Videos

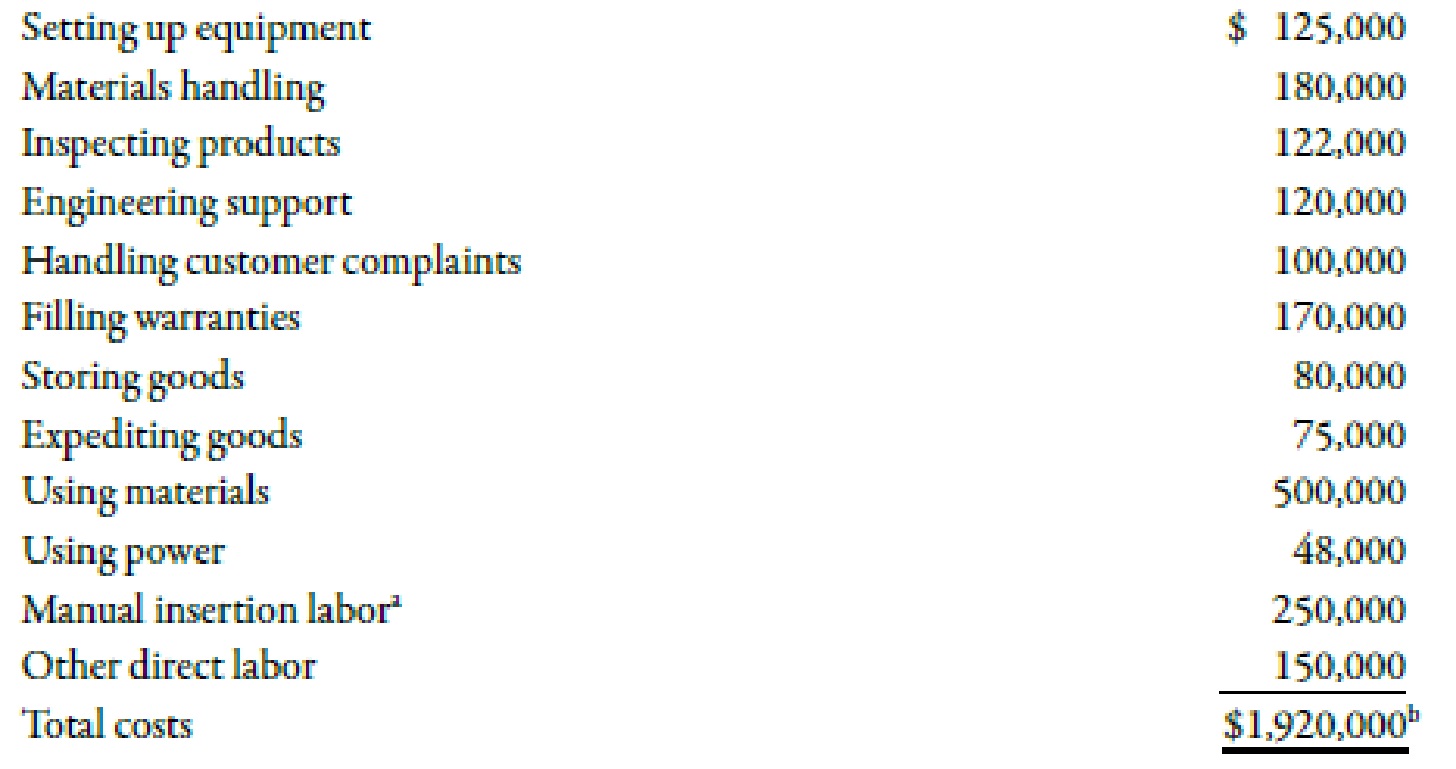

Danna Martin, president of Mays Electronics, was concerned about the end-of-the year marketing report that she had just received. According to Larry Savage, marketing manager, a price decrease for the coming year was again needed to maintain the company’s annual sales volume of integrated circuit boards (CBs). This would make a bad situation worse. The current selling price of $18 per unit was producing a $2-per-unit profit—half the customary $4-per-unit profit. Foreign competitors kept reducing their prices. To match the latest reduction would reduce the price from $18 to $14. This would put the price below the cost to produce and sell it. How could these firms sell for such a low price? Determined to find out if there were problems with the company’s operations, Danna decided to hire a consultant to evaluate the way in which the CBs were produced and sold. After two weeks, the consultant had identified the following activities and costs:

The consultant indicated that some preliminary activity analysis shows that per-unit costs can be reduced by at least $7. Since the marketing manager had indicated that the market share (sales volume) for the boards could be increased by 50% if the price could be reduced to $12, Danna became quite excited.

