Concept explainers

Videos

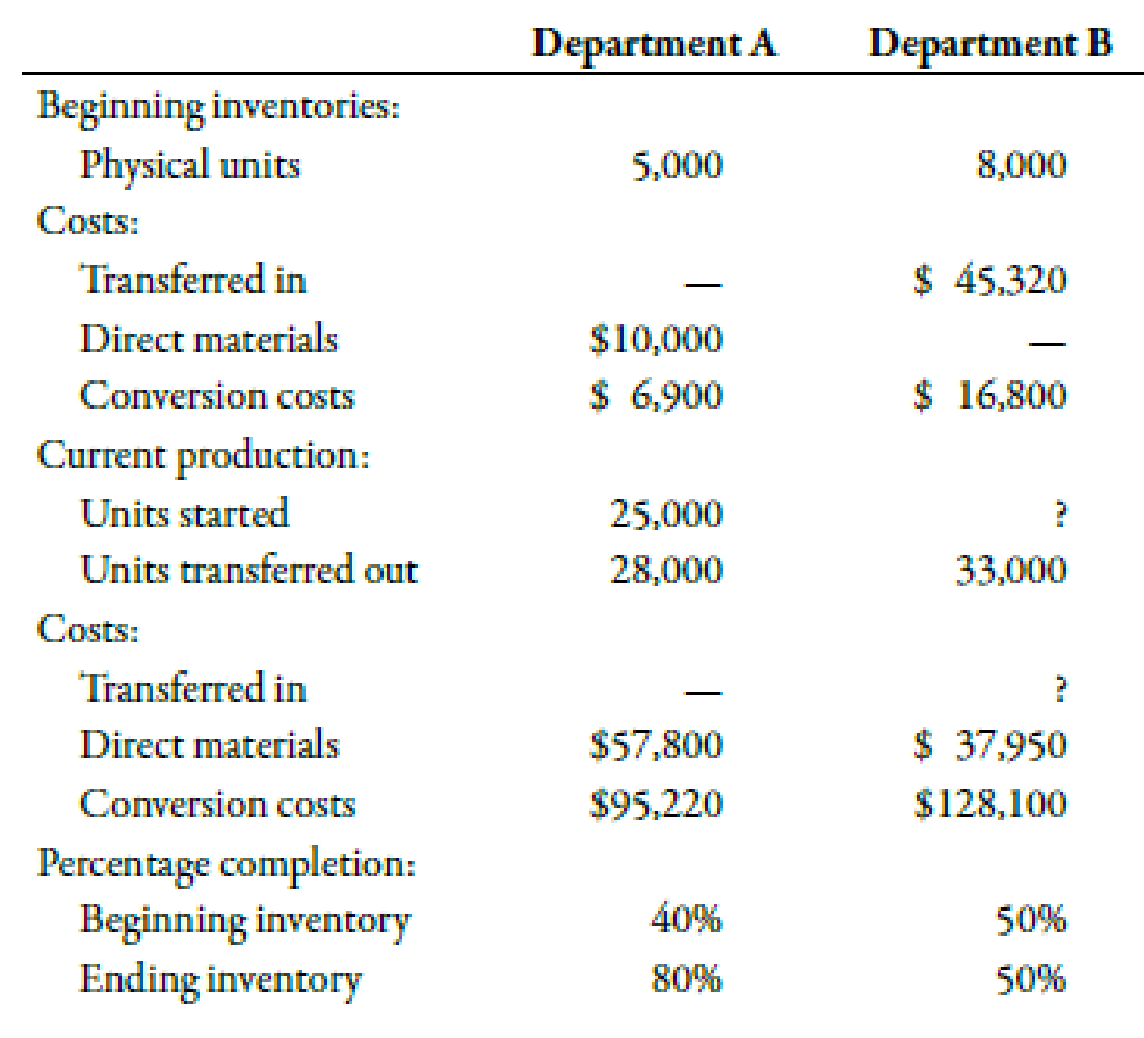

Seacrest Company uses a process-costing system. The company manufactures a product that is processed in two departments: A and B. As work is completed, it is transferred out. All inputs are added uniformly in Department A. The following summarizes the production activity and costs for November:

Required:

- 1. Using the weighted average method, prepare the following for Department A: (a) a physical flow schedule, (b) an equivalent unit calculation, (c) calculation of unit costs (Note: Round to four decimal places.), (d) cost of EWIP and cost of goods transferred out, and (e) a cost reconciliation.

