Concept explainers

Videos

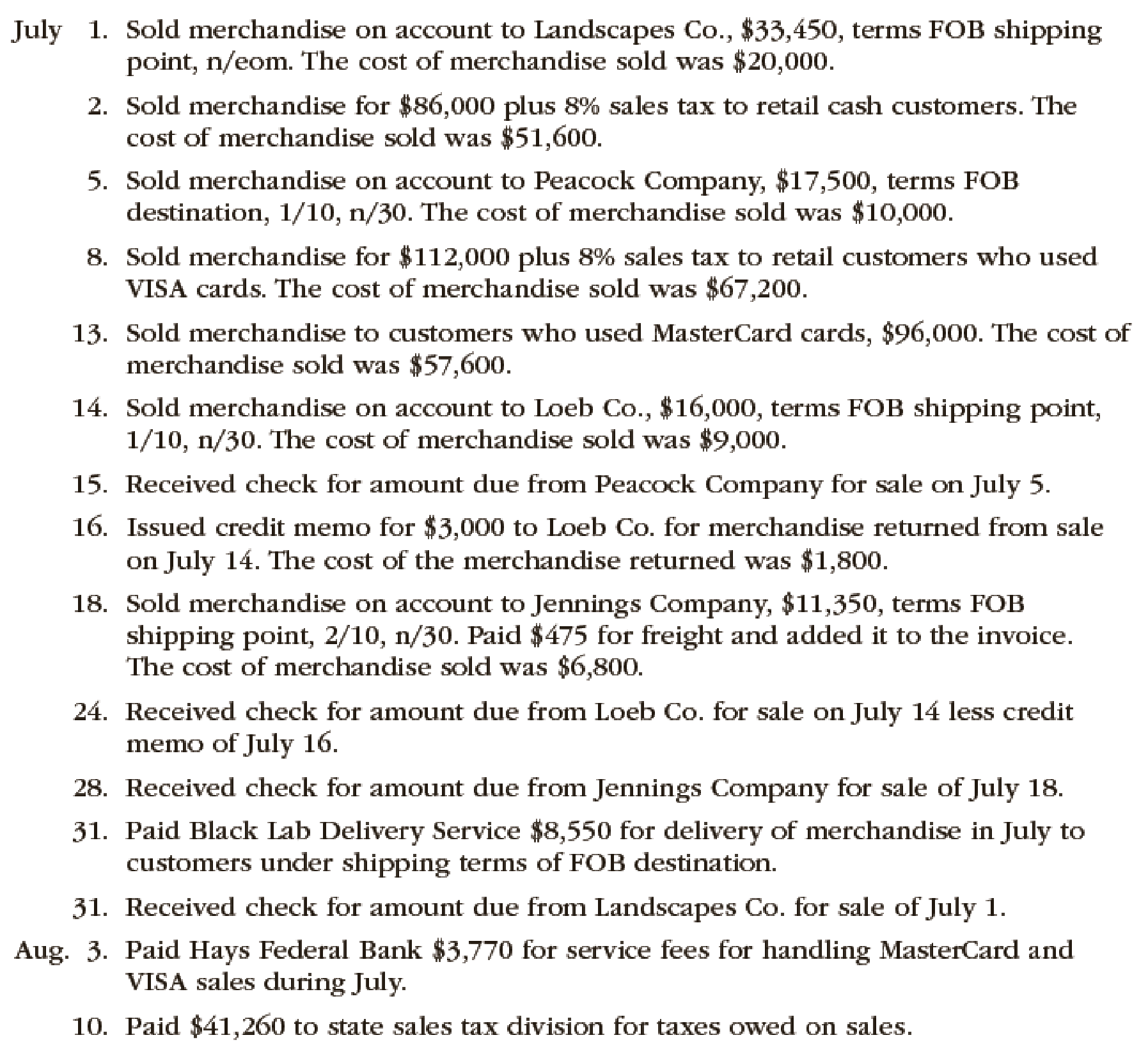

The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to wholesalers and occasionally to retail customers:

Instructions

Record the sale transactions of the company.

Explanation of Solution

Sales is an activity of selling the merchandise inventory of a business.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Accounts receivable | 33,450 | |

| Sales Revenue | 33,450 | ||

| (To record the sale of inventory on account) |

Table (1)

- Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

- Sales revenue is revenue and it increases the value of equity by $33,450. Therefore, credit sales revenue with $33,450.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Cost of Merchandise Sold | 20,000 | |

| Merchandise Inventory | 20,000 | ||

| (To record the cost of goods sold) |

Table (2)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $20,000. Therefore, debit cost of merchandise sold account with $20,000.

- Merchandise Inventory is an asset and it is decreased by $20,000. Therefore, credit inventory account with $20,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cash | 92,880 (2) | |

| Sales Revenue | 86,000 | ||

| Sales Tax Payable | 6,880 (1) | ||

| (To record the sale of inventory for cash) |

Table (3)

- Cash is an asset and it is increased by $92,880. Therefore, debit cash account with $92,880.

- Sales revenue is revenue and it increases the value of equity by $86,000. Therefore, credit sales revenue with $86,000.

- Sales tax payable is a liability and it is increased by $6,880. Therefore, credit sales tax payable account with $6,880.

Working Note (1):

Calculate the amount of sales tax payable.

Sales revenue = $86,000

Sales tax percentage = 8%

Working Note (2):

Calculate the amount of cash received.

Sales revenue = $86,000

Sales tax payable = $6,880 (1)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cost of Merchandise Sold | 51,600 | |

| Merchandise Inventory | 51,600 | ||

| (To record the cost of goods sold) |

Table (4)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $51,600. Therefore, debit cost of merchandise sold account with $51,600.

- Merchandise Inventory is an asset and it is decreased by $51,600. Therefore, credit inventory account with $51,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Accounts receivable | 17,325 (3) | |

| Sales Revenue | 17,325 | ||

| (To record the sale of inventory on account) |

Table (5)

- Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

- Sales revenue is revenue and it increases the value of equity by $17,325. Therefore, credit sales revenue with $17,325.

Working Note (3):

Calculate the amount of accounts receivable.

Sales = $17,500

Discount percentage = 1%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Cost of Merchandise Sold | 10,000 | |

| Merchandise Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (6)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of merchandise sold account with $10,000.

- Merchandise Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cash | 120,960 (5) | |

| Sales Revenue | 112,000 | ||

| Sales Tax Payable | 8,960 (4) | ||

| (To record the sale of inventory for cash) |

Table (7)

- Cash is an asset and it is increased by $120,960. Therefore, debit cash account with $120,960.

- Sales revenue is revenue and it increases the value of equity by $112,000. Therefore, credit sales revenue with $112,000.

- Sales tax payable is a liability and it is increased by $8,960. Therefore, credit sales tax payable account with $8,960.

Working Note (4):

Calculate the amount of sales tax payable.

Sales revenue = $112,000

Sales tax percentage = 8%

Working Note (5):

Calculate the amount of cash received.

Sales revenue = $112,000

Sales tax payable = $8,960 (4)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cost of Merchandise Sold | 67,200 | |

| Merchandise Inventory | 67,200 | ||

| (To record the cost of goods sold) |

Table (8)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $67,200. Therefore, debit cost of merchandise sold account with $67,200.

- Merchandise Inventory is an asset and it is decreased by $67,200. Therefore, credit inventory account with $67,200.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cash | 96,000 | |

| Sales Revenue | 96,000 | ||

| (To record the sale of inventory for cash) |

Table (9)

- Cash is an asset and it is increased by $96,000. Therefore, debit cash account with $96,000.

- Sales revenue is revenue and it increases the value of equity by $96,000. Therefore, credit sales revenue with $96,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cost of Merchandise Sold | 57,600 | |

| Merchandise Inventory | 57,600 | ||

| (To record the cost of goods sold) |

Table (10)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $57,600. Therefore, debit cost of merchandise sold account with $57,600.

- Merchandise Inventory is an asset and it is decreased by $57,600. Therefore, credit inventory account with $57,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Accounts receivable | 15,840 (6) | |

| Sales Revenue | 15,840 | ||

| (To record the sale of inventory on account) |

Table (11)

- Accounts Receivable is an asset and it is increased by $15,840. Therefore, debit accounts receivable with $15,840.

- Sales revenue is revenue and it increases the value of equity by $15,840. Therefore, credit sales revenue with $15,840.

Working Note (6):

Calculate the amount of accounts receivable.

Sales = $16,000

Discount percentage = 1%

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Cost of Merchandise Sold | 9,000 | |

| Merchandise Inventory | 9,000 | ||

| (To record the cost of goods sold) |

Table (12)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $9,000. Therefore, debit cost of merchandise sold account with $9,000.

- Merchandise Inventory is an asset and it is decreased by $9,000. Therefore, credit inventory account with $9,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 15 | Cash | 17,325 | |

| Accounts Receivable | 17,325 | ||

| (To record the receipt of cash against accounts receivables) |

Table (13)

- Cash is an asset and it is increased by $17,325. Therefore, debit cash account with $17,325.

- Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 16 | Customer Refunds Payable | 2,970 (7) | ||

| Accounts Receivable | 2,970 | |||

| (To record sales returns) |

Table (14)

- Customer refunds payable is a liability account and it is decreased by $2,970. Therefore, debit customer refunds payable account with $2,970.

- Accounts Receivable is an asset and it is decreased by $2,970. Therefore, credit account receivable with $2,970.

Working Note (7):

Calculate the amount of refund owed to the customer.

Sales return = $3,000

Discount percentage = 1%

Record the journal entry for the return of the merchandise.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 16 | Merchandise Inventory | 1,800 | |

| Estimated Returns Inventory | 1,800 | ||

| (To record the return of the merchandise) |

Table (15)

- Merchandise Inventory is an asset and it is increased by $1,800. Therefore, debit inventory account with $1,800.

- Estimated retunrs inventory is an expense account and it increases the value of equity by $1,800. Therefore, credit estimated returns inventory account with $1,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Accounts receivable | 11,123 (8) | |

| Sales Revenue | 11,123 | ||

| (To record the sale of inventory on account) |

Table (16)

- Accounts Receivable is an asset and it is increased by $11,123. Therefore, debit accounts receivable with $11,123.

- Sales revenue is revenue and it increases the value of equity by $11,123. Therefore, credit sales revenue with $11,123.

Working Note (8):

Calculate the amount of accounts receivable.

Sales = $11,350

Discount percentage = 2%

- Accounts Receivable is an asset and it is increased by $475. Therefore, debit accounts receivable with $475.

- Cash is an asset and it is decreased by $475. Therefore, credit cash account with $475.

Record the journal entry for freight charges paid.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 18 | Accounts Receivable | 475 | ||

| Cash | 475 | |||

| (To record freight charges paid) |

Table (17)

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Cost of Merchandise Sold | 6,800 | |

| Merchandise Inventory | 6,800 | ||

| (To record the cost of goods sold) |

Table (18)

- Cost of merchandise sold is an expense account and it decreases the value of equity by $6,800. Therefore, debit cost of merchandise sold account with $6,800.

- Merchandise Inventory is an asset and it is decreased by $6,800. Therefore, credit inventory account with $6,800.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 24 | Cash | 12,870 (9) | |

| Accounts Receivable | 12,870 | ||

| (To record the receipt of cash against accounts receivables) |

Table (19)

- Cash is an asset and it is increased by $12,870. Therefore, debit cash account with $12,870.

- Accounts Receivable is an asset and it is increased by $12,870. Therefore, debit accounts receivable with $12,870.

Working Note (9):

Calculate the amount of cash received.

Net accounts receivable = $15,840

Customer refunds payable = $2,970

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 28 | Cash | 11,598 (10) | |

| Accounts Receivable | 11,598 | ||

| (To record the receipt of cash against accounts receivables) |

Table (20)

- Cash is an asset and it is increased by $11,598. Therefore, debit cash account with $11,598.

- Accounts Receivable is an asset and it is increased by $11,598. Therefore, debit accounts receivable with $11,598.

Working Note (10):

Calculate the amount of cash received.

Net accounts receivable = $11,123

Freight charges = $475

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Delivery expense | 8,550 | |

| Cash | 8,550 | ||

| (To record the payment of delivery expenses) |

Table (21)

- Delivery expense is an expense account and it decreases the value of equity by $8,550. Therefore, debit delivery expense account with $8,550.

- Cash is an asset and it is decreased by $8,550. Therefore, credit cash account with $8,550.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 31 | Cash | 33,450 | |

| Accounts Receivable | 33,450 | ||

| (To record the receipt of cash against accounts receivables) |

Table (22)

- Cash is an asset and it is increased by $33,450. Therefore, debit cash account with $33,450.

- Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 3 | Credit card expense | 3,770 | |

| Cash | 3,770 | ||

| (To record the payment of credit card expenses) |

Table (23)

- Credit card expense is an expense account and it decreases the value of equity by $3,770. Therefore, debit credit card expense account with $3,770.

- Cash is an asset and it is decreased by $3,770. Therefore, credit cash account with $3,770.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 10 | Sales tax payable | 41,260 | |

| Cash | 41,260 | ||

| (To record the payment of credit card expenses) |

Table (24)

- Sales tax payable is a liability account and it is decreased by $41,260. Therefore, debit customer refunds payable account with $41,260.

- Cash is an asset and it is decreased by $41,260. Therefore, credit cash account with $41,260.

Want to see more full solutions like this?

Chapter 6 Solutions

Financial Accounting

- The following selected transactions were completed by Amsterdam Supply Co., which sells office supplies primarily to wholesalers and occasionally to retail customers: Instructions Journalize the entries to record the transactions of Amsterdam Supply Co.arrow_forwardLeanders Landscaping Service maintains the following chart of accounts: The following transactions were completed by Leander: Required 1. Journalize the transactions in the general journal. Prepare a brief explanation for each entry. 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. 3. Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) 4. Prepare a trial balance dated April 30, 20. If you are using CLGL, use the year 2020 when recording transactions and preparing reports.arrow_forwardThe following payments and receipts are related to land, land improvements, and buildings acquired for use in a wholesale ceramic business. The receipts are identified by an asterisk. Instructions 1. Assign each payment and receipt to Land (unlimited life), Land Improvements (limited life), Building, or Other Accounts. Indicate receipts by an asterisk. Identify each item by letter and list the amounts in columnar form, as follows: 2. Determine the amount debited to Land, Land Improvements, and Building. 3. The costs assigned to the land, which is used as a plant site, will not be depreciated, while the costs assigned to land improvements will be depreciated. Explain this seemingly contradictory application of the concept of depreciation. 4. What would be the effect on the current years income statement and balance sheet if the cost of filling and grading land of 12,000 [payment (i)] was incorrectly classified as Land Improvements rather than Land? Assume that Land Improvements are depreciated over a 20-year life using the double-declining-balance method.arrow_forward

- Plumb Line Surveyors provides survey work for construction projects. The office staff use office supplies, while surveying crews use field supplies. Purchases on account completed by Plumb Line Surveyors during May are as follows: Instructions 1. Insert the following balances in the general ledger as of May 1: 2. Insert the following balances in the accounts payable subsidiary ledger as of May 1: 3. Journalize the transactions for May, using a purchases journal (p. 30) similar to the one illustrated in this chapter. Prepare the purchases journal with columns for Accounts Payable, Field Supplies, Office Supplies, and Other Accounts. Post to the creditor accounts in the accounts payable subsidiary ledger immediately after each entry. 4. Post the purchases journal to the accounts in the general ledger. 5. a. What is the sum of the creditor balances in the subsidiary ledger at May 31? b. What is the balance of the accounts payable controlling account at May 31? 6. What type of e-commerce application would be used to plan and coordinate transactions with suppliers?arrow_forwardThe following items are recorded in the general journal, except Select one: A. Purchase of non-current assets on credit B. Withdrawal of goods by the owner for personal consumption C. Opening entries, adjusting entries and closing entries D. Purchase of goods on credit from supplierarrow_forwardCollins Landscape Company purchased various landscaping supplies on account to be used for landscape designs for its customers. How will this business transaction affect the accounting equation?arrow_forward

- Laras Landscaping Service has the following chart of accounts: The following transactions were completed by Laras Landscaping Service: Required 1. Journalize the transactions in the general journal. Provide a brief explanation for each entry. 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. (Skip this step if you are using CLGL.) 3. Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) 4. Prepare a trial balance dated March 31, 20. If you are using CLGL, use the year 2020 when recording transaction! and preparing reports.arrow_forwardReview the following transactions, and prepare any necessary journal entries for Juniper Landscaping Services. A. On November 5, Juniper receives advance cash payment from a customer for landscaping services in the amount of $3,500. Juniper had yet to provide landscaping services as of November 5. B. On December 11, Juniper provides all of the landscaping services to the customer from November 5. C. On December 14, Juniper receives advance payment from another customer for landscaping services in the amount of $4,400. Juniper has yet to provide landscaping services as of December 14. D. On January 19 of the following year, Juniper provides and recognizes 80% of landscaping services to the customer from December 14.arrow_forwardFrom the following list, identify which items are considered original sources: prepaid insurance bank statement sales ticket general journal trial balance balance sheet telephone bill invoice from supplier company sales account income statementarrow_forward

- From the following list, identify those that are likely to serve as source documents. Trial balanceunanswered Telephone bill Sales receiptunanswered Income statement Invoice from supplier Bank statementarrow_forwardPurchased $4,200 worth of cleaning supplies on account from Eastern Dry Cleaning Suppliers Ltd. What would be the correct entry into the General Journal?arrow_forwardSelected accounts from Han Corporations trial balance are as follows. Prepare the detailed schedule showing the Property, Plant, and Equipment.arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College