Required:

- 1. CONCEPTUAL CONNECTION What is activity-based management? What phases of activity analysis did the consultant provide? What else remains to be done?

- 2. CONCEPTUAL CONNECTION Identify as many nonvalue-added costs as possible. Compute the cost savings per unit that would be realized if these costs were eliminated. Was the consultant correct in the preliminary cost reduction assessment? Discuss actions that the company can take to reduce or eliminate the nonvalue-added activities.

- 3. Compute the unit cost required to maintain current market share, while earning a profit of $4 per unit. Now compute the unit cost required to expand sales by 50%, assuming a per-unit profit of $4. How much cost reduction would be required to achieve each unit cost?

- 4. Assume that further activity analysis revealed the following: switching to automated insertion would save $60,000 of engineering support and $90,000 of direct labor. Now, what is the total potential cost reduction per unit available from activity analysis? With these additional reductions, can Mays achieve the unit cost to maintain current sales? To increase it by 50%? What form of activity analysis is this: reduction, sharing, elimination, or selection?

- 5. CONCEPTUAL CONNECTION Calculate income based on current sales, prices, and costs. Then calculate the income by using a $14 price and a $12 price, assuming that the maximum cost reduction possible is achieved (including Requirement 4’s reduction). What price should be selected?

1.

Explain activity based management. Discuss the phases that are provided by the consultant. Also, explain the other phases that need to be done in an organization.

Explanation of Solution

Activity Based Costing (ABC):

Activity based costing is a apportionment of costs that first considers the activity drivers that helps in the allocation of costs to various activities and then allocates costs to different cost objects by using the drivers.

Activity based management is a technique that focuses on the attention of management towards the various activities. It includes two dimensions that is a cost dimension and a process dimension. Activity based management are identifying the activities, evaluating their values and continuing only value-adding activities. The consultant only identifying the activities but does not categorize the activities as value-added activity or non-value added activity. Also, consultant does not give any suggestions for increasing efficiency of use of activities. The consultant only eliminates non-value added activities for increasing the potential savings. Therefore, activity based management suggest how to reduce, remove, share and choose various activities in order to get the cost reductions.

2.

Calculate the cost savings per unit that would be realized if these costs were eliminated. Identify whether the consultant correct in the preliminary cost reduction assessment. Also, explain the actions that company can take to reduce or eliminate the non-value added activities.

Explanation of Solution

| Particulars |

Amount ($) |

| Setting up equipment | 125,000 |

| Materials handling | 180,000 |

| Inspecting products | 122,000 |

| Handling customer complaints | 100,000 |

| Filling warranties | 170,000 |

| Storing goods | 80,000 |

| Expediting goods | 75,000 |

| Total (A) | 852,000 |

| Units produced and sold (B) | 120,0001 |

| Potential unit cost reduction | 7.10 |

Table (1)

Consultant is able to achieve its target. On the basis of above calculation, per unit costs is reduced by $7.10 and consultant is also able to reduce further costs by improving the value-added activities.

Currently, an organization earns $2 per unit profit. If an organization decreases the cost per unit to $4 per unit, then their current sales and profit is $14 at a price. Also, if an organization savings the cost, then the company is able to earn additional profit.

Working Note:

1.

Calculation of units produced and sold:

3.

Calculate the unit cost required to maintain the current market share while earning a profit of $4 per unit. Calculate the unit cost required to expand sale by 50%. Also, discuss how much cost reduction is needed to attain the each unit cost.

Explanation of Solution

Use the following formula to calculate the unit cost to maintain sales:

Substitute $14 for latest reduction and $4 for profit per unit in the above formula.

Therefore, unit cost to maintain sales is $10.

Use the following formula to calculate the unit cost to expand sales:

Substitute $12 for latest reduction and $4 for profit per unit in the above formula.

Therefore, unit cost to expand sales is $8.

Use the following formula to calculate the cost reduction to maintain sales:

Substitute $16 for current sales and $10 for unit cost to maintain sales in the above formula.

Therefore, cost reduction to maintain sales is $6.

Use the following formula to calculate the cost reduction to expand sales:

Substitute $16 for current sales and $8 for unit cost to expand sales in the above formula.

Therefore, cost reduction to expand sales is $8.

4.

Calculate the total potential cost reduction per unit. Also, identify the form of activity as a reduction, sharing, elimination or selection.

Explanation of Solution

| Particulars |

Amount ($) |

| Total potential reduction | 852,000 |

| Automated Cost | 150,000 |

| Total (A) | 1,002,000 |

| Units (B) | 120,000 |

| Units savings | 8.35 |

Table (2)

Therefore, company needs to decrease the cost by $8.35 to maintain the current market share. If company removes the non-value added costs, then the cost reduction increases the market share. In the given problem, activity selection is uses in the activity management.

5.

Compute the income based on current sales, prices and costs. Also, compute the income with the help of $14 price and a $12 price.

Explanation of Solution

Calculation of the income on the basis of current sales:

| Particulars |

Amount ($) |

| Sales | 2,160,000 |

| Less: Costs | 1,920,000 |

| Income | 240,000 |

Table (3)

Calculation of the income when the price is $14:

| Particulars |

Amount ($) |

| Sales | 1,680,000 |

| Less: Costs | 918,000 |

| Income | 762,000 |

Table (4)

Calculation of the income when the price is $12:

| Particulars |

Amount ($) |

| Sales | 2,160,000 |

| Less: Costs | 1,377,000 |

| Income | 783,000 |

Table (5)

Therefore, if company is adopting the price of $12, then company is able to earn maximum profit.

Working Note:

1.

Calculation of cost rate:

Want to see more full solutions like this?

Chapter 5 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Boxer Production, Inc., is in the process of considering a flexible manufacturing system that will help the company react more swiftly to customer needs. The controller, Mick Morrell, estimated that the system will have a 10-year life and a required return of 10% with a net present value of negative $500,000. Nevertheless, he acknowledges that he did not quantify the potential sales increases that might result from this improvement on the issue of on-time delivery, because it was too difficult to quantify. If there is a general agreement that qualitative factors may offer an additional net cash flow of $150,000 per year, how should Boxer proceed with this Investment?arrow_forwardMoses Moonrocks Inc. has developed a balanced scorecard with a measure map that suggests that the number of erroneous shipments has a direct effect on operating profit. The company estimates that every shipment error leads to a reduction of revenue by 3,000 and increased costs of about 2,000. If the company has the following budgeted sales and costs for next month (without accounting for any possible shipping errors), determine how many shipping errors the company can afford to have and still break even:arrow_forwardDanna Wise, president of Tidwell Company, recently returned from a conference on quality and productivity. At the conference, she was told that many American firms have quality costs totaling 20 to 30% of sales. The quality experts at the conference convinced her that a company could increase its profitability by improving quality. However, she was of the opinion that the quality of Tidwell Company was much less than 20%probably more in the 4 to 6% range. However, because the potential for increasing profits was so great if she was wrong, she decided to request a preliminary estimate of the total quality costs currently being incurred. She asked her controller for a summary of quality costs, with the costs classified into four categories: prevention, appraisal, internal failure, or external failure. She also wanted the costs expressed as a percentage of both sales and profits. The controller had his staff assemble the following information from the past year, 20X1: a. Sales revenue, 37,240,000; net income, 4,000,000. b. During the year, customers returned 40,000 units needing repair. Repair cost averages 9 per unit. c. Twelve inspectors are employed, each earning an annual salary of 80,000. The inspectors are involved only with final inspection (product acceptance). d. Total scrap is 200,000 units. Of this total, ninety percent is quality related. The cost of scrap is about 10 per unit. e. Each year, approximately 800,000 units are rejected in final inspection. Of these units, seventy-five percent can be recovered through rework. The cost of rework is 1.80 per I unit. f. A customer cancelled an order that would have increased profits by 600,000. The customers reason for cancellation was poor product performance. g. The company employs 10 full-time employees in its complaint department. Each earns 48,600 a year. h. The company gave sales allowances totaling 180,000 due to substandard products being sent to the customer. i. The company requires all new employees to take its 4-hour quality training program. The estimated annual cost of the program is 120,000. Required: 1. Prepare a simple quality cost report classifying costs by category. 2. Compute the quality cost-sales ratio. Also, compare the total quality costs with total profits. Should Danna be concerned with the level of quality costs? 3. Prepare a pie chart for the quality costs. Discuss the distribution of quality costs among the four categories. Are they properly distributed? Explain. 4. Discuss how the company can improve its overall quality and at the same time reduce total quality costs. 5. By how much will profits increase if quality costs are reduced to 3% of sales?arrow_forward

- At the beginning of the last quarter of 20x1, Youngston, Inc., a consumer products firm, hired Maria Carrillo to take over one of its divisions. The division manufactured small home appliances and was struggling to survive in a very competitive market. Maria immediately requested a projected income statement for 20x1. In response, the controller provided the following statement: After some investigation, Maria soon realized that the products being produced had a serious problem with quality. She once again requested a special study by the controllers office to supply a report on the level of quality costs. By the middle of November, Maria received the following report from the controller: Maria was surprised at the level of quality costs. They represented 30 percent of sales, which was certainly excessive. She knew that the division had to produce high-quality products to survive. The number of defective units produced needed to be reduced dramatically. Thus, Maria decided to pursue a quality-driven turnaround strategy. Revenue growth and cost reduction could both be achieved if quality could be improved. By growing revenues and decreasing costs, profitability could be increased. After meeting with the managers of production, marketing, purchasing, and human resources, Maria made the following decisions, effective immediately (end of November 20x1): a. More will be invested in employee training. Workers will be trained to detect quality problems and empowered to make improvements. Workers will be allowed a bonus of 10 percent of any cost savings produced by their suggested improvements. b. Two design engineers will be hired immediately, with expectations of hiring one or two more within a year. These engineers will be in charge of redesigning processes and products with the objective of improving quality. They will also be given the responsibility of working with selected suppliers to help improve the quality of their products and processes. Design engineers were considered a strategic necessity. c. Implement a new process: evaluation and selection of suppliers. This new process has the objective of selecting a group of suppliers that are willing and capable of providing nondefective components. d. Effective immediately, the division will begin inspecting purchased components. According to production, many of the quality problems are caused by defective components purchased from outside suppliers. Incoming inspection is viewed as a transitional activity. Once the division has developed a group of suppliers capable of delivering nondefective components, this activity will be eliminated. e. Within three years, the goal is to produce products with a defect rate less than 0.10 percent. By reducing the defect rate to this level, marketing is confident that market share will increase by at least 50 percent (as a consequence of increased customer satisfaction). Products with better quality will help establish an improved product image and reputation, allowing the division to capture new customers and increase market share. f. Accounting will be given the charge to install a quality information reporting system. Daily reports on operational quality data (e.g., percentage of defective units), weekly updates of trend graphs (posted throughout the division), and quarterly cost reports are the types of information required. g. To help direct the improvements in quality activities, kaizen costing is to be implemented. For example, for the year 20x1, a kaizen standard of 6 percent of the selling price per unit was set for rework costs, a 25 percent reduction from the current actual cost. To ensure that the quality improvements were directed and translated into concrete financial outcomes, Maria also began to implement a Balanced Scorecard for the division. By the end of 20x2, progress was being made. Sales had increased to 26,000,000, and the kaizen improvements were meeting or beating expectations. For example, rework costs had dropped to 1,500,000. At the end of 20x3, two years after the turnaround quality strategy was implemented, Maria received the following quality cost report: Maria also received an income statement for 20x3: Maria was pleased with the outcomes. Revenues had grown, and costs had been reduced by at least as much as she had projected for the two-year period. Growth next year should be even greater as she was beginning to observe a favorable effect from the higher-quality products. Also, further quality cost reductions should materialize as incoming inspections were showing much higher-quality purchased components. Required: 1. Identify the strategic objectives, classified by the Balanced Scorecard perspective. Next, suggest measures for each objective. 2. Using the results from Requirement 1, describe Marias strategy using a series of if-then statements. Next, prepare a strategy map. 3. Explain how you would evaluate the success of the quality-driven turnaround strategy. What additional information would you like to have for this evaluation? 4. Explain why Maria felt that the Balanced Scorecard would increase the likelihood that the turnaround strategy would actually produce good financial outcomes. 5. Advise Maria on how to encourage her employees to align their actions and behavior with the turnaround strategy.arrow_forwardBannister Company, an electronics firm, buys circuit boards and manually inserts various electronic devices into the printed circuit board. Bannister sells its products to original equipment manufacturers. Profits for the last two years have been less than expected. Mandy Confer, owner of Bannister, was convinced that her firm needed to adopt a revenue growth and cost reduction strategy to increase overall profits. After a careful review of her firms condition, Mandy realized that the main obstacle for increasing revenues and reducing costs was the high defect rate of her products (a 6 percent reject rate). She was certain that revenues would grow if the defect rate was reduced dramatically. Costs would also decline as there would be fewer rejects and less rework. By decreasing the defect rate, customer satisfaction would increase, causing, in turn, an increase in market share. Mandy also felt that the following actions were needed to help ensure the success of the revenue growth and cost reduction strategy: a. Improve the soldering capabilities by sending employees to an outside course. b. Redesign the insertion process to eliminate some of the common mistakes. c. Improve the procurement process by selecting suppliers that provide higher-quality circuit boards. Required: 1. State the revenue growth and cost reduction strategy using a series of cause-and-effect relationships expressed as if-then statements. 2. Illustrate the strategy using a strategy map. 3. Explain how the revenue growth strategy can be tested. In your explanation, discuss the role of lead and lag measures, targets, and double-loop feedback.arrow_forwardThe president of Poleski would like to know the effect that each of the following suggestions for improving performance would have on contribution margin per unit, sales needed to break even, and projected net income for next year. Each change should be considered independently. Reset the Data Section to its original values after each suggestion is analyzed. Fill in the table following the suggestions with the results of your analysis. a. The president suggests cutting the products price. Since the market is relatively sensitive to price, . . . a 10% cut in price ought to generate a 30% increase in sales (to 156,000 units). How can you lose? b. The sales manager feels that putting all sales personnel on straight commission would help. This would eliminate 77,000 in fixed sales salaries expense. Variable sales commissions would increase to 2.00 per unit. This move would also increase sales volume by 30%. c. Poleskis head of product engineering wants to redesign the package for the product. This will cut 1.00 per unit from direct materials and 0.50 per unit from direct labor, but will increase fixed factory overhead by 100,000 for additional depreciation on the new packaging machine. The package redesign would not affect sales volume. d. The firms consumer marketing manager suggests undertaking a new advertising campaign on Facebook. This would cost 30,000 more than is currently planned for advertising but would be expected to increase sales volume by 30%. e. The production superintendent suggests raising quality and raising price. This will increase direct materials by 1.00 per unit, direct labor by 0.50 per unit, and fixed factory overhead by 110,000. With improved quality, . . . raise the price to 18.50 and advertise the heck out of it. If you double your current planned advertising, Ill bet you can increase your sales volume by 30%.arrow_forward

- Carpetland salespersons average 8,000 per week in sales. Steve Contois, the firms vice president, proposes a compensation plan with new selling incentives. Steve hopes that the results of a trial selling period will enable him to conclude that the compensation plan increases the average sales per salesperson. a. Develop the appropriate null and alternative hypotheses. b. What is the Type I error in this situation? What are the consequences of making this error? c. What is the Type II error in this situation? What are the consequences of making this error?arrow_forwardNico Parts, Inc., produces electronic products with short life cycles (of less than two years). Development has to be rapid, and the profitability of the products is tied strongly to the ability to find designs that will keep production and logistics costs low. Recently, management has also decided that post-purchase costs are important in design decisions. Last month, a proposal for a new product was presented to management. The total market was projected at 200,000 units (for the two-year period). The proposed selling price was 130 per unit. At this price, market share was expected to be 25 percent. The manufacturing and logistics costs were estimated to be 120 per unit. Upon reviewing the projected figures, Brian Metcalf, president of Nico, called in his chief design engineer, Mark Williams, and his marketing manager, Cathy McCourt. The following conversation was recorded: BRIAN: Mark, as you know, we agreed that a profit of 15 per unit is needed for this new product. Also, as I look at the projected market share, 25 percent isnt acceptable. Total profits need to be increased. Cathy, what suggestions do you have? CATHY: Simple. Decrease the selling price to 125 and we expand our market share to 35 percent. To increase total profits, however, we need some cost reductions as well. BRIAN: Youre right. However, keep in mind that I do not want to earn a profit that is less than 15 per unit. MARK: Does that 15 per unit factor in preproduction costs? You know we have already spent 100,000 on developing this product. To lower costs will require more expenditure on development. BRIAN: Good point. No, the projected cost of 120 does not include the 100,000 we have already spent. I do want a design that will provide a 15-per-unit profit, including consideration of preproduction costs. CATHY: I might mention that post-purchase costs are important as well. The current design will impose about 10 per unit for using, maintaining, and disposing our product. Thats about the same as our competitors. If we can reduce that cost to about 5 per unit by designing a better product, we could probably capture about 50 percent of the market. I have just completed a marketing survey at Marks request and have found out that the current design has two features not valued by potential customers. These two features have a projected cost of 6 per unit. However, the price consumers are willing to pay for the product is the same with or without the features. Required: 1. Calculate the target cost associated with the initial 25 percent market share. Does the initial design meet this target? Now calculate the total life-cycle profit that the current (initial) design offers (including preproduction costs). 2. Assume that the two features that are apparently not valued by consumers will be eliminated. Also assume that the selling price is lowered to 125. a. Calculate the target cost for the 125 price and 35 percent market share. b. How much more cost reduction is needed? c. What are the total life-cycle profits now projected for the new product? d. Describe the three general approaches that Nico can take to reduce the projected cost to this new target. Of the three approaches, which is likely to produce the most reduction? 3. Suppose that the Engineering Department has two new designs: Design A and Design B. Both designs eliminate the two nonvalued features. Both designs also reduce production and logistics costs by an additional 8 per unit. Design A, however, leaves post-purchase costs at 10 per unit, while Design B reduces post-purchase costs to 4 per unit. Developing and testing Design A costs an additional 150,000, while Design B costs an additional 300,000. Assuming a price of 125, calculate the total life-cycle profits under each design. Which would you choose? Explain. What if the design you chose cost an additional 500,000 instead of 150,000 or 300,000? Would this have changed your decision? 4. Refer to Requirement 3. For every extra dollar spent on preproduction activities, how much benefit was generated? What does this say about the importance of knowing the linkages between preproduction activities and later activities?arrow_forwardPoleski Manufacturing, which maintains the same level of inventory at the end of each year, provided the following information about expenses anticipated for next year: The selling price of Poleskis single product is 16. In recent years, profits have fallen and Poleskis management is now considering a number of alternatives. Poleski wants to have a net income next year of 250,000, but expects to sell only 120,000 units unless some changes are made. The president of Poleski has asked you to calculate the companys projected net income (assuming 120,000 units are sold) and the sales needed to achieve the companys net income objective for next year. Also, compute Poleskis contribution margin per unit, contribution margin ratio, and break-even point for next year. The worksheet CVP has been provided to assist you. Note that the data from the problem have already been entered into the Data Section of the worksheet.arrow_forward

- Wayne Johnson, president of Banshee Company, recently returned from a conference on quality and productivity. At the conference, he was told that many American firms have quality costs totaling 20 to 30 percent of sales. He, however, was skeptical about this statistic. But even if the quality gurus were right, he was sure that his companys quality costs were much lowerprobably less than 5 percent. On the other hand, if he was wrong, he would be passing up an opportunity to improve profits significantly and simultaneously strengthen his competitive position. The possibility was at least worth exploring. He knew that his company produced most of the information needed for quality cost reportingbut there never was a need to bother with any formal quality data gathering and analysis. This conference, however, had convinced him that a firms profitability can increase significantly by improving qualityprovided the potential for improvement exists. Thus, before committing the company to a quality improvement program, Wayne requested a preliminary estimate of the total quality costs currently being incurred. He also indicated that the costs should be classified into four categories: prevention, appraisal, internal failure, or external failure. He has asked you to prepare a summary of quality costs and to compare the total costs to sales and profits. To assist you in this task, the following information has been prepared from the past year, 20x5: a. Sales revenue, 15,000,000; net income, 1,500,000. b. During the year, customers returned 90,000 units needing repair. Repair cost averages 1 per unit. c. Four inspectors are employed, each earning an annual salary of 60,000. These four inspectors are involved only with final inspection (product acceptance). d. Total scrap is 150,000 units. Of this total, 60 percent is quality related. The cost of scrap is about 5 per unit. e. Each year, approximately 450,000 units are rejected in final inspection. Of these units, 80 percent can be recovered through rework. The cost of rework is 0.75 per unit. f. A customer cancelled an order that would have increased profits by 150,000. The customers reason for cancellation was poor product performance. g. The company employs three full-time employees in its complaint department. Each earns 40,500 a year. h. The company gave sales allowances totaling 45,000 due to substandard products being sent to the customer. i. The company requires all new employees to take its three-hour quality training program. The estimated annual cost of the program is 30,000. Required: 1. Prepare a simple quality cost report classifying costs by category. 2. Compute the quality cost-to-sales ratio. Also, compare the total quality costs with total profits. Should Wayne be concerned with the level of quality costs? 3. Prepare a pie chart for the quality costs. Discuss the distribution of quality costs among the four categories. Are they properly distributed? Explain. 4. Discuss how the company can improve its overall quality and at the same time reduce total quality costs. 5. By how much will profits increase if quality costs are reduced to 2.5 percent of sales?arrow_forwardKimball Company has developed the following cost formulas: Materialusage:Ym=80X;r=0.95Laborusage(direct):Yl=20X;r=0.96Overheadactivity:Yo=350,000+100X;r=0.75Sellingactivity:Ys=50,000+10X;r=0.93 where X=Directlaborhours The company has a policy of producing on demand and keeps very little, if any, finished goods inventory (thus, units produced equals units sold). Each unit uses one direct labor hour for production. The president of Kimball Company has recently implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. This policy was implemented because Kimballs industry is in a recession and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that minimally cover their variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Required: 1. Compute the total unit variable cost. Suppose that Kimball has an opportunity to accept an order for 20,000 units at 220 per unit. Should Kimball accept the order? (The order would not displace any of Kimballs regular orders.) 2. Explain the significance of the coefficient of correlation measures for the cost formulas. Did these measures have a bearing on your answer in Requirement 1? Should they have a bearing? Why or why not? 3. Suppose that a multiple regression equation is developed for overhead costs: Y = 100,000 + 100X1 + 5,000X2 + 300X3, where X1 = direct labor hours, X2 = number of setups, and X3 = engineering hours. The coefficient of determination for the equation is 0.94. Assume that the order of 20,000 units requires 12 setups and 600 engineering hours. Given this new information, should the company accept the special order referred to in Requirement 1? Is there any other information about cost behavior that you would like to have? Explain.arrow_forwardVariety Artisans has a bottleneck in their production that occurs within the engraving department. Arjun Naipul, the COO, is considering hiring an extra worker, whose salary will be $45,000 per year, to solve the problem. With this extra worker, the company could produce and sell 3,500 more units per year. Currently, the selling price per unit is $18 and the cost per unit is $5.85. Using the information provided, calculate the annual financial impact of hiring the extra worker.arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub