Videos

Analysis of costs for a shipping department

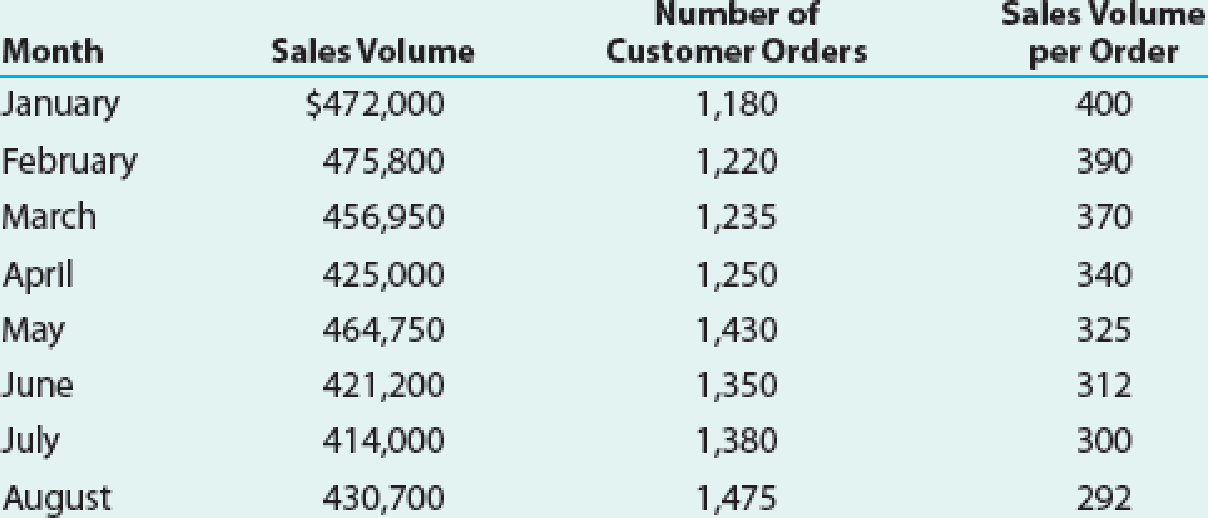

Sales volume has been dropping at Mumford Industries. During this time, the Shipping Department manager has been under severe financial constraints. Most of the Shipping Department’s efforts are related to pulling inventory from the warehouse for each order and performing the paperwork. The paperwork involves preparing shipping documents for each order. Thus, the pulling and paperwork effort associated with each sales order is essentially the same, regardless of the size of the order. The Shipping Department manager has discussed the financial situation with senior management. Senior management has responded by pointing out that because sales volume has been dropping, the amount of work in the Shipping Department also should be dropping. Thus, senior management told the Shipping Department manager that costs should be decreasing in the department.

The Shipping Department manager prepared the following information:

Given this information, how would you respond to senior management?

Want to see the full answer?

Check out a sample textbook solution

Chapter 6 Solutions

Managerial Accounting

- Kimball Company has developed the following cost formulas: Materialusage:Ym=80X;r=0.95Laborusage(direct):Yl=20X;r=0.96Overheadactivity:Yo=350,000+100X;r=0.75Sellingactivity:Ys=50,000+10X;r=0.93 where X=Directlaborhours The company has a policy of producing on demand and keeps very little, if any, finished goods inventory (thus, units produced equals units sold). Each unit uses one direct labor hour for production. The president of Kimball Company has recently implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. This policy was implemented because Kimballs industry is in a recession and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that minimally cover their variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Required: 1. Compute the total unit variable cost. Suppose that Kimball has an opportunity to accept an order for 20,000 units at 220 per unit. Should Kimball accept the order? (The order would not displace any of Kimballs regular orders.) 2. Explain the significance of the coefficient of correlation measures for the cost formulas. Did these measures have a bearing on your answer in Requirement 1? Should they have a bearing? Why or why not? 3. Suppose that a multiple regression equation is developed for overhead costs: Y = 100,000 + 100X1 + 5,000X2 + 300X3, where X1 = direct labor hours, X2 = number of setups, and X3 = engineering hours. The coefficient of determination for the equation is 0.94. Assume that the order of 20,000 units requires 12 setups and 600 engineering hours. Given this new information, should the company accept the special order referred to in Requirement 1? Is there any other information about cost behavior that you would like to have? Explain.arrow_forwardAssume you are the warehouse manager for Vinnies Vinyls, a multi-location business specializing in vinyl records. Vinniess operates under a cost-based transfer structure and the warehouse supplies all stores with the records. The stores can purchase records only from the warehouse, and the warehouse can only sell to Vinnies stores. The manager of the West store has some concerns relating to the stores financial performance and has asked for your help analyzing transfer costs. After calculating the operating income in dollars and the operating income percent, analyze the following financial information to determine costs that may need further investigation. (Hint: it may be helpful to perform a vertical analysis.)arrow_forwardIn 20X1, Don Blackburn, president of Price Electronics, received a report indicating that quality costs were 31% of sales. Faced with increasing pressures from imported goods. Don resolved to take measures to improve the overall quality of the companys products. After hiring a consultant in 20X1, the company began an aggressive program of total quality control. At the end of 20X5, Don requested an analysis of the progress the company had made in reducing and controlling quality costs. The accounting department assembled the following data: Required: 1. Compute the quality costs as a percentage of sales by category and in total for each year. 2. Prepare a multiple-year trend graph for quality costs, both by total costs and by category. Using the graph, assess the progress made in reducing and controlling quality costs. Does the graph provide evidence that quality has improved? Explain. 3. Using the 20X1 quality cost relationships (assume all costs are variable), calculate the quality costs that would have prevailed in 20X4. By how much did profits increase in 20X4 because of the quality improvement program? Repeat for 20X5.arrow_forward

- Kelly Gray, production manager, was upset with the latest performance report, which indicated that she was 100,000 over budget. Given the efforts that she and her workers had made, she was confident that they had met or beat the budget. Now, she was not only upset but also genuinely puzzled over the results. Three itemsdirect labor, power, and setupswere over budget. The actual costs for these three items follow: Kelly knew that her operation had produced more units than originally had been budgeted, so more power and labor had naturally been used. She also knew that the uncertainty in scheduling had led to more setups than planned. When she pointed this out to John Huang, the controller, he assured her that the budgeted costs had been adjusted for the increase in productive activity. Curious, Kelly questioned John about the methods used to make the adjustment. JOHN: If the actual level of activity differs from the original planned level, we adjust the budget by using budget formulasformulas that allow us to predict what the costs will be for different levels of activity. KELLY: The approach sounds reasonable. However, Im sure something is wrong here. Tell me exactly how you adjusted the costs of labor, power, and setups. JOHN: First, we obtain formulas for the individual items in the budget by using the method of least squares. We assume that cost variations can be explained by variations in productive activity where activity is measured by direct labor hours. Here is a list of the cost formulas for the three items you mentioned. The variable X is the number of direct labor hours: Labor cost = 10X Power cost = 5,000 + 4X Setup cost = 100,000 KELLY: I think I see the problem. Power costs dont have a lot to do with direct labor hours. They have more to do with machine hours. As production increases, machine hours increase more rapidly than direct labor hours. Also, ... JOHN: You know, you have a point. The coefficient of determination for power cost is only about 50 percent. That leaves a lot of unexplained cost variation. The coefficient for labor, however, is much betterit explains about 96 percent of the cost variation. Setup costs, of course, are fixed. KELLY: Well, as I was about to say, setup costs also have very little to do with direct labor hours. And I might add that they certainly are not fixedat least not all of them. We had to do more setups than our original plan called for because of the scheduling changes. And we have to pay our people when they work extra hours. It seems as if we are always paying overtime. I wonder if we simply do not have enough people for the setup activity. Supplies are used for each setup, and these are not cheap. Did you build these extra costs of increased setup activity into your budget? JOHN: No, we assumed that setup costs were fixed. I see now that some of them could vary as the number of setups increases. Kelly, let me see if I can develop some cost formulas based on better explanatory variables. Ill get back with you in a few days. Assume that after a few days work, John developed the following cost formulas, all with a coefficient of determination greater than 90 percent: Labor cost = 10X; where X = Direct labor hours Power cost = 68,000 + 0.9Y; where Y = Machine hours Setup cost = 98,000 + 400Z; where Z = Number of setups The actual measures of each of the activity drivers are as follows: Required: 1. Prepare a performance report for direct labor, power, and setups using the direct-labor-based formulas. 2. Prepare a performance report for direct labor, power, and setups using the multiple cost driver formulas that John developed. 3. Of the two approaches, which provides the most accurate picture of Kellys performance? Why? 4. After reviewing the approach to performance measurement, a consultant remarked that non-value-added cost trend reports would be a much better performance measurement approach than comparing actual costs with budgeted costseven if activity flexible budgets were used. Do you agree or disagree? Explain.arrow_forwardEvaluating selling and administrative cost allocations Gordon Gecco Furniture Company has two major product lines with the following characteristics: Commercial office furniture: Few large orders, little advertising support, shipments in full truckloads, and low handling complexity Home office furniture: Many small orders, large advertising support, shipments in partial truckloads, and high handling complexity The company produced the following profitability report for management: The selling and administrative expenses are allocated to the products on the basis of relative sales dollars. Evaluate the accuracy of this report and recommend an alternative approach.arrow_forwardTonya Martin, CMA and controller or the Parts Division of Gunderson Inc., was meeting with Doug Adams, manager of the division. The topic of discussion was the assignment of overhead costs to jobs and their impact on the divisions pricing decisions. Their conversation was as follows: Tonya: Doug, as you know, about 25% of our business is based on government contracts, with the other 75% based on jobs from private sources won through bidding. During the last several years, our private business has declined. We have been losing more bids than usual. After some careful investigation, I have concluded that we are overpricing some jobs because of improper assignment of overhead costs. Some jobs are also being underpriced. Unfortunately, the jobs being overpriced are coming from our higher-volume, labor-intensive products, so we are losing business. Dong: I think I understand. Jobs associated with our high-volume products are being assigned more overhead than they should be receiving. Then when we add our standard 40% markup, we end up with a higher price than our competitors, who assign costs more accurately. Tonya: Exactly. We have two producing departments, one labor-intensive and the other machine-intensive. The labor-intensive department generates much less overhead than the machine-intensive department. Furthermore, virtually all of our high-volume jobs are labor-intensive. We have been using a plantwide rate based on direct labor hours to assign overhead to all jobs. As a result, the high-volume, labor-intensive jobs receive a greater share of the machine-intensive departments overhead than they deserve. This problem can be greatly alleviated by switching to departmental overhead rates. For example, an average high-volume job would be assigned 100,000 of overhead using a plantwide rate and only 70,000 using departmental rates. The change would lower our bidding price on high-volume jobs by an average of 42,000 per job. By increasing the accuracy of our product costing, we can make better pricing decisions and win back much of our private-sector business. Doug: Sounds good. When can you implement the change in overhead rates? Tonya: It wont take long. I can have the new system working within four to six weekscertainly by the start of the new fiscal year. Doug: Hold it. I just thought of a possible complication. As I recall, most of our government contract work is done in the labor-intensive department. This new overhead assignment scheme will push down the cost on the government jobs, and we will lose revenues. They pay us full cost plus our standard markup. This business is not threatened by our current costing procedures, but we cant switch our rates for only the private business. Government auditors would question the lack of consistency in our costing procedures. Tonya: You do have a point. I thought of this issue also. According to my estimates, we will gain more revenues from the private sector than we will lose from our government contracts. Besides, the costs of our government jobs are distorted. In effect, we are overcharging the government. Doug: They dont know that and never would unless we switch our overhead assignment procedures. I think I have the solution. Officially, lets keep our plantwide overhead rate. All of the official records will reflect this overhead costing approach for both our private and government business. Unofficially. I want you to develop a separate set of books that can be used to generate the information we need to prepare competitive bids for our private-sector business. Required: 1. Do you believe that the solution proposed by Doug is ethical? Explain. 2. Suppose that Tonya decides that Dougs solution is not right and objects strongly. Further suppose that, despite Tonyas objections, Doug insists strongly on implementing the action. What should Tonya do?arrow_forward

- Jackie Iverson was furious. She was about ready to fire Tom Rich, her purchasing agent. Just a month ago, she had given him a salary increase and a bonus for his performance. She had been especially pleased with his ability to meet or beat the price standards. But now, she found out that it was because of a huge purchase of raw materials. It would take months to use that inventory, and there was hardly space to store it. In the meantime, space had to be found for the other materials supplies that would be ordered and processed on a regular basis. Additionally, it was a lot of capital to tie up in inventorymoney that could have been used to help finance the cash needs of the new product just coming online. Her interview with Tom was frustrating. He was defensive, arguing that he thought she wanted those standards met and that the means were not that important. He also pointed out that quantity purchases were the only way to meet the price standards. Otherwise, an unfavorable variance would have been realized. Required: 1. CONCEPTUAL CONNECTION Why did Tom Rich purchase the large quantity of raw materials? Do you think that this behavior was the objective of the price standard? If not, what is the objective(s)? 2. CONCEPTUAL CONNECTION Suppose that Tom is right and that the only way to meet the price standards is through the use of quantity discounts. Also, assume that using quantity discounts is not a desirable practice for this company. What would you do to solve this dilemma? 3. CONCEPTUAL CONNECTION Should Tom be fired? Explain.arrow_forwardThe Personnel Department at LastCall Enterprises handles many administrative tasks for the two divisions that make up LastCall: LaidBack and StressedOut. LaidBack division manages the company’s traditional business line. This business, although lucrative, is currently not growing. StressedOut, on the other hand, is the company’s new business, which has experienced double-digit growth for each of the last three years. The cost allocation system at LastCall allocates all corporate costs to the divisions based on a variety of cost allocation bases. Personnel costs are allocated based on the average number of employees in the two divisions. There are two basic activities in the Personnel Department. The first, called employee maintenance, manages employee records. Virtually all of this activity occurs when employees are hired or leave the company. The other activity is payroll, which is an ongoing activity and requires the same amount of work for each employee regardless of the…arrow_forwardThe Personnel Department at LastCall Enterprises handles many administrative tasks for the two divisions that make up LastCall: LaidBack and StressedOut. LaidBack division manages the company’s traditional business line. This business, although lucrative, is currently not growing. StressedOut, on the other hand, is the company’s new business, which has experienced double-digit growth for each of the last three years. The cost allocation system at LastCall allocates all corporate costs to the divisions based on a variety of cost allocation bases. Personnel costs are allocated based on the average number of employees in the two divisions. There are two basic activities in the Personnel Department. The first, which is called employee maintenance, manages employee records. Virtually all of this activity occurs when employees are hired or leave the company. The other activity is payroll, which is an ongoing activity and requires the same amount of work for each employee regardless of the…arrow_forward

- The Personnel Department at LastCall Enterprises handles many administrative tasks for the two divisions that make up LastCall: LaidBack and StressedOut. LaidBack division manages the company’s traditional business line. This business, although lucrative, is currently not growing. StressedOut, on the other hand, is the company’s new business, which has experienced double-digit growth for each of the last three years. The cost allocation system at LastCall allocates all corporate costs to the divisions based on a variety of cost allocation bases. Personnel costs are allocated based on the average number of employees in the two divisions. There are two basic activities in the Personnel Department. The first, called employee maintenance, manages employee records. Virtually all of this activity occurs when employees are hired or leave the company. The other activity is payroll, which is an ongoing activity and requires the same amount of work for each employee regardless of the employee’s…arrow_forwardWithin a company is a (micro)economy that is monitored by the accounting procedures. In terms of the accounts, the various departments "produce" costs, some of which are internal and some of which are direct costs. This problem shows how an open Leontief model can be used to determine departmental costs. The sales department of an auto dealership charges 10% of its total monthly costs to the service department, and the service department charges 20% of its total monthly costs to the sales department. During a given month, the direct costs are $88,200 for sales and $29,400 for service. Find the total costs (in dollars) of each department. (Round your answers to the nearest whole number.) sales department $ service department $arrow_forwardThe head of operations of a manufacturing company has conducted an analysis with respect to the capacity of his production line. The major findings are the following: Theoretical capacity is 530 units per day. The effective capacity is 515 units per day The process capacity is 450 units per day. Two projects have been proposed to increase the capacity. The first proposal focuses on improving maintenance in order to reduce machine breakdowns. The second proposal focuses on increasing the capacity of the inventory buffer between various stages. Given that there is only enough budget to implement one of the proposals, which proposal should be selected based on the given information. Clearly motivate your answer. Please do fast.. ASAP ..fast pleasearrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning