Concept explainers

Videos

(Appendix 4A) Predetermined

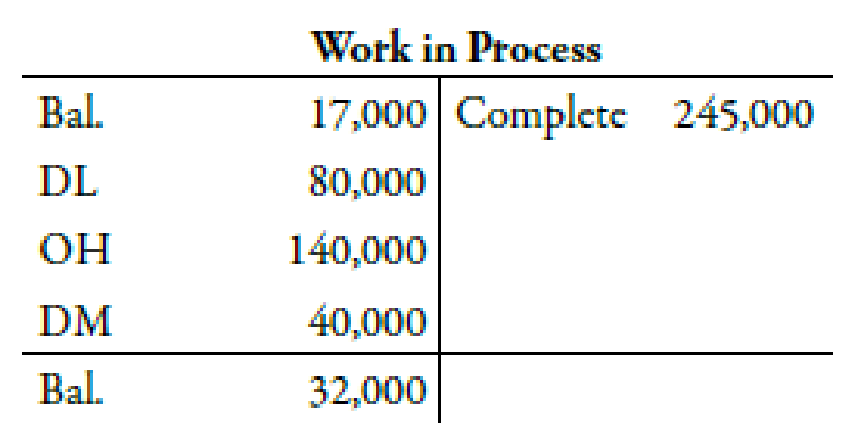

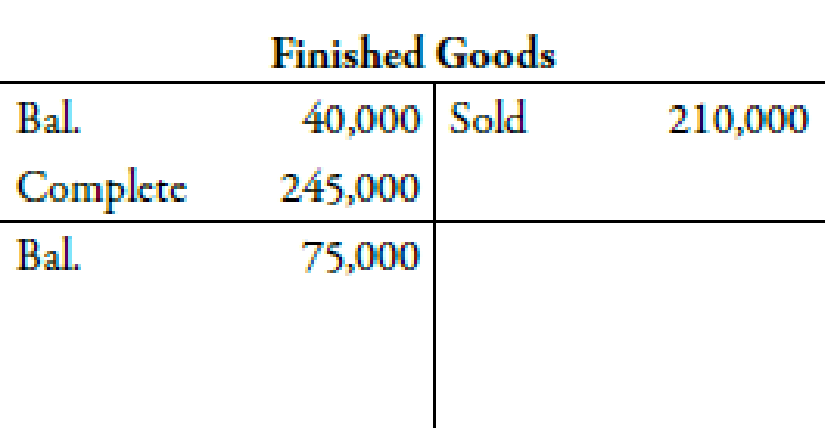

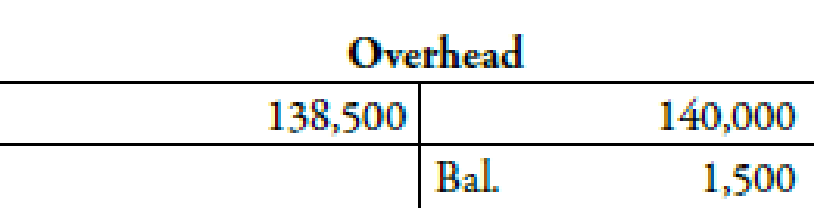

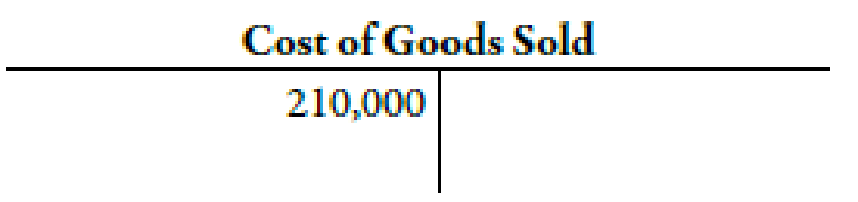

Barrymore Costume Company, located in New York City, sews costumes for plays and musicals. Barrymore considers itself primarily a service firm, as it never produces costumes without a preexisting order and only purchases materials to the specifications of the particular job. Any finished goods ending inventory is temporary and is zeroed out as soon as the show producer pays for the order. Overhead is applied on the basis of direct labor cost. During the first quarter of the year, the following activity took place in each of the accounts listed:

Job 32 was the only job in process at the end of the first quarter. A total of 1,000 direct labor hours at $10 per hour were charged to Job 32.

Required:

- 1. Assuming that overhead is applied on the basis of direct labor cost, what was the overhead rate used during the first quarter of the year?

- 2. What was the applied overhead for the first quarter? The actual overhead? The under- or overapplied overhead?

- 3. What was the cost of goods manufactured for the quarter?

- 4. Assume that the overhead variance is closed to the cost of goods sold account. Prepare the

journal entry to close out the overhead control account. What is the adjusted balance in Cost of Goods Sold? - 5. For Job 32, identify the costs incurred for direct materials, direct labor, and overhead.

Trending nowThis is a popular solution!

Chapter 4 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Maney Televisions utilizes a traditional overhead allocation method, and has determined that overhead costs are driven by direct labor hours. Relevant cost information is provided below. Total estimated overhead costs $650,000 Total estimated DL hours 130,000 Actual overhead costs $640,300 Actual DL hours 127,500 The unadjusted cost of goods sold balance at the end of the year is $56,000. What is the overhead variance? Please provide your answer as a positive number rounded to the nearest whole dollar.arrow_forwardMethod of Least Squares, Predicting Cost for Different Time Periods from the One Used to Develop a Cost Formula Farnsworth Company has gathered data on its overhead activities and associated costs for the past 10 months. Tracy Heppler, a member of the controller's department, has convinced management that overhead costs can be better estimated and controlled if the fixed and variable components of each overhead activity are known. One such activity is receiving raw materials (unloading incoming goods, counting goods, and inspecting goods), which she believes is driven by the number of receiving orders. Ten months of data have been gathered for the receiving activity and are as follows: Month Receiving Orders Receiving Cost 1 1,000 $18,000 2 700 $15,000 3 1,500 $28,000 4 1,200 $17,000 5 1,300 $25,000 6 1,100 $21,000 7 1,600 $29,000 8 1,400 $24,000 9 1,700 $27,000 10 900 $16,000 Assume that Tracy…arrow_forwardWhich of the following is not a reason to allocate overhead? Some overhead costs are seasonal and should be spread over production for the entire year. Unlike direct materials and direct labor, the amount of overhead actually incurred may not be known at the time a job is being worked on. Allocation is more accurate than tracing items directly to jobs. Manufacturing overhead is an indirect cost that cannot be physically or economically traced back to a specific item.arrow_forward

- Wright Brothers is debating the use of direct labor cost or direct labor hours as the cost allocation base for allocating manufacturing overhead. The following information is available for the year ended Dec 31, 2007. Estimated labor cost $449,500 Actual direct labor cost $441,000 Estimated manufacturing overhead $359,600 Actual manufacturing overhead costs $338,000 Actual direct labor hours $242,000 Using direct labour hours as the cost driver, the journal entry to dispose of the manufacturing overhead variance is: Select one: a. Dr. Manufacturing Overhead $14,800 and Cr. COGS $14,800 b. Dr. Manufacturing overhead $12,900 and Cr. COGS $12,900 c. Dr. COGS $14,800 and Cr. Manufacturing Overhead $14,800 d. Dr. WIP $12,900 and Cr. Manufacturing Overhead $12,900arrow_forwardAs part of its cost control program, Tracer Companyuses a standard costing system for all manufactureditems. The standard cost for each item is established atthe beginning of the fiscal year, and the standards are not revised until thebeginning of the next fiscal year. Changes in costs, caused during the year bychanges in direct materials or direct labor inputs or by changes in themanufacturing process, are recognized as they occur by the inclusion ofplanned variances in Tracer's monthly operating budgets.The following direct labor standard was established for one of Tracer'sproducts, effective June 1, 2012, the beginning of the fiscal year: Assembler A labor (5 hrs @ $10) $50 Assembler B labor (3 hrs @$11) 33 Machinist labor (2 hrs @$15) 30 Standard cost per 100 units $113 The standard was based on the direct labor being performed by a teamconsisting of five persons with Assembler A skills, three persons withAssembler B skills, and two persons with machinist skills; this team…arrow_forwardSama Company is a contract manufacturer for a variety of pharmaceutical and over-the-counter products. It has a reputation for operational excellence and boasts a normal spoilage rate of 2% of normal input. Normal spoilage is recognized during the budgeting process and is classified as a component of manufacturing overhead when determining the overhead rate. Lynn Sanger, one of Flextron’s quality control managers, obtains the following information for Job No. M102, an order from a consumer products company. The order was completed recently, just before the close of Flextron’s fiscal year. The units will be delivered early in the next accounting period. A total of 128,500 units were started, and 6,000 spoiled units were rejected at final inspection, yielding 122,500 good units. Spoiled units were sold at $4 per unit. Sanger indicates that all spoilage was related to this specific job. The total costs for all 128,500 units of Job No. M102 follow. The job has been completed, but the costs…arrow_forward

- Sama Company is a contract manufacturer for a variety of pharmaceutical and over-the-counter products. It has a reputation for operational excellence and boasts a normal spoilage rate of 2% of normal input. Normal spoilage is recognized during the budgeting process and is classified as a component of manufacturing overhead when determining the overhead rate. Lynn Sanger, one of Flextron’s quality control managers, obtains the following information for Job No. M102, an order from a consumer products company. The order was completed recently, just before the close of Flextron’s fiscal year. The units will be delivered early in the next accounting period. A total of 128,500 units were started, and 6,000 spoiled units were rejected at final inspection, yielding 122,500 good units. Spoiled units were sold at $4 per unit. Sanger indicates that all spoilage was related to this specific job. The total costs for all 128,500 units of Job No. M102 follow. The job has been completed, but the…arrow_forwardScattergraph, High–Low Method, and Predicting Cost for a Different Time Period from the One Used to Develop a Cost Formula Farnsworth Company has gathered data on its overhead activities and associated costs for the past 10 months. Tracy Heppler, a member of the controller's department, has convinced management that overhead costs can be better estimated and controlled if the fixed and variable components of each overhead activity are known. One such activity is receiving raw materials (unloading incoming goods, counting goods, and inspecting goods), which she believes is driven by the number of receiving orders. Ten months of data have been gathered for the receiving activity and are as follows: Month Receiving Orders Receiving Cost ($) 1 1,000 27,000 2 700 22,500 3 1,500 42,000 4 1,200 25,500 5 1,300 37,500 6 1,100 31,500 7 1,600 43,500 8 1,400 36,000 9 1,700 40,500 10 900 24,000 Required: 1. On your own paper, prepare a scattergraph based on the 10…arrow_forwardPotter Company has installed a JIT purchasing and manufacturing system and is using back-flush accounting for its cost flows. It currently uses a two-trigger approach with the purchase of materials as the first trigger point and the completion of goods as the second trigger point. During the month of June, Potter had the following transactions: 40,500 labor plus 222,750 overhead. There were no beginning or ending inventories. All goods produced were sold with a 60 percent markup. Any variance is closed to Cost of Goods Sold. (Variances are recognized monthly.) Required: Prepare the journal entries for the month of June using backflush costing, assuming that Potter uses the sale of goods as the second trigger point instead of the completion of goods.arrow_forward

- Yohan Company has the following balances in its direct materials and direct labor variance accounts at year-end: Unadjusted Cost of Goods Sold equals 1,500,000, unadjusted Work in Process equals 236,000, and unadjusted Finished Goods equals 180,000. Required: 1. Assume that the ending balances in the variance accounts are immaterial and prepare the journal entries to close them to Cost of Goods Sold. What is the adjusted balance in Cost of Goods Sold after closing out the variances? 2. What if any ending balance in a variance account that exceeds 10,000 is considered material? Close the immaterial variance accounts to Cost of Goods Sold and prorate the material variances among Cost of Goods Sold, Work in Process, and Finished Goods on the basis of prime costs in these accounts. The prime cost in Cost of Goods Sold is 1,050,000, the prime cost in Work in Process is 165,200, and the prime cost in Finished Goods is 126,000. What are the adjusted balances in Work in Process, Finished Goods, and Cost of Goods Sold after closing out all variances? (Round ratios to four significant digits. Round journal entries to the nearest dollar.)arrow_forwardCost and production data for Binghamton Beverages Inc. are presented as follows: Required: Calculate net variances for materials, labor, and factory overhead. Calculate specific materials and labor variances by department, using the diagram format in Figure 8-4. Comment on the possible causes for each of the variances that you computed. Make all journal entries to record production costs in Work in Process and Finished Goods. Determine the balance of ending Work in Process in each department. Assume that 4,000 units were sold at $40 each. Calculate the gross margin based on standard cost. Calculate the gross margin based on actual cost. Why does the gross margin at actual cost differ from the gross margin at standard cost. As the plant controller, you present the variance report in Item 1 above to Paul Crooke, the plant manager. After reading it, Paul states: “If we present this performance report to corporate with that large unfavorable labor variance in Blending, nobody in the plant will receive a bonus. Those standard hours of 5,500 are way too tight for this production process. Fifty-eight hundred hours would be more reasonable, and that would result in a favorable labor efficiency variance that would more than offset the unfavorable labor rate variance. Please redo the variance calculations using 5,800 hours as the standard.” You object, but Paul ends the conversation with, “That is an order.” What standards of ethical professional practice would be violated if you adhered to Paul’s order? How would you attempt to resolve this ethical conflict?arrow_forwardAs part of its cost control program, Tracer Company uses a standard costing system for all manufactured items. The standard cost for each item is established at the beginning of the fiscal year, and the standards are not revised until the beginning of the next fiscal year. Changes in costs, caused during the year by changes in direct materials or direct labor inputs or by changes in the manufacturing process, are recognized as they occur by the inclusion of planned variances in Tracers monthly operating budgets. The following direct labor standard was established for one of Tracers products, effective June 1, 2012, the beginning of the fiscal year: The standard was based on the direct labor being performed by a team consisting of five persons with Assembler A skills, three persons with Assembler B skills, and two persons with machinist skills; this team represents the most efficient use of the companys skilled employees. The standard also assumed that the quality of direct materials that had been used in prior years would be available for the coming year. For the first seven months of the fiscal year, actual manufacturing costs at Tracer have been within the standards established. However, the company has received a significant increase in orders, and there is an insufficient number of skilled workers to meet the increased production. Therefore, beginning in January, the production teams will consist of eight persons with Assembler A skills, one person with Assembler B skills, and one person with machinist skills. The reorganized teams will work more slowly than the normal teams, and as a result, only 80 units will be produced in the same time period in which 100 units would normally be produced. Faulty work has never been a cause for units to be rejected in the final inspection process, and it is not expected to be a cause for rejection with the reorganized teams. Furthermore, Tracer has been notified by its direct materials supplier that lower-quality direct materials will be supplied beginning January 1. Normally, one unit of direct materials is required for each good unit produced, and no units are lost due to defective direct materials. Tracer estimates that 6 percent of the units manufactured after January 1 will be rejected in the final inspection process due to defective direct materials. Required: 1. Determine the number of units of lower quality direct materials that Tracer Company must enter into production in order to produce 47,000 good finished units. 2. How many hours of each class of direct labor must be used to manufacture 47,000 good finished units? 3. Determine the amount that should be included in Tracers January operating budget for the planned direct labor variance caused by the reorganization of the direct labor teams and the lower quality direct materials. (CMA adapted)arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning