Corporate Financial Accounting

14th Edition

ISBN: 9781305653535

Author: Carl Warren, James M. Reeve, Jonathan Duchac

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 6, Problem 6.7APR

Retail method; gross profit method

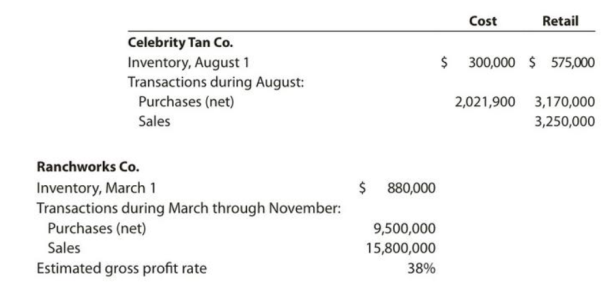

Selected data on inventory, purchases, and sales for Celebrity Tan Co. and Ranchworks Co. are as follows:

Instructions

- 1. Determine the estimated cost of the inventory of Celebrity Tan Co. on August 31 by the retail method, presenting details of the computations.

- 2. A. Estimate the cost of the inventory of Ranchworks Co. on November 30 by the gross profit method, presenting details of the computations.

B. Assume that Ranchworks Co. took a physical inventory on November 30 and discovered that $369,750 of inventory was on hand. What was the estimated loss of inventory due to theft or damage during March through November?

Expert Solution & Answer

Trending nowThis is a popular solution!

Chapter 6 Solutions

Corporate Financial Accounting

Ch. 6 - Prob. 1DQCh. 6 - Why is it important to periodically take a...Ch. 6 - Do the terms FIFO, LIFO, and weighted average...Ch. 6 - If inventory is being valued at cost and the price...Ch. 6 - Which of the three methods of inventory...Ch. 6 - If inventory is being valued at cost and the price...Ch. 6 - Using the following data, how should the inventory...Ch. 6 - The inventory at the end of the year was...Ch. 6 - Hutch Co. sold merchandise to Bibbins Company on...Ch. 6 - A manufacturer shipped merchandise to a retailer...

Ch. 6 - Cost flow methods The following three identical...Ch. 6 - Perpetual inventory using FIFO Beginning...Ch. 6 - Perpetual inventory using LIFO Beginning...Ch. 6 - Periodic inventory using FIFO, UFO, and weighted...Ch. 6 - Lower-of-cost-or-market method On the basis of the...Ch. 6 - Effect of inventory errors During the taking of...Ch. 6 - Control of inventories Triple Creek Hardware Store...Ch. 6 - Control of inventories Hardcase Luggage Shop is a...Ch. 6 - Perpetual inventory using FIFO Beginning...Ch. 6 - Perpetual inventory using LIFO Assume that the...Ch. 6 - Perpetual inventory using LIFO Beginning...Ch. 6 - Perpetual inventory using FIFO Assume that the...Ch. 6 - FIFO and UFO costs under perpetual inventory...Ch. 6 - Weighted average cost flow method under perpetual...Ch. 6 - Weighted average cost flow method under perpetual...Ch. 6 - Perpetual inventory using FIFO Assume that the...Ch. 6 - Perpetual inventory using LIFO Assume that the...Ch. 6 - Periodic inventory by three methods The units of...Ch. 6 - Periodic inventory by three methods; cost of goods...Ch. 6 - Comparing inventory methods Assume that a firm...Ch. 6 - Lower-of-cost-or-market inventory On the basis of...Ch. 6 - Inventory on the balance sheet Based on the data...Ch. 6 - Effect of errors n physical inventory Madison...Ch. 6 - Effect of errors in physical inventory Fonda...Ch. 6 - Prob. 6.19EXCh. 6 - Retail method A business using the retail method...Ch. 6 - Retail method A business using the retail method...Ch. 6 - Prob. 6.22EXCh. 6 - Retail method On the basis of the following data,...Ch. 6 - Prob. 6.24EXCh. 6 - Gross profit method Based on the following data,...Ch. 6 - Gross profit method Based on the following data,...Ch. 6 - FIFO perpetual inventory The beginning inventory...Ch. 6 - LIFO perpetual inventory The beginning inventory...Ch. 6 - Weighted average cost method with perpetual...Ch. 6 - Periodic inventory by three methods The beginning...Ch. 6 - Periodic inventory by three methods Dymac...Ch. 6 - Lower-of-cost-or-market inventory Data on the...Ch. 6 - Retail method; gross profit method Selected data...Ch. 6 - FIFO perpetual inventory The beginning inventory...Ch. 6 - LIFO perpetual inventory The beginning inventory...Ch. 6 - Weighted average cost method with perpetual...Ch. 6 - Periodic inventory by three methods The beginning...Ch. 6 - Periodic inventory by three methods Pappas...Ch. 6 - Lower-of-cost-or-market inventory Data on the...Ch. 6 - Retail method; gross profit method Selected data...Ch. 6 - Continuing Company AnalysisAmazon: Inventory...Ch. 6 - Costco, Walmart, Nordstrom: Inventory turnover and...Ch. 6 - Monster Beverage and Brown-Forman: Inventory...Ch. 6 - Prob. 6.4ADMCh. 6 - Ethics in Action Sizemo Elektroniks sells...Ch. 6 - Communication Golden Eagle Company began...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Retail method; gross profit method Selected data on inventory, purchases, and sales for Jaffe Co. and Coronado Co. are as follows: Instructions 1. Determine the estimated cost of the inventory of Jaffe Co. on February 28 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the inventory of Coronado Co. on October 31 by the gross profit method, presenting details of the computations. b. Assume that Coronado Co. took a physical inventory on October 31 and discovered that 366,500 of inventory was on hand. What was the estimated loss of inventory due to theft or damage during May through October?arrow_forwardSelected data on merchandise inventory, purchases, and sales for Celebrity Tan Co. and Ranchworks Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Celebrity Tan Co. on August 31 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Ranchworks Co. on November 30 by the gross profit method, presenting details of the computations. b. Assume that Ranchworks Co. took a physical inventory on November 30 and discovered that 369,750 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during March through November?arrow_forwardSelected data on merchandise inventory, purchases, and sales for Jaffe Co. and Coronado Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Jaffe Co. on February 28 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Coronado Co. on October 31 by the gross profit method, presenting details of the computations. b. Assume that Coronado Co. took a physical inventory on October 31 and discovered that 366,500 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during May through October?arrow_forward

- Inventory Costing Methods Crandall Distributors uses a perpetual inventory system and has the following data available for inventory, purchases, and sales for a recent year. Required: 1. Compute the cost of ending inventory and the cost of goods sold using the specific identification method. Assume the ending inventory is made up of 40 units from beginning inventory, 30 units from Purchase 1, 80 units from Purchase 2, and 40 units from Purchase 3. 2. Compute the cost of ending inventory and cost of goods sold using the FIFO inventory costing method. 3. Compute the cost of ending inventory and cost of goods sold using the LIFO inventory costing method. 4. Compute the cost of ending inventory and cost of goods sold using the average cost inventory costing method. ( Note: Use four decimal places for per-unit calculations and round all other numbers to the nearest dollar.) 5. CONCEPTUAL CONNECTION Compare the ending inventory and cost of goods sold computed under all four methods. What can you conclude about the effects of the inventory costing methods on the balance sheet and the income statement?arrow_forwardPerpetual inventory using LIFO Assume that the business in Exercise 6-3 maintains a perpetual inventory system, costing by the last-in, first-out method. Determine the cost of goods sold for each sale and the inventory balance after each sale, presenting the data in the form illustrated in Exhibit 4.arrow_forwardInventory Costing Methods Andersons Department Store has the following data for inventory, purchases, and sales of merchandise for December. Andersons uses a perpetual inventory system. All purchases and sales were for cash. Required: 1. Compute cost of goods sold and the cost of ending inventory using FIFO. 2. Compute cost of goods sold and the cost of ending inventory using LIFO. 3. Compute cost of goods sold and the cost of ending inventory using the average cost method. ( Note: Use four decimal places for per-unit calculations.) 4. Prepare the journal entries to record these transactions assuming Anderson chooses to use the FIFO method. 5. CONCEPTUAL CONNECTION Which method would result in the lowest amount paid for taxes?arrow_forward

- Lower-of-cost-or-market inventory Data on the physical inventory of Katus Products Co. as of December 31 follows: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and also at the lower of cost or market applied on an item-by-item basis, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet, and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forwardCalculate the cost of goods sold dollar value for B74 Company for the sale on November 20, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG).arrow_forwardPerpetual inventory using FIFO Assume that the business in Exercise 6-5 maintains a perpetual inventory system, costing by the first-in, first-out method. Determine the cost of goods sold for each sale and the inventory balance after each sale, presenting the data in the form illustrated in Exhibit 3.arrow_forward

- Inventory by three cost flow methods Details regarding the inventory of appliances on January 1, 20Y7, purchases invoices during the year, and the inventory count on December 31. 2O’7. of Amsterdam Appliances are summarized as follows: Instructions Discuss which method (FIFO or LIFO) would be preferred for income tax purposes in periods of (a) rising prices and (b) declining prices.arrow_forwardInventoriable Costs During the first month of operations, ABC Company incurred the following costs in ordering and receiving merchandise for resale. No inventory was sold. Required What amount do you recommend the company record as merchandise inventory on its balance sheet? Explain your answer. For any items not to be included in inventory, indicate their appropriate treatment in the financial statements.arrow_forwardLower-of-cost-or-market inventory Data on the physical inventory of Ashwood Products Company as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and also at the lower of cost or market applied on an item-by-item basis, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet, and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage LearningPrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage LearningPrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:9781337679503

Author:Gilbertson

Publisher:Cengage

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

Chapter 6 Merchandise Inventory; Author: Vicki Stewart;https://www.youtube.com/watch?v=DnrcQLD2yKU;License: Standard YouTube License, CC-BY

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License