- 2. CONCEPTUAL CONNECTION Prepare

journal entries that show the flow ofmanufacturing costs for Department A. Use a conversion cost control account for conversion costs. Many firms are now combining direct labor and overhead costs into one category. They are not tracking direct labor separately. Offer some reasons for this practice.

1.

a.

Make a physical flow schedule for department A.

Explanation of Solution

Physical Flow Schedule:

The schedule which is made with the objective to determine the production of physical units is known as physical flow schedule. It considers all units in process which can be related to any completion stage.

Prepare physical flow schedule of Company J:

| Physical Flow Schedule | |

| Units to account for: | Units |

| Units in BWIP | 5,000 |

| Add: Units started | 25,000 |

| Total units account for | 30,000 |

| Units accounted for: | |

| Units started and completed that are transferred. | 28,000 |

|

Add: Units in EWIP | 2,000 |

| Total units accounted for | 30,000 |

Table (1)

Therefore, the units accounted for and units to account for are 30,000 units.

b.

Compute equivalent unit of production with help of equivalent unit schedule of Company J.

Answer to Problem 65P

The equivalent units of production are 29,600units.

Explanation of Solution

Prepare equivalent unit schedule of Department A:

| Particulars | Units |

| Units completed | 28,000 |

| Add: Units in EWIP | 1,600 |

| Total equivalent unit | 29,600 |

Table (2)

Therefore, equivalent units of production are 29,600 units.

c.

Compute unit cost of Department A.

Answer to Problem 65P

The unit cost for Department A is $5.7405.

Explanation of Solution

Use the following formula to calculate unit cost for Department A:

Therefore, the unit cost is $5.7405

d.

Compute total cost of goods transferred out and cost of EWIP.

Answer to Problem 65P

The total cost of goods transferred out and cost of EWIP are $160,734 and $9,185 respectively.

Explanation of Solution

Use the following formula to calculate total cost of goods transferred out:

Therefore, total cost of goods transferred out is $160,734.

Use the following formula to calculate cost of EWIP:

Therefore, cost of EWIP is $9,185.

e.

Make cost reconciliation for Department A.

Explanation of Solution

Prepare cost reconciliation for Department A:

| Costs to account for | Amount($) | Cost accounted for | Amount($) |

| Cost of BWIP | 16,900 | Transferred out | 160,734 |

| Cost of the period | 153,020 | Cost of EWIP | 9,185 |

| Total cost | 169,920 | 169,919 |

Table (3)

Therefore, total cost of $169,920 has been reconciled (the difference of $1 is due to differences in rounding off certain amounts).

2.

Journalize the transactions that show the flow of manufacturing costs for department A. State the reasons for firms combining direct labor and overhead costs into one category.

Explanation of Solution

Pass journal entry to record cost of direct materials incurred as shown below:

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| Work in Process | 57,800 | |||

| Raw materials | 57,800 | |||

| (To record cost of direct materials incurred during the period ) |

Table (1)

Work in process is debited as cost has increased, so this account is debited and raw materials account is credited.

Pass journal entry to record conversion cost incurred as shown below:

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| Work in Process | 95,220 | |||

| Conversion cost | 95,220 | |||

| (To record conversion cost incurred during the period ) |

Work in process is debited as cost has increased, so this account is debited and conversion cost is credited.

Pass journal entry to record transfer cost from department A to department B as shown below:

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| Work in Process-Department B | 160,734 | |||

| Work in Process-Department A | 160,734 | |||

| (To record cost transferred from department A to department B ) |

The cost transferred from department A increases the cost of department B. This is the reason to debit the work in process of department B.

Cost is transferred from department A to department B. This is the reason that the amount of department A cost decreases. Therefore balance of work in process of department A is credited.

Direct labor is treated as any other overhead cost by some firms as direct labor carry out functions of other overhead costs such as inspection and maintenance. Another reason for merging these cost could be that fraction of direct labor cost acquires only small proportion of total manufacturing cost.

Want to see more full solutions like this?

Chapter 6 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- K-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.arrow_forwardSonoma Products Inc. manufactures a liquid product in one department. Due to the nature of the product and the process, units are regularly lost during production. Materials and conversion costs are added evenly throughout the process. The following summaries were prepared for March: Calculate the unit cost for materials, labor, and factory overhead for March and show the costs of units transferred to finished goods and to ending work in process inventory.arrow_forwardUsing the same data found in Exercise 6.22, assume the company uses the FIFO method. Required: Prepare a schedule of equivalent units, and compute the unit cost for the month of December. Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000.arrow_forward

- Aero Aluminum Inc. uses a process cost system. The records for May show the following information: Required: Prepare a cost of production summary for each department. (Hint: When preparing the Converting production summary, refer to the Rolling production summary for the costs transferred in during the month.)arrow_forwardTanaka Manufacturing Co. uses the process cost system. The following information for the month of December was obtained from the company’s books and from the production reports submitted by the department heads: Required: Prepare cost of production summaries for the Mixing, Blending, and Bottling (Hint: You must calculate the adjusted unit cost from Blending.) departments. Prepare a departmental cost work sheet. Draft the journal entries required to record the month’s operations. Prepare a statement of cost of goods manufactured for December. (Hint: Goods finished but not transferred to finished goods are considered part of work in process inventory.)arrow_forwardHeap Company manufactures a product that passes through two processes: Fabrication and Assembly. The following information was obtained for the Fabrication Department for September: a. All materials are added at the beginning of the process. b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs. c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs. d. Started in process, 95,000 units. Required: 1. Prepare a physical flow schedule. 2. Compute equivalent units using the weighted average method. 3. Compute equivalent units using the FIFO method.arrow_forward

- The standard cost summary for the most popular product of Phenom Products Co. is shown as follows, together with production and cost data for the period. One gallon each of liquid lead and varnish are added at the start of processing. The balance of the materials is added when the process is two-thirds complete. Labor and overhead are added evenly throughout the process. There were no units in process at the beginning of the month. Required: Calculate equivalent production for materials, labor, and overhead. (Be sure to refer to the standard cost summary to help determine the percentage of materials in ending work in process.) Calculate materials and labor variances and indicate whether they are favorable or unfavorable, using the diagram format shown in Figure 8-4. Determine the cost of materials and labor in the work in process account at the end of the month.arrow_forwardLacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Materials are added at the beginning of the process. Overhead is applied using the following drivers and activity rates: Other data for the Plate Cutting Department are as follows: Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production for: a. Direct materials b. Conversion costs 3. Calculate unit costs for: a. Direct materials b. Conversion costs c. Total manufacturing 4. Provide the following information: a. The total cost of units transferred out b. The journal entry for transferring costs from Plate Cutting to Welding c. The cost assigned to units in ending inventoryarrow_forwardThe following information concerns production in the Finishing Department for May. The Finishing Department uses the weighted average method. a. Determine the number of units in work in process inventory at the end of the month. b. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for May. Assume that direct materials are placed in process during production.arrow_forward

- Units of production data for the two departments of Atlantic Cable and Wire Company for July of the current fiscal year are as follows: Each department uses the weighted average method. For each department, assume that direct Materials are placed in process during production. a. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for the Drawing Department. b. Determine the number of whole units to be accounted for and to be assigned costs and the equivalent units of production for the Winding Department.arrow_forwardPrimera Company produces two products and uses a predetermined overhead rate to apply overhead. Primera currently applies overhead using a plantwide rate based on direct labor hours. Consideration is being given to the use of departmental overhead rates where overhead would be applied on the basis of direct labor hours in Department 1 and on the basis of machine hours in Department 2. At the beginning of the year, the following estimates are provided: Actual results reported by department and product during the year are as follows: Required: 1. Compute the plantwide predetermined overhead rate and calculate the overhead assigned to each product. 2. Calculate the predetermined departmental overhead rates and calculate the overhead assigned to each product. 3. Using departmental rates, compute the applied overhead for the year. What is the under- or overapplied overhead for the firm? 4. Prepare the journal entry that disposes of the overhead variance calculated in Requirement 3, assuming it is not material in amount. What additional information would you need if the variance is material to make the appropriate journal entry?arrow_forwardPrepare a cost of production report for the Cutting Department of Dalton Carpet Company for January. Assuming that direct materials are placed in process during production, use the weighted average method with the following data:arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,