Concept explainers

Videos

Using FIFO for Multiproduct Inventory Transactions (Chapters 6 and 7)

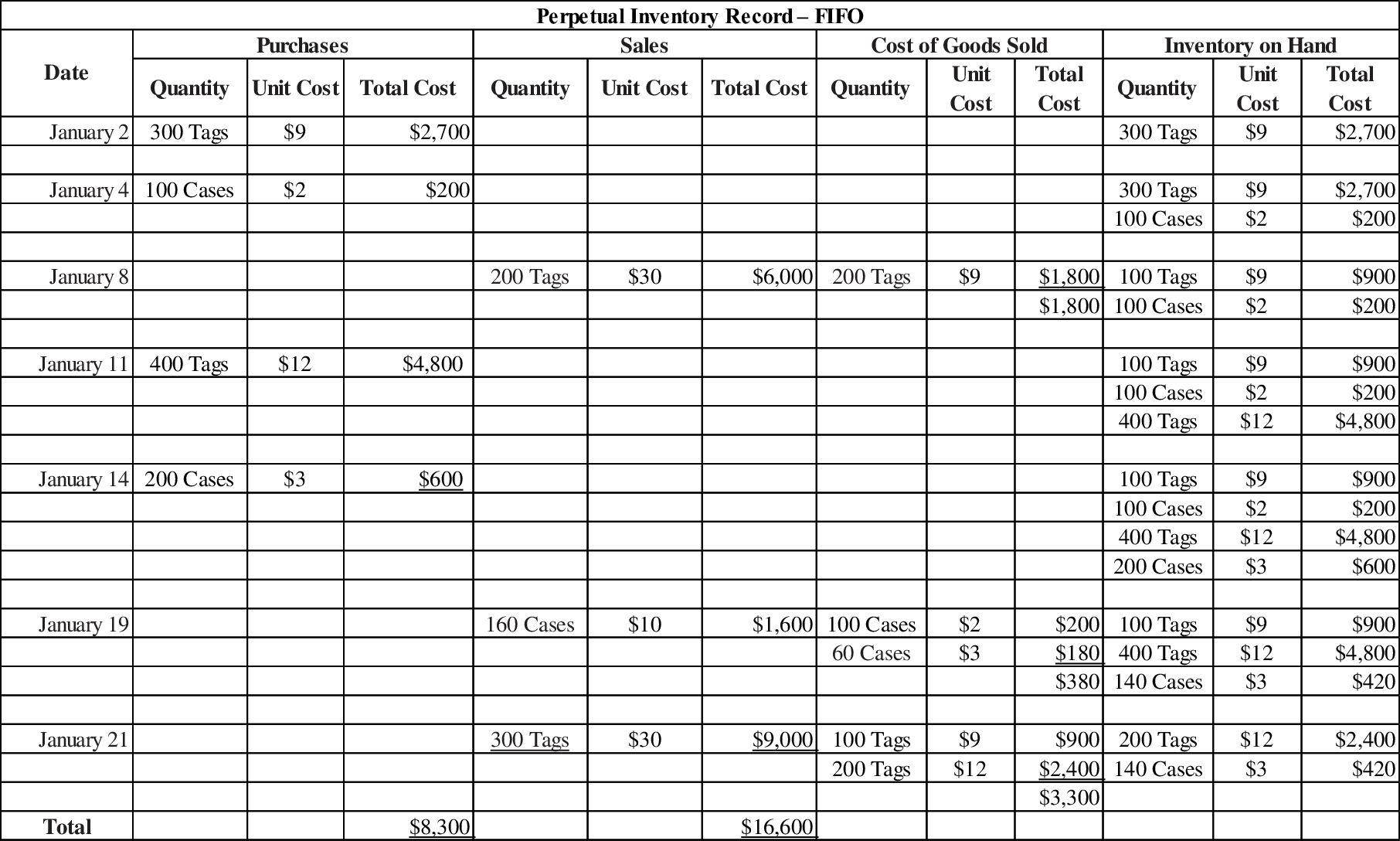

TrackR, Inc., (TI) has developed a coin-sized tracking tag that attaches to key rings, wallets, and other items and can be prompted to emit a signal using a smartphone app. TI sells these tags, as well as water-resistant cases for the tags, with terms FOB shipping point. Assume TI has no inventory at the beginning of the month, and it has outsourced the production of its tags and cases. TI uses FIFO and has entered into the following transactions:

| Jan. 2: | TI purchased and received 300 tags from Xioasi Manufacturing (XM) at a cost of $9 per tag, n/15. |

| Jan. 4: | TI purchased and received 100 cases from Bachittar Products (BP) at a cost of $2 per case, n/20. |

| Jan. 6: | TI paid cash for the tags purchased from XM on Jan. 2. |

| Jan. 8: | TI mailed 200 tags via the U.S. Postal Service (USPS) to customers at a price of $30 per tag, on account. |

| Jan. 11: | TI purchased and received 400 tags from XM at a cost of $12 per tag, n/15. |

| Jan. 14: | TI purchased and received 200 cases from BP at a cost of $3 per case, n/20. |

| Jan. 16: | TI paid cash for the cases purchased from BP on Jan. 4. |

| Jan. 9: | TI mailed 160 cases via the USPS to customers at a price of $10 per case, on account. |

| Jan. 21: | TI mailed 300 tags to customers at a price of $30 per tag. |

Required:

- 1. Prepare

journal entries for each of the above dates, assuming TI uses a perpetual inventory system. - 2. Calculate the dollars of gross profit and the gross profit percentage from selling (a) tags and (b) cases.

- 3. Which product line yields more dollars of profit?

- 4. Which product line yields more profit per dollar of sales?

1.

Prepare journal entries for the given transactions of Company TI; assume that the company uses perpetual inventory system.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Perpetual inventory system: The method or system of maintaining, recording, and adjusting the inventory perpetually throughout the year, is referred to as perpetual inventory system.

Prepare journal entry for the given transaction of Company TAC; assume that the company uses weighted average in its perpetual inventory system as follows:

- Prepare journal entry for the transaction occurred on January 2.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 2 | Inventories (Refer working note 1) | 2,700 | ||

| Accounts Payable | 2,700 | ||||

| (To record the purchase of 300 tags at a cost of $9 on account) | |||||

Table (1)

- Inventory is an asset and increased by $2,700. Therefore, debit the inventory account with $2,700.

- Accounts Payable is a liability and decreased by $2,700. Therefore, credit the accounts payable account with $2,700.

- Prepare journal entry for the transaction occurred on January 4.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 4 | Inventories (Refer working note 1) | 200 | ||

| Accounts Payable | 200 | ||||

| (To record the purchase of 100 tags at a cost of $2 on account) | |||||

Table (2)

- Inventory is an asset and increased by $200. Therefore, debit the inventory account with $200.

- Accounts Payable is a liability and decreased by $200. Therefore, credit the accounts payable account with $200.

- Prepare journal entry for the transaction occurred on January 6.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 6 | Accounts Payable | 2,700 | ||

| Cash | 2,700 | ||||

| (To record the payment of cash for the goods purchased on January 2) | |||||

Table (3)

- Accounts Payable is a liability and increased by $2,700. Therefore, debit the accounts payable account with $2,700.

- Cash is an asset and there is a decrease in the value of asset. So credit the cash account with $2,700

- Prepare journal entry for the transaction occurred on January 8.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 8 | Accounts Receivable (Refer working note 1) | 6,000 | ||

| Sales Revenue | 6,000 | ||||

| (To record sale of inventories on account) | |||||

| Cost of Goods Sold (Refer working note 1) | 1,800 | ||||

| Inventories | 1,800 | ||||

| (To record the cost of goods sold ) | |||||

Table (4)

Description:

- Accounts Receivable is an asset and there is an increase in the value of asset. So debit the accounts receivable account with $6,000.

- Sales Revenue is a component of stockholder’s equity and there is an increase in the value of stockholder’s equity. So credit the sales revenue account for $6,000.

- Cost of goods sold is an expense and increased; hence it has decreased the equity by $1,800. Therefore, debit cost of goods sold account with $1,800.

- Inventory is an asset and decreased by $1,800. Therefore, credit the inventory account with $1,800.

- Prepare journal entry for the transaction occurred on January 11.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 11 | Inventories (Refer working note 1) | 4,800 | ||

| Accounts Payable | 4,800 | ||||

| (To record the purchase of 300 tags at a cost of $9 on account) | |||||

Table (5)

- Inventory is an asset and increased by $4,800. Therefore, debit the inventory account with $4,800.

- Accounts Payable is a liability and decreased by $4,800. Therefore, credit the accounts payable account with $4,800.

- Prepare journal entry for the transaction occurred on January 14.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 14 | Inventories (Refer working note 1) | 600 | ||

| Accounts Payable | 600 | ||||

| (To record the purchase of 300 tags at a cost of $9 on account) | |||||

Table (6)

- Inventory is an asset and increased by $600. Therefore, debit the inventory account with $600.

