Videos

INTEREST RATE DETERMINATION AND YIELD CURVES

a. What effect would each of the following events likely have on the level of nominal interest rates?

- 1. Households dramatically increase their savings rate.

- 2. Corporations increase their demand for funds following an increase in investment opportunities.

- 3. The government runs a larger-than-expected budget deficit.

- 4. There is an increase in expected inflation.

b. Suppose you are considering two possible investment opportunities: a 12-year Treasury bond and a 7-year, A-rated corporate bond. The current real risk-free rate is 4%; and inflation is expected to be 2% for the next 2 years, 3% for the following 4 years, and 4% thereafter. The maturity risk premium is estimated by this formula: MRP = 0 02(t − 1)%. The liquidity premium (LP) for the corporate bond is estimated to be 0.3%. You may determine the default risk premium (DRP), given the company’s bond rating, from the table below. Remember to subtract the bond’s LP from the corporate spread given in the table to arrive at the bond’s DRP. What yield would you predict for each of these two investments?

| Rate | Corporate Bond Yield Spread = DRP + LP | ||

| U.S. Treasury | 0.83% | ---- | |

| AAA corporate | 0.93 | 0.10% | |

| AA corporate | 1.29 | 0.46 | |

| A corporate | 1.67 | 0.84 | |

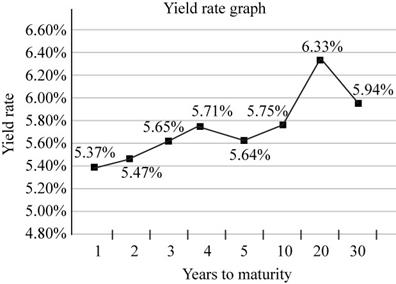

c. Given the following Treasury bond yield information, construct a graph of the yield curve.

| Maturity | Yield |

| 1 year | 5.37% |

| 2 years | 5.47 |

| 3 years | 5.65 |

| 4 years | 5.71 |

| 5 years | 5.64 |

| 10 years | 5.75 |

| 20 years | 6.33 |

| 30 years | 5.94 |

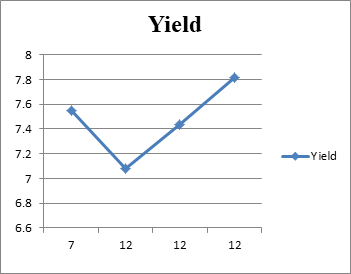

d. Based on the information about the corporate bond provided in part b, calculate yields and then construct a new yield curve graph that shows both the Treasury and the corporate bonds.

e. Which part of the yield curve (the left side or right side) is likely to be most volatile over time?

f. Using the Treasury yield information in part c, calculate the following rates using geometric averages:

- 1. The 1-year rate 1 year from now

- 2. The 5-year rate 5 years from now

- 3. The 10-year rate 10 years from now

- 4. The 10-year rate 20 years from now

a. (1)

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

The increment in the rates of savings account of households leads to increase in nominal interest rate as the households get good returns from treasury bills or bonds the nominal rate would increase.

Explanation of Solution

- The increase ininterest rate of savings account of the households resultsto increase the demand for the funds.

- To offer the good returns to households lead to increase in demand forinvestment in a savings account and the returns of Treasury securities where the household invest their money would also increase.

Hence, if the households would increase the interest rates to get more investment it will lead to increase in nominal rate.

(2)

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

The corporations increase the rates to increase the demand of their funds which leads to increase in nominal rate.

Explanation of Solution

- The corporations require fund for their business and to increase the demand for the product.

- Increase in demand of the product leads to increase in nominal interest rate.

Hence, the increase in nominal rate would result in the increase in demand of the funds of corporations.

3.

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

Solution:

The larger-than-expected budget leads to increase in nominal interest rate.

Explanation of Solution

- The larger-than-expected budget refers the negative condition of the budget of government.

- To make the balance of budget, the governmentwould issue the investment securities and increase the interest on that and nominal rates would increase.

Hence, the larger deficit of the budget leads to increase in nominal rate as the government issues the securities to raise fund.

4.

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

Increase in interest rate leads to increase rate as it is included in nominal rate.

Explanation of Solution

- Inflation refers to the condition when the price of the goods and commodity increase and the purchasing power parity would also increase.

- The interest rates of the investments avenues include the inflation rate in it.

Hence, the increase in inflation positively leads to increase in nominal interest rate.

b.

To compute: The expected yield for 12-year Treasury bond and 7-year A-rated corporate bond.

Yield:

Yield is the percentage of the securities at which the return is provided by the company to its investors. Yield can be there in the form of dividend and interest.

Explanation of Solution

Compute the yield for the 12-years treasury bonds.

The risk-free rate is 4%. (Given)

The inflation premium is 3.33%. (Calculated in working note)

The maturity risk premium is 0.22%. (Calculated in working note)

The formula to calculate the yield on treasury bonds,

Where,

-

-

-

- MRP is maturity risk premium.

Substitute 4% for

The yield on 12-year treasury bonds is 7.55%.

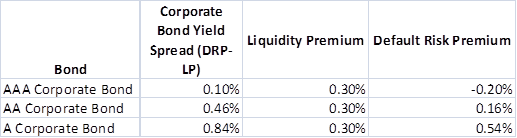

Compute the default risk premium on a corporate bond,

Table (1)

Compute the yield for AAA Corporate bond.

The risk-free rate is 4%. (Given)

The liquidity premium and default risk premium is 0.10%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is the liquidity premium.

Substitute 4% for

The yield on 7-year AAA corporate bond is 7.08%.

Compute the yield for AA Corporate bond.

The risk-free rate is 4%. (Given)

Default risk premium and liquidity premium is 0.46%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is liquidity premium.

Substitute 4% for

The yield on 7-year AA corporate bond is 7.44%.

Compute the yield for A Corporate bond.

The risk-free rate is 4%. (Given)

Default risk premium and liquidity premium is 0.84%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is liquidity premium.

Substitute 4% for

The yield on 7-year A corporate bond is 7.82%.

Working note:

Treasury bond calculations:

Computation of inflation premium on 12-years treasury bonds,

Computation of the maturity risk premium,

7-years bond calculations:

Computation of the inflation premium,

Computation of the maturity risk premium,

Hence,the default risk premiums of AAA corporate bond, AA corporate bond, and A corporate bond, are (0.20%), 0.16% and 0.54% respectively. The expected yield of 12-yearTreasury bond is 7.55%, AAA corporate bond is 7.08%, AA corporate bond is 7.44% and A corporate bond is 7.82%.

c.

To prepare: A yield curve chart for given information.

Yield Curve:

The graphical representation of the expected return, provided by the company to its investors during the years is known as the yield curve.

Answer to Problem 20SP

The yield curve chart

Fig 1

Explanation of Solution

- The x-axis shows the number of years.

- The y-axis shows years to maturity.

- The graph shows the expected yield with their respective years.

- The yield curve is sloping upwards and is increasing until the 20th year and then it slopes downward.

The yield curve chart for the given information is as mentioned above.

d.

To draw: The yield curve chart.

Answer to Problem 20SP

Statement to show the relative yields, calculated in part b.

| Bond | Expected Yield |

| 12-year Treasury Bond | 7.55% |

| 7-year AAA Corporate Bond | 7.08% |

| 7-year AA Corporate Bond | 7.44% |

| 7-year A Corporate Bond | 7.82% |

Table (2)

The yield to maturity graph:

Fig 2

Explanation of Solution

- The x-axis shows the number of years.

- The y-axis shows years to maturity.

- The graph shows the expected yield with their respective years.

- The yield curve shows a downward slope up to 12 years.

- The curve then shows an upward slope and continues to increase.

Thus, the yield curve chart is shown as above.

e.

To identify: The side of a yield curve which would be more volatile.

Answer to Problem 20SP

Solution:

The right side of the yield curve would be more volatile as an increase in the maturity increases the yield of the bond.

Explanation of Solution

- The yield curve represents the yield of relative bonds with their respective years.

- The yield increase towards the right as the year of maturity increases and more volatile from the right side.

Hence, the right side of the yieldcurve is more volatile than the left side.

f. (1)

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 2 years is 5.47%.

The yield for 1 year is 5.37%.

The formula to compute the rate,

Substitute 0.0547 for yield for year 2, 0.0537 for yield for year 1, 1 for a number of years and 1 for years from now.

The rate is 5.57%.

Hence, the rate of 1-year, 1 year from now is 5.57%.

2.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 10 years is 5.75%.

The yield for 5years is 5.64%.

The formula to compute the rate,

Substitute 0.0575 for yield for year 10, 0.0564 for yield for year 5, 5 for a number of years and 5 for years from now.

Take root to bothsides.

The rate is 5.86%.

Hence, the rate of 5-year, 5 years from now is 5.86%.

3.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 20 years is 6.33%.

The yield for 10years is 5.75%.

The formula to compute the rate,

Substitute 0.0633 for yield for year 20, 0.0575 for yield for year 10, 10 for a number of years and 10 for years from now.

Take root to bothsides.

The rate is 6.91%.

Hence, the rate of 10-year, 10 years from now is 6.91%.

4.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 30 years is 5.94%.

The yield for 20 years is 6.33%.

The formula to compute the rate,

Substitute 0.0633 for yield for year 20, 0.0594 for yield for year 30, 10 for a number of years and 20 for years from now.

Take root to bothsides.

The rate is 5.61%.

Hence, the rate of 10-year, 20 years from now is 5.61%.

Want to see more full solutions like this?

Chapter 6 Solutions

Fundamentals of Financial Management (MindTap Course List)

- YIELD CURVES Assume that yields on U.S. Treasury securities were as follows: Term Rate 6 months 4.69% 1 year 5.492 years 5.663 years 5.71 4 years 5.89 5 years 6.05 10 years 6.12 20 years 6.64 30 years 6.76 Plot a yield curve based on these data. What type of yield curve is shown? Whatinformationdoesthisgraphtellyou? Based on this yield curve, if you needed to borrow money for longer than 1 year, would it make sense for you to borrow short term and renew the loan or borrow long term? Explain.arrow_forwardPandemic has caused higher unemployment rate and lower growth in GDP. Federal Reserve wants to buy more 1-year and 10-year Treasury securities and sell 5-year Treasury securities to stimulate the economy. What would be shape of Treasury yield curve as a result of this move by Fed? Explain this yield curve using appropriate theory of term structure.arrow_forwardThe yield on two-year government bonds is 4.5%, and one-year government bonds provide a yield of 3%. In addition, the real risk-free interest rate (r*) is 1%, and the maturity risk premium is 0. 1) According to the theory of expectation, what is the rate of return on annual government bonds from now to later? Calculate the rate of return using the geometric mean. 2) What are the expected inflation rates for the first and second years respectively?arrow_forward

- Suppose two firms want to borrow money from a bank for a period of 10 years. Firm A has excellent credit and can borrow at the prime rate, whereas Firm B's credit standing is prime rate plus 2 percent. The current prime rate is 5.75 percent, the 30-year Treasury bond yield is 4.35 percent, the three-month Treasury bill yield is 3.54 percent, and the 10-year Treasury note yield is 4.24 percent. What are the appropriate loan rates for both the firms? 6.45% for Firm A, 7.75% for Firm B 6.45% for Firm A, 8.45% for Firm B 5.75% for Firm A, 8.45% for Firm B None of the abovearrow_forwardAssume that yields on U.S. Treasury securities were as follows:Term Rate6 months 4.69%1 year 5.492 years 5.663 years 5.714 years 5.895 years 6.0510 years 6.1220 years 6.6430 years 6.76 a. Plot a yield curve based on these data.b. What type of yield curve is shown?c. What information does this graph tell you?d. Based on this yield curve, if you needed to borrow money for longer than 1 year,would it make sense for you to borrow short term and renew the loan or borrow longterm? Explain.arrow_forwardLiquidity Premium Hypothesis Based on economists' forecasts and analysis, one-year Treasury bill rates and liquidity premiums for the next four years are expected to be as follows: R1 = 6.05% E(r2) = 7.15% L2 = .85% E(r3) = 7.35% L3 = .88% E(r4) = 7.55% L4 = .90% Using the liquidity premium hypothesis, what is the current rate on a four-year Treasury security?arrow_forward

- 1. Briefly explain the following: a. You want to sell your bond that has a par value of ₱100,000 plus a 5 percent annual coupon rate thatwill mature after one year. The prevailing interest rate is 8%. Will you be able to sell your bond for ₱100,000 or higher? Briefly explain your answer.b. Is it possible for a country to have a twin deficit (a budget deficit and trade deficit) at the same time? How will this affect the economy? Briefly explain the benefits and dangers of a twin deficit.c. Which is better for the receiving country, FDI or FPI? Briefly explain your answer.arrow_forwardHyperinflation is indicated by all of the following, except: a. The general population prefers to keep its wealthy in nonmonetary assets. b. Interest rates, wages and prices are linked to a price index. c. The cumulative inflation rate over three years is approaching or exceeds 100%. d. All of the choices indicate hyperinflation.arrow_forwardYou are a fixed income investor who is expecting an upcoming recession (inverted yield curve). What is the best strategy to maximize your fixed income? A Keep money in existing fixed income assets B Move money to the long term because of higher interest rates C Sell off bonds with longer maturities and buy shorter maturity bonds D Purchase only 10 year government bonds to avoid default risk in a recessionarrow_forward

- Question Consider the following balance sheet positions for a financial institution:• Rate-sensitive assets = $120 million; Rate-sensitive liabilities = $180 million.• Rate-sensitive assets = $230 million; Rate-sensitive liabilities = $200 million.a) Calculate the repricing gap and the impact on net interest income of a 2 percent increase in interest rates for each position. b) Calculate the repricing gap and the impact on net interest income of a 2 percent decrease in interest rates for each position.c) Explain the type of risk this FI is exposed to in each position.arrow_forwardQuestion Consider the following balance sheet positions for a financial institution:• Rate-sensitive assets = $120 million; Rate-sensitive liabilities = $180 million.• Rate-sensitive assets = $230 million; Rate-sensitive liabilities = $200 million.a) Calculate the repricing gap and the impact on net interest income of a 2 percent increase in interest rates for each position. b) Calculate the repricing gap and the impact on net interest income of a 2 percent decrease in interest rates for each position.c) Explain the type of risk this FI is exposed to in each position. Kindly explain in detailarrow_forward

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT