? 3. Compute the cost of producing 24,000 units of output using Combination F1. Compare this cost to the cost using Combination F2. Does moving from Combination F1 to Combination F2 represent a productivity improvement? Explain.arrow_forward

- Pelder Products Company manufactures two types of engineering diagnostic equipment used in construction. The two products are based upon different technologies, X-ray and ultrasound, but are manufactured in the same factory. Pelder has computed the manufacturing cost of the X-ray and ultrasound products by adding together direct materials, direct labor, and overhead cost applied based on the number of direct labor hours. The factory has three overhead departments that support the single production line that makes both products. Budgeted overhead spending for the departments is as follows: Pelders budgeted manufacturing activities and costs for the period are as follows: The budgeted cost to manufacture one ultrasound machine using the activity-based costing method is: a. 225. b. 264. c. 293. d. 305.arrow_forwardJacson Company produces two brands of a popular pain medication: regular strength and extra strength. Regular strength is produced in tablet form, and extra strength is produced in capsule form. All direct materials needed for each batch are requisitioned at the start. The work orders for two batches of the products are shown below, along with some associated cost information: In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year were 60,000 for direct labor and 190,000 for overhead. Budgeted direct labor hours were 5,000. It takes one minute of labor time to mix the ingredients needed for a 100-unit bottle (for either product). In the Bottling Department, conversion costs are applied on the basis of machine hours. Budgeted conversion costs for the department for the year were 400,000. Budgeted machine hours were 20,000. It takes one-half minute of machine time to fill a bottle of 100 units. Required: 1. What are the conversion costs applied in the Mixing Department for each batch? The Bottling Department? 2. Calculate the cost per bottle for the regular and extra strength pain medications. 3. Prepare the journal entries that record the costs of the 12,000 regular strength batch as it moves through the various operations. 4. Suppose that the direct materials are requisitioned by each department as needed for a batch. For the 12,000 regular strength batch, direct materials are requisitioned for the Mixing and Bottling departments. Assume that the amount of cost is split evenly between the two departments. How will this change the journal entries made in Requirement 3?arrow_forwardVargas, Inc., produces industrial machinery. Vargas has a machining department and a group of direct laborers called machinists. Each machinist is paid 25,000 and can machine up to 500 units per year. Vargas also hires supervisors to develop machine specification plans and to oversee production within the machining department. Given the planning and supervisory work, a supervisor can oversee three machinists, at most. Vargass accounting and production history reveal the following relationships between units produced and the costs of direct labor and supervision (measured on an annual basis): Required: 1. Prepare two graphs: one that illustrates the relationship between direct labor cost and units produced, and one that illustrates the relationship between the cost of supervision and units produced. Let cost be the vertical axis and units produced the horizontal axis. 2. How would you classify each cost? Why? 3. Suppose that the normal range of activity is between 2,400 and 2,450 units and that the exact number of machinists is currently hired to support this level of activity. Further suppose that production for the next year is expected to increase by an additional 400 units. How much will the cost of direct labor increase (and how will this increase be realized)? Cost of supervision?arrow_forward

- "The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agent has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward"The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agent has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward"The controller for Tulsa Medical Supply Company has established the following activity cost pools and cost drivers. Activity Cost Pool Budgeted Overhead cost Cost Driver Budgeted Level for cost Driver Pool Rate Machine Setups $250,000 Number of Setups 125 $2,000 per setup Material Handling 75,000 Weight of Raw Material 37,500 Lb. $2 per pound Hazardous Waste Control 25,000 Weight of hazardous Chemical used 5,000 Lb. $5 per pound Quality Control 75,000 Numbers of Inspections 1,000 $75 per inspection Other Overhead cost 200,000 Machine Hours 20,000 $10 per hours Total $625,000 An order for 1,000 boxes of medical-testing agents has the following production requirements Machine setups ...............................................................................................5 setups Raw material .........................................................................................10,000…arrow_forward

- The Radiology Department provides imaging services for Emergency Medical Center. One important activity in the Radiology Department is transcribing digitally recorded analyses of images into a written report. The manager of the Radiology Department determined that the average transcriptionist could type 700 lines of a report in an hour. The plan for the first week in May called for 81,900 typed lines to be written. The Radiology Department has three transcriptionists. Each transcriptionist is hired from an employment firm that requires temporary employees to be hired for a minimum of a 40-hour week. Transcriptionists are paid $23.00 per hour. The manager offered a bonus if the department could type more lines for the week, without overtime. Due to high service demands, the transcriptionists typed more lines in the first week of May than planned. The actual amount of lines typed in the first week of May was 88,900 lines, without overtime. As a result, the bonus caused the average…arrow_forwardCaldwell Home Appliances Inc. is estimating the activity cost associated with producing ovens and refrigerators. The indirect labor can be traced into four separate activity pools, based on time records provided by the employees. The budgeted activity cost and activity-base information are provided as follows: Activity Activity Pool Cost Activity Base Procurement $12,600 Number of purchase orders Scheduling 90,000 Number of production orders Materials handling 11,000 Number of moves Product development 50,000 Number of engineering changes Total cost $163,600 The estimated activity-base usage and unit information for two product lines was determined as follows: Number ofPurchase Orders Number ofProduction Orders Number ofMoves Number ofEngineering Change Orders Units Ovens 400 800 300 80 1,000 Refrigerators 300 400 200 120 500 Totals 700 1,200 500 200 1,500 a.…arrow_forwardCaldwell Home Appliances Inc. is estimating the activity cost associated with producing ovens and refrigerators. The indirect labor can be traced into four separate activity pools, based on time records provided by the employees. The budgeted activity cost and activity-base information are provided as follows: Activity Activity Pool Cost Activity Base Procurement $12,600 Number of purchase orders Scheduling 90,000 Number of production orders Materials handling 11,000 Number of moves Product development 50,000 Number of engineering changes Total cost $163,600 The estimated activity-base usage and unit information for two product lines was determined as follows: Number ofPurchase Orders Number ofProduction Orders Number ofMoves Number ofEngineering Change Orders Units Ovens 400 800 300 80 1,000 Refrigerators 300 400 200 120 500 Totals 700 1,200 500 200 1,500 a.…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

What is Cost Allocation? Definition & Process; Author: FloQast;https://www.youtube.com/watch?v=hLhvvHvZ3JM;License: Standard Youtube License