- Accounts Payable is a liability and decreased by $600. Therefore, credit the accounts payable account with $600.

- Prepare journal entry for the transaction occurred on January 16.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 16 | Accounts Payable | 200 | ||

| Cash | 200 | ||||

| (To record the payment of cash for the goods purchased on January 4) | |||||

Table (7)

- Accounts Payable is a liability and increased by $200. Therefore, debit the accounts payable account with $200.

- Cash is an asset and there is a decrease in the value of asset. So credit the cash account with $200.

- Prepare journal entry for the transaction occurred on January 19.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 19 | Accounts Receivable (Refer working note 1) | 1,600 | ||

| Sales Revenue | 1,600 | ||||

| (To record sale of inventories on account) | |||||

| Cost of Goods Sold (Refer working note 1) | 380 | ||||

| Inventories | 380 | ||||

| (To record the cost of goods sold ) | |||||

Table (8)

Description:

- Accounts Receivable is an asset and there is an increase in the value of asset. So debit the accounts receivable account with $6,000.

- Sales Revenue is a component of stockholder’s equity and there is an increase in the value of stockholder’s equity. So credit the sales revenue account for $6,000.

- Cost of goods sold is an expense and increased; hence it has decreased the equity by $380. Therefore, debit cost of goods sold account with $380.

- Inventory is an asset and decreased by $380. Therefore, credit the inventory account with $380.

- Prepare journal entry for the transaction occurred on January 21.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| January | 19 | Accounts Receivable (Refer working note 1) | 9,000 | ||

| Sales Revenue | 9,000 | ||||

| (To record sale of inventories on account) | |||||

| Cost of Goods Sold (Refer working note 1) | 3,300 | ||||

| Inventories | 3,300 | ||||

| (To record the cost of goods sold ) | |||||

Table (9)

Description:

- Accounts Receivable is an asset and there is an increase in the value of asset. So debit the accounts receivable account with $9,000.

- Sales Revenue is a component of stockholder’s equity and there is an increase in the value of stockholder’s equity. So credit the sales revenue account for $9,000.

- Cost of goods sold is an expense and increased; hence it has decreased the equity by $3,300. Therefore, debit cost of goods sold account with $3,300.

- Inventory is an asset and decreased by $3,300. Therefore, credit the inventory account with $3,300.

Working note 1:

Calculate the amount of sales, cost of goods sold, purchases and inventory on hand (Ending inventory) under FIFO method as follows:

Figure (1)

2.

Calculate the dollars of gross profit and the gross profit percentage from selling the following items:

- a) Tags and

- b) Cases.

Explanation of Solution

Gross margin (gross profit): Gross margin is the amount of revenue earned from goods sold over the costs incurred for the goods sold.

Gross margin percentage: The percentage of gross profit generated by every dollar of net sales is referred to as gross profit percentage. This ratio measures the profitability of a company by quantifying the amount of income earned from sales revenue generated after cost of goods sold are paid. The higher the ratio, the more ability to cover operating expenses.

a. Calculate the dollars of gross profit and the gross profit percentage from the sale of Tags as follows:

Calculate the dollars of gross profit as follows:

| Particulars | $ |

| Sales Revenue (Refer working note 1) | $6,000 |

| Sales Revenue (Refer working note 1) | 9,000 |

| Total Sales | 15,000 |

| Less: Cost of Goods Sold | |

| On January 8 (Refer working note 1) | 1,800 |

| On January 21 (Refer working note 1) | 3,300 |

| Gross Profit | $9,900 |

Table (10)

Calculate the dollars of gross profit percentage as follows:

b. Calculate the dollars of gross profit and the gross profit percentage from the sale of Cases as follows:

Calculate the dollars of gross profit as follows:

| Particulars | $ |

| Sales Revenue (Refer working note 1) | $1,600 |

| Less: Cost of Goods Sold | |

| On January 19 (Refer working note 1) | 380 |

| Gross Profit | $1,220 |

Table (11)

Calculate the dollars of gross profit percentage as follows:

3.

State the product line that yields more dollars of profit.

Explanation of Solution

State the product line that yields more dollars of profit as follows:

In this case, the Tags product line yields more dollars of profit than Cases product line. From the above calculation it is clear that the gross profit of Tags product line ($9,900) is more than the gross profit of Cases product line ($1,220).

4.

State the product line that yields more profit per dollar of sales.

