FINANCIAL ACCT.FUND.(LOOSELEAF)

7th Edition

ISBN: 9781260482867

Author: Wild

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 5, Problem 6PSB

Analysis of inventory errors

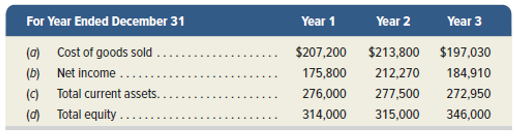

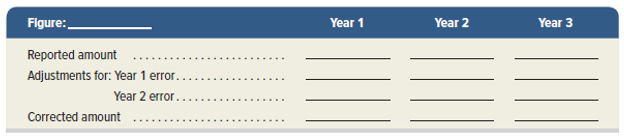

Hallam Company’s financial statements show the following. The company recently discovered that in making physical counts of inventory, it had made the following errors: Year 1 ending inventory is overstated by $18,000 and Year 2 ending inventory is understated by $26,000.

Required

- For each key financial statement figure (a), (b), (c), and (d) above - prepare a table similar to the following to show the adjustments necessary to correct the reported amounts. Check (1) Corrected net income: Year 1, $157,800; Year 2, $256,270; Year 3, $158,910

- What is the total error in combined net income for the three-year period resulting from the inventory errors? Explain.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

FINANCIAL ACCT.FUND.(LOOSELEAF)

Ch. 5 - Use the following information from Marvel Company...Ch. 5 - Use the following information from marvel company...Ch. 5 - Use the following information from Marvel Company...Ch. 5 - Use the following information from Marvel company...Ch. 5 - Periodic: A company reports the following...Ch. 5 - Prob. 6MCQCh. 5 - Prob. 1DQCh. 5 - Prob. 2DQCh. 5 - Prob. 3DQCh. 5 - Prob. 4DQ

Ch. 5 - Prob. 5DQCh. 5 - Prob. 6DQCh. 5 - Prob. 7DQCh. 5 - Prob. 8DQCh. 5 - Prob. 9DQCh. 5 - Prob. 10DQCh. 5 - Prob. 11DQCh. 5 - Prob. 12DQCh. 5 - Prob. 1QSCh. 5 - Prob. 2QSCh. 5 - Prob. 3QSCh. 5 - Prob. 4QSCh. 5 - Prob. 5QSCh. 5 - Prob. 6QSCh. 5 - Prob. 7QSCh. 5 - Prob. 8QSCh. 5 - Prob. 9QSCh. 5 - Prob. 10QSCh. 5 - Prob. 11QSCh. 5 - Prob. 12QSCh. 5 - Prob. 13QSCh. 5 - Prob. 14QSCh. 5 - Prob. 15QSCh. 5 - Prob. 16QSCh. 5 - Prob. 17QSCh. 5 - Prob. 18QSCh. 5 - Prob. 19QSCh. 5 - Prob. 20QSCh. 5 - Prob. 21QSCh. 5 - Prob. 22QSCh. 5 - Prob. 23QSCh. 5 - Prob. 1ECh. 5 - Prob. 2ECh. 5 - Prob. 3ECh. 5 - Prob. 4ECh. 5 - Prob. 5ECh. 5 - Prob. 6ECh. 5 - Prob. 7ECh. 5 - Prob. 8ECh. 5 - Prob. 9ECh. 5 - Prob. 10ECh. 5 - Prob. 11ECh. 5 - Prob. 12ECh. 5 - Prob. 13ECh. 5 - Prob. 14ECh. 5 - Prob. 15ECh. 5 - Prob. 16ECh. 5 - Prob. 17ECh. 5 - Prob. 18ECh. 5 - Prob. 19ECh. 5 - Perpetual: Alternative cost flows P1 Warnerwoods...Ch. 5 - Periodic: Alternative cost flows P3 Refer to the...Ch. 5 - Perpetual: Alternative cost flows P1 Montoure...Ch. 5 - Prob. 4PSACh. 5 - Prob. 5PSACh. 5 - Analysis of inventory errors A2 Navajo Company’s...Ch. 5 - Prob. 7PSACh. 5 - Periodic: Income comparisons and cost flows A1P3...Ch. 5 - Prob. 9PSACh. 5 - Prob. 10PSACh. 5 - Prob. 1PSBCh. 5 - Prob. 2PSBCh. 5 - Prob. 3PSBCh. 5 - Prob. 4PSBCh. 5 - Lower of cost or market P2 A physical inventory of...Ch. 5 - Analysis of inventory errors A2 Hallam Company’s...Ch. 5 - Prob. 7PSBCh. 5 - Periodic: Income comparisons and cost flows A1P3...Ch. 5 - Prob. 9PSBCh. 5 - Prob. 10PSBCh. 5 - Prob. 5SPCh. 5 - Prob. 1AACh. 5 - Prob. 2AACh. 5 - Prob. 3AACh. 5 - Prob. 1BTNCh. 5 - Prob. 2BTNCh. 5 - Prob. 3BTNCh. 5 - Prob. 4BTNCh. 5 - Prob. 5BTNCh. 5 - Visit four retail stores with another classmate....

Additional Business Textbook Solutions

Find more solutions based on key concepts

Bank loan; accrued interest LO132 On October 1, Eder Fabrication borrowed 60 million and issued a nine-month, ...

Intermediate Accounting

Ravenna Candles recently purchased candleholders for resale in its shops. Which of the following costs would be...

Financial Accounting (12th Edition) (What's New in Accounting)

Place the letter of the appropriate accounting cost in Column 2 in the blank next to each decision category in ...

Fundamentals of Cost Accounting

This year, Prewer Inc. received a 160,000 dividend on its investment consisting of 16 percent of the outstandin...

PRINCIPLES OF TAXATION F/BUS.+INVEST.

BE1-7 Indicate which statement you would examine to find each of the following items: income statement (IS), ba...

Financial Accounting: Tools for Business Decision Making, 8th Edition

What are assets limited as to use and how do they differ from restricted assets?

Accounting For Governmental & Nonprofit Entities

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- If a group of inventory items costing $3,200 had been double counted during the year-end inventory count, what impact would the error have on the following inventory calculations? Indicate the effect (and amount) as either (a) none, (b) understated $______, or (c) overstated $______. Table 10.2arrow_forwardErrors As controller of Lerner Company, which uses a periodic inventory system, you discover the following errors in the current year: 1. Merchandise with a cost of 17,500 was properly included in the final inventory, but the purchase was not recorded until the following year. 2. Merchandise purchases are in transit under terms of FOB shipping point. They have been excluded from the inventory, but the purchase was recorded in the current year on the receipt of the invoice of 4,300. 3. Goods out on consignment have been excluded from inventory. 4. Merchandise purchases under terms FOB shipping point have been omitted from the purchases account and the ending inventory. The purchases were recorded in the following year. 5. Goods held on consignment from Talbert Supply Co. were included in the inventory. Required: For each error, indicate the effect on the ending inventory and the net income for the current year and on the net income for the following year.arrow_forwardEffects of an Inventory Error The income statements for Graul Corporation for the 3 years ending in 2019 appear below. During 2019, Graul discovered that the 2017 ending inventory had been misstated due to the following two transactions being recorded incorrectly. a. A purchase return of inventory costing $42,000 was recorded twice. b. A credit purchase of inventory' made on December 20 for $28,500 was not recorded. The goods were shipped F.O.B. shipping point and were shipped on December 22, 2017. Required: 1. Was ending inventory for 2017 overstated or understated? By how much? 2. Prepare correct income statements for all 3 years. 3. CONCEPTUAL CONNECTION Did the error in 2017 affect cumulative net income for the 3-year period? Explain your response. 4. CONCEPTUAL CONNECTION Why was the 2019 net income unaffected?arrow_forward

- Lower of Cost or Market Garcia Company uses FIFO, and its inventory at the end of the year was recorded in the accounting records at $17,800. Due to technological changes in the market, Garcia would be able to replace its inventory for $16,500. Required: 1. Using the lower of cost or market method, what amount should Garcia report for inventory on its balance sheet at the end of the year? 2. Prepare the journal entry required to value the inventory at the lower of cost or market.arrow_forwardIf a group of inventory items costing $15,000 had been omitted from the year-end inventory count, what impact would the error have on the following inventory calculations? Indicate the effect (and amount) as either (a) none, (b) understated $______, or (c) overstated $______. Table 10.1arrow_forwardInventory Errors McLelland Inc. reported net income of $175,000 for 2019 and $210,000 for 2020. Early in 2020, McLelland discovers that the December 31, 2019 ending inventory was overstated by $20,000. For simplicity, ignore taxes. Required: 1. What is the correct net income for 2019? For 2020? 2. Assuming the error was not corrected, what is the effect on the balance sheet at December 31, 2019? At December 31, 2020?arrow_forward

- The following are independent errors made by a company that uses the periodic inventory system: a. Goods in transit, purchased on credit and shipped FOB destination, 10,000, were included in purchases but not in the physical count of ending inventory. b. Purchase of a machine for 2,000 was expensed. The machine has a 4-year life, no residual value, and straight-line depreciation is used. c. Wages payable of 2,000 were not accrued. d. Payment of next years rent, 4,000, was recorded as rent expense. e. Allowance for doubtful accounts of 5,000 was not recorded. The company normally uses the aging method. f. Equipment with a book value of 70,000 and a fair value of 100,000 was sold at the beginning of the year. A 2-year, non-interest-bearing note for 129,960 was received and recorded at its face value, and a gain of 59,960 was recognized. No interest revenue was recorded and 14% is a fair rate of interest. Required: 1. Next Level Indicate the effect of each of the preceding errors on the companys assets, liabilities, shareholders equity, and net income in the year in which the error occurs. State whether the error causes an overstatement (+), an understatement (), or no effect (NE). 2. Prepare the correcting journal entry or entries required at the beginning of the year for each of the preceding errors, assuming the company discovers the error in the year after it was made. Ignore income taxes.arrow_forwardAnalyzing Inventory The recent financial statements of McLelland Clothing Inc. include the following data: Required: 1. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the FIFO inventory costing method. Be sure to explain what each ratio means. 2. Calculate McLellands gross profit ratio (rounded to two decimal places), inventory turnover ratio (rounded to three decimal places), and the average days to sell inventory (assume a 365-day year and round to two decimal places) using the LIFO inventory costing method. Be sure to explain what each ratio means. 3. CONCEPTUAL CONNECTION Which ratios-the ones computed using FIFO or LIFO inventory values-provide the better indicator of how successful McLelland was at managing and controlling its inventory?arrow_forward( Appendix 6B) Inventory Costing Methods: Periodic System Harrington Company had the following data for inventory during a recent year: Assume that Harrington uses a periodic inventory accounting system. Required: 1. Using the FIFO, LIFO, and average cost methods, compute the ending inventory and cost of goods sold. ( Note: Use four decimal places for per-unit calculations and round all other numbers to the nearest dollar.) 2. CONCEPTUAL CONNECTION Which method will produce the most realistic amount for income? For inventory? 3. CONCEPTUAL CONNECTION Which method will produce the lowest amount paid for taxes?arrow_forward

- Assuming a companys year-end inventory were understated by $16,000, indicate the effect (overstated/understated/no effect) of the error on the following balance sheet and income statement accounts. A. Income Statement: Cost of Goods Sold B. Income Statement: Net Income C. Balance Sheet: Assets D. Balance Sheet: Liabilities E. Balance Sheet: Equityarrow_forwardEffects of an Error in Ending Inventory Waymire Company prepared the partial income statements presented below for 2019 and 2018. During 2020, Waymires accountant discovered that ending inventory for 2018 had been understated by $6,500. Required: 1. Prepare corrected income statements for 2019 and 2018. 2. Prepare a schedule showing each financial statement item affected by the error and the amount of the error for that item (ignore the effect of income taxes). Indicate whether each error is an overstatement (+) or an understatement (-).arrow_forward( Appendix 6B) Refer to the information for Morgan Inc. above. If Morgan uses a periodic inventory system, what is the cost of ending inventory under LIFO at April 30? a. $32,800 b. $38,400 c. $63,600 d. $69,200arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...

Accounting

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

Chapter 6 Merchandise Inventory; Author: Vicki Stewart;https://www.youtube.com/watch?v=DnrcQLD2yKU;License: Standard YouTube License, CC-BY

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License