Explanation of Solution

State the product line that yields more profit per dollar of sales as follows:

The cases product line yields more profit per dollar of sales than the Tags product line. Since the cases product line has a higher gross profit percentage of 76.25%, while the tags product line has a gross profit percentage of only 66%.

Want to see more full solutions like this?

Chapter 7 Solutions

Fundamentals Of Financial Accounting

- Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2016 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section, and place a check mark () in the Posting Reference column. Journalize the transactions for July, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardYour client, Daves Sport Shop, sells sports equipment and clothing in three retail outlets in New York City. During 2019, the CFO decided that keeping track of inventory using a combination of QuickBooks and spreadsheets was not an efficient way to manage the stores inventories. So Daves purchased an inventory management system for 9,000 that allowed the entity to keep track of inventory, as well as automate ordering and purchasing, without replacing QuickBooks for its accounting function. The CFO would like to know whether the cost of the inventory management program can be expensed in the year of purchase. Write a letter to the CFO, Cassandra Martin, that addresses the tax treatment of purchased software. Cassandras mailing address is 867 Broadway, New York, NY 10003.arrow_forwardThe beginning inventory for Funky Party Supplies and data on purchases and sales for a three-month period are shown in Problem 7-1A. Instructions 1. Determine the inventory on March 31, 2016, and the cost of goods sold for the three-month period, using the first-in, first-out method and the periodic inventory system. 2. Determine the inventory on March 31, 2016, and the cost of goods sold for the three-month period, using the last-in, first-out method and the periodic inventory system. 3. Determine the inventory on March 31, 2016, and the cost of goods sold for the three-month period, using the weighted average cost method and the periodic inventory system. Round the weighted average unit cost to the nearest cent. 4. Compare the gross profit and the March 31, 2016, inventories, using the following column headings:arrow_forward

- E7-12 (Algo) Using FIFO for Multiproduct Inventory Transactions (Chapters 6 and 7) [LO 6-3, LO 6-4, LO 7-3] Skip to question [The following information applies to the questions displayed below.]FindMe Incorporated, (FI) has developed a coin-sized tracking tag that attaches to key rings, wallets, and other items and can be prompted to emit a signal using a smartphone app. FI sells these tags, as well as water-resistant cases for the tags, with terms FOB shipping point. Assume FI has no inventory at the beginning of the month, and it has outsourced the production of its tags and cases. FI uses FIFO and has entered into the following transactions: January 2 FI purchased and received 330 tags from Xioasi Manufacturing (XM) at a cost of $11 per tag, n/15. January 4 FI purchased and received 130 cases from Bachittar Products (BP) at a cost of $2 per case, n/20. January 6 FI paid cash for the tags purchased from XM on January 2. January 8 FI mailed 230 tags via the U.S. Postal…arrow_forwardAssume the perpetual inventory system is used unless stated otherwise. Round all numbers to the nearest whole dollar unless stated otherwise. Comparing periodic and perpetual inventory systems For each statement below, identify whether the statement applies to the periodic inventory system, the perpetual inventory system, or both. Normally used for relatively inexpensive goods. Keeps a running computerized record of merchandise inventory. Achieves better control over merchandise inventory. Requires a physical count of inventory to determine the quantities on hand. Uses bar codes to keep up-to-the-minute records of inventory.arrow_forwardyou found the following information relating to certain inventory transactions from your observation of the client’s physical count and review of sales and purchases cutoff: a. Goods costing P180,000 were received from a vendor on January 3, 2021. The goods were not included in the physical count. The related invoice was received and recorded on December 30, 2020. The goods were shipped on December 31, 2020, terms FOB shipping point. b. Goods costing P200,000, sold for P300,000, were shipped on December 31, 2020, and were received by the customer on January 2, 2021. The terms of the invoice were FOB shipping point. The goods were included in the ending inventory for 2020 and the sale was recorded in 2021. c. The invoice for goods costing P150,000 was received and recorded as a purchase on December 31, 2020. The related goods shipped FOB destination were received on January 2, 2021 but were included in the physical inventory as goods in transit. d. A P600,000 shipment of goods to a…arrow_forward

- Chipolo sells a coin-sized tracking tag that attaches to keys, wallets, and other personal items. Chipolo began January with an inventory of 200 tags purchased from its supplier in November last year at a cost of $12 per tag, plus 100 tags purchased in December last year at a cost of $15 per tag. Chipolo sells the tags at a price of $30 per tag, on account with terms n/30, FOB destination. Chipolo uses a perpetual inventory system to account for the following transactions. Jan. 8 Chipolo gave 250 tags to a courier company (FedEx) to deliver to customers. Jan. 9 FedEx confirmed that all 250 tags were delivered today to customers. Jan. 11 Chipolo ordered 350 tags from its supplier. The supplier was out of stock but promised to send them to Chipolo as soon as possible. Chipolo agreed to a cost of $21 per tag, n/30. Jan. 17 Chipolo received cash payment from customers for 125 of the tags delivered 8 days earlier. Jan. 21 The 350 tags ordered on January 11…arrow_forwardChipolo sells a coin-sized tracking tag that attaches to keys, wallets, and other personal items. Chipolo began January with an inventory of 200 tags purchased from its supplier in November last year at a cost of $12 per tag, plus 100 tags purchased in December last year at a cost of $15 per tag. Chipolo sells the tags at a price of $30 per tag, on account with terms n/30, FOB destination. Chipolo uses a perpetual inventory system to account for the following transactions. Jan. 8 Chipolo gave 250 tags to a courier company (FedEx) to deliver to customers. Jan. 9 FedEx confirmed that all 250 tags were delivered today to customers. Jan. 11 Chipolo ordered 350 tags from its supplier. The supplier was out of stock but promised to send them to Chipolo as soon as possible. Chipolo agreed to a cost of $21 per tag, n/30. Jan. 17 Chipolo received cash payment from customers for 125 of the tags delivered 8 days earlier. Jan. 21 The 350 tags ordered on January 11…arrow_forwardChipolo sells a coin-sized tracking tag that attaches to keys, wallets, and other personal items. Chipolo began January with an inventory of 200 tags purchased from its supplier in November last year at a cost of $12 per tag, plus 100 tags purchased in December last year at a cost of $15 per tag. Chipolo sells the tags at a price of $30 per tag, on account with terms n/30, FOB destination. Chipolo uses a perpetual inventory system to account for the following transactions. Jan. 8 Chipolo gave 250 tags to a courier company (FedEx) to deliver to customers. Jan. 9 FedEx confirmed that all 250 tags were delivered today to customers. Jan. 11 Chipolo ordered 350 tags from its supplier. The supplier was out of stock but promised to send them to Chipolo as soon as possible. Chipolo agreed to a cost of $21 per tag, n/30. Jan. 17 Chipolo received cash payment from customers for 125 of the tags delivered 8 days earlier. Jan. 21 The 350 tags ordered on January 11…arrow_forward

- Assume you're the assistant controller at a bookstore that's run by an independent bookseller. Manual, periodic inventory updating, physical counts at year end, and the FIFO technique for inventory costs are all used by the firm. How would you tackle the question of whether or not the organization should move to computerized perpetual inventory updating? Can you make a compelling case for the advantages of perpetual? Explain.arrow_forwardThe following data is available for the month of September for two items of inventory that might soon be render obsolete for Island Solutions. Inventory balances at September 1, 2023, were as follows: USB-C(TA3)HUB Date Purchases Sales Sept 5 500 @ $450 10 500 @ $540 15 400 @ $475 20 400 @ $570 25 300 @ $500 USB-C(TB3) HUB Date Purchases Sales Sept 10 600 @ $900 19 300 @ $950 25 900 @ $1,080 28 500 @ $1,000 30 600 @ $1,140 In addition to the inventory data provided above, Island Solutions accountant has made the following projections in light of the market changes. USB-C(TA3)HUB USB-C(TB3)HUB Expected unit selling price (net of cost to sell) $580 $1,050 Costs to complete 30 150 1. Assume that Island Solutions applies LCNRV at the individual product level, determine the value of inventory that should be reported on the statement of financial position on September 30, 2023. 2. Assume Island…arrow_forwardTriple Creek Hardware Store currently uses a periodic inventory system. Kevin Carlton, the owner, is considering the purchase of a computer system that would make it feasible to switch to a perpetual inventory system.Kevin is unhappy with the periodic inventory system because it does not provide timely information on inventory levels. Kevin has noticed on several occasions that the store runs out of good-selling items, while too many poor-selling items are on hand.Kevin is also concerned about lost sales while a physical inventory is being taken. Triple Creek Hardware currently takes a physical inventory twice a year. To minimize distractions, the store is closed on the day inventory is taken. Kevin believes that closing the store is the only way to get an accurate inventory count. Will switching to a perpetual inventory system strengthen Triple Creek Hardware’s control over inventory items? Will switching to a perpetual inventory system eliminate the need for a physical inventory…arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT