Concept explainers

Videos

Absorption and Variable Costing; Production Constant, Sales Fluctuate L07—1, L07—2, L07—3

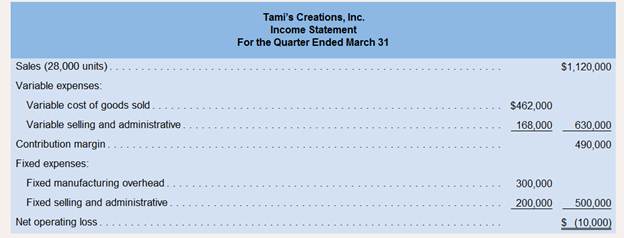

Tami Tyler opened Tami’s Creations; Inc., a small manufacturing company, at the beginning of the year. Getting the company through its first quarter of operations placed a considerable strain on Ms. Tyler s

Ms. Tyler is discouraged over the loss shown for the quarter, particularly because she had planned to use the statement as support for a bank loan. Another friend, a CPA; insists that the company should be using absorption costing rather than variable costing and argues that if absorption costing had been used the company probably would have reported at least some profit for the quarter.

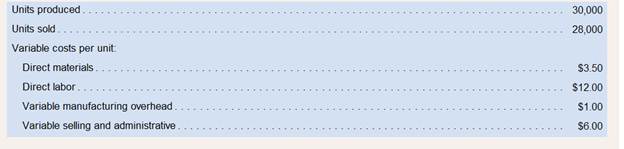

At this point; Ms. Tyler is manufacturing only one product—a swimsuit. Production and cost data relating to the swimsuit for the first quarter follow:

Required:

1. Complete the following:

a. Compute the unit product cost under absorption costing.

b. What is the company’s absorption costing net operating income (loss) for the quarter?

c. Reconcile the variable and absorption costing net operating income (loss) figures.

2. Was the CPA correct in suggesting that the company really earned a “profit” for the quarter? Explain.

3. During the second quarter of operations, the company again produced 30,000 units but sold 32,000 units. (Assume no change in total fixed costs.)

a. What is the company’s variable costing net operating income (loss) for the second quarter?

b. What is the company’s absorption costing net operating income (loss) for the second quarter?

c. Reconcile the variable costing and absorption costing net operating incomes for the second quarter.

1:

Absorption Costing: is also known as Full costing method. In this method, those costs which vary directly with production are considered in product cost. Also, fixed Manufacturing Expenses are treated as product cost only. Selling Expenses (since they do not vary with production), both variable and fixed, are charged off completely in the period in which the expenses get incurred.

Unit product Cost and Net Operating Income for the quarter.

Answer to Problem 23P

Solution (a):

| Computation of Unit Product Cost under Absorption Costing | ||

| Cost per unit | ||

| Direct Material | $ 3.5 | |

| Direct Labor | $ 12.0 | |

| Variable Manufacturing Overhead | $ 1.0 | |

| Fixed Manufacturing Overhead | $ 10.0 | |

| Total Product Cost | $ 26.5 | |

Explanation of Solution

- Given:

Direct Material, Direct Labor and Variable Manufacturing Overhead are given in the question

- Formula:

- Calculation:

The unit product cost under absorption costing is $ 26.50

Absorption Costing: is also known as Full costing method. In this method, those costs which vary directly with production are considered in product cost. Also, fixed Manufacturing Expenses are treated as product cost only. Selling Expenses (since they do not vary with production), both variable and fixed, are charged off completely in the period in which the expenses get incurred.

Unit product Cost and Net Operating Income for the quarter.

Answer to Problem 23P

Solution (b):

| Income Statement (Contribution Format) under Absorption Costing | |

| Quarter 1 | |

| Sales | $1,120,000 |

| Cost of Goods Sold | $ 742,000 |

| Gross Margin | $ 378,000 |

| Selling & Administrative Expenses | $ 368,000 |

| Net Operating Income | $ 10,000 |

Explanation of Solution

The income statement under this method requires following computations:

Sales − Cost of Goods Sold = Gross Margin

Gross Margin − Total Selling Cost = Net Operating Income

Cost of Goods Sold comprises of variable as well as fixed manufacturing cost.

Total selling expenses comprise of variable as well as fixed selling cost.

- Given:

Sales are given as $ 1,120,000

- Formula:

- Calculation:

- Opening Stock = Nil

Fixed selling expenses = $ 200,000

Net Operating Income is $ 10,000

Reconciliation between Variable costing and Absorption Costing

Answer to Problem 23P

Solution:

| Reconciliation | |

| Quarter 1 | |

| Net Operating Income as per Variable Costing | $ (10,000) |

| Closing Stock | 2,000 |

| Opening Stock | - |

| Difference in Stock (Closing - Opening) | 2,000 |

| Fixed Overhead per unit | $ 10 |

| Fixed Overhead on Difference Stock | 20,000 |

| Profit as per Absorption Costing | $ 10,000 |

Explanation of Solution

Reconciliation is done between Net Operating Income as per Variable Costing and that as per Absorption Costing.

The difference between the two net operating income figures would be on account of fixed cost element on inventory.

- Net operating income under variable costing is taken as a base;

- Difference of stock quantity is computed as closing stock less opening stock

- This difference in stock is multiplied with fixed overhead per unit (as computed in Unit product cost). This will the amount of fixed overhead which has been deferred over to the next period;

- Adding this fixed overhead amount to Net Operating Income as per Variable Costing will give Net Operating Income as per Absorption Costing.

- Given

Opening stock is given as Nil.

- Formula

Under Variable costing, the inventory is valued at Unit product cost as per variable costing method which is direct material plus direct labour plus variable manufacturing expenses whereas under Absorption costing, the inventory is valued at Unit product cost as per absorption costing method which is direct material plus direct labour plus variable manufacturing expenses plus fixed cost per unit.

Due to the inclusion of fixed cost in inventory in absorption costing, following is the impact:

- Opening inventory is higher resulting in decrease in profit

- Closing inventory is higher resulting in increase in profit

2:

Whether company earned profit for the quarter under review

Explanation of Solution

As per CPA the Company did earn profit under absorption costing. However, under absorption costing the fixed expenses get deferred to next period due to absorption in closing stock even though they have actually been incurred.

Though absorption costing shows profit, this is not real profit.

Reconciliation between Variable costing and Absorption Costing

Answer to Problem 23P

3:

Solution (a):

| Tami Tyler's Creations Inc

Income Statement (Contribution Format) under Absorption Costing | |

| Quarter 2 | |

| Sales | $1,280,000 |

| Cost of Goods Sold | $ 848,000 |

| Gross Margin | $ 432,000 |

| Selling & Administrative Expenses | $ 392,000 |

| Net Operating Income | $ 40,000 |

Explanation of Solution

- Formula:

- Calculation:

Value of Opening Stock = $ 53,000

Fixed selling expenses = $ 200,000

Reconciliation between Variable costing and Absorption Costing

Answer to Problem 23P

Solution (b):

| Tami Tyler's Creations Inc

Income Statement (Contribution Format) under Variable Costing | |

| Quarter 2 | |

| Sales | $1,280,000 |

| Cost of Goods Sold | $ 528,000 |

| Variable selling and administrative expenses | $ 192,000 |

| Contribution Margin | $ 560,000 |

| Fixed Expenses (Manufacturing + Selling) | $ 500,000 |

| Net Operating Income | $ 60,000 |

Explanation:

Formula:

Opening Stock = 2000 units

Working Notes:

| Quarter 1 | Quarter 2 | ||

| Sales Quantity | 28000 | 32000 | (as given in question) |

| Production Quantity | 30000 | 30000 | (as given in question) |

| Opening Stock | 0 | 2000 | (Closing Stock of previous year) |

| Closing Stock | 2000 | 0 | (Opening Stock + Production - Sales) |

| Selling Price per unit | 40 | 40 | (Sales Value $ 1,120,000/ 28,000 units) |

| Fixed Manufacturing Cost | 300000 | 300000 | |

| Fixed Manufacturing Cost per unit | 10 | 10 | (Fixed manufacturing cost / Production Qty) |

| Variable Selling cost per unit | 6 | 6 | (as given in question) |

| Fixed Selling Expenses | 200000 | 200000 | (as given in question) |

| Unit Product Cost under Variable Costing | Quarter 1 | Quarter 2 | |

| Direct Material | 3.5 | 3.5 | |

| Direct Labour | 12 | 12 | |

| Variable Manufacturing Overhead | 1 | 1 | |

| 16.5 | 16.5 |

Explanation of Solution

Formula:

Opening Stock = 2000 units

Working Notes:

| Quarter 1 | Quarter 2 | ||

| Sales Quantity | 28000 | 32000 | (as given in question) |

| Production Quantity | 30000 | 30000 | (as given in question) |

| Opening Stock | 0 | 2000 | (Closing Stock of previous year) |

| Closing Stock | 2000 | 0 | (Opening Stock + Production - Sales) |

| Selling Price per unit | 40 | 40 | (Sales Value $ 1,120,000/ 28,000 units) |

| Fixed Manufacturing Cost | 300000 | 300000 | |

| Fixed Manufacturing Cost per unit | 10 | 10 | (Fixed manufacturing cost / Production Qty) |

| Variable Selling cost per unit | 6 | 6 | (as given in question) |

| Fixed Selling Expenses | 200000 | 200000 | (as given in question) |

| Unit Product Cost under Variable Costing | Quarter 1 | Quarter 2 | |

| Direct Material | 3.5 | 3.5 | |

| Direct Labour | 12 | 12 | |

| Variable Manufacturing Overhead | 1 | 1 | |

| 16.5 | 16.5 |

Under Variable costing, the inventory is valued at Unit product cost as per variable costing method which is direct material plus direct labour plus variable manufacturing expenses whereas under Absorption costing, the inventory is valued at Unit product cost as per absorption costing method which is direct material plus direct labour plus variable manufacturing expenses plus fixed cost per unit.

Due to the inclusion of fixed cost in inventory in absorption costing, following is the impact:

- Opening inventory is higher resulting in decrease in profit

- Closing inventory is higher resulting in increase in profit

Reconciliation between Variable costing and Absorption Costing

Answer to Problem 23P

Solution:

| Reconciliation | |

| Quarter 1 | |

| Net Operating Income as per Variable Costing | $ 60,000 |

| Closing Stock | - |

| Opening Stock | 2,000 |

| Difference in Stock (Closing - Opening) | (2,000) |

| Fixed Overhead per unit | $ 10 |

| Fixed Overhead on Difference Stock | (20,000) |

| Profit as per Absorption Costing | $ 40,000 |

Explanation of Solution

Reconciliation is done between Net Operating Income as per Variable Costing and that as per Absorption Costing.

The difference between the two net operating income figures would be on account of fixed cost element on inventory.

- Net operating income under variable costing is taken as a base;

- Difference of stock quantity is computed as closing stock less opening stock

- This difference in stock is multiplied with fixed overhead per unit (as computed in Unit product cost). This will the amount of fixed overhead which has been deferred over to the next period;

- Adding this fixed overhead amount to Net Operating Income as per Variable Costing will give Net Operating Income as per Absorption Costing.

- Given

Opening stock is calculated as 2,000 units from previous solutions.

Closing stock is available as Nil

- Formula

Under Variable costing, the inventory is valued at Unit product cost as per variable costing method which is direct material plus direct labour plus variable manufacturing expenses whereas under Absorption costing, the inventory is valued at Unit product cost as per absorption costing method which is direct material plus direct labour plus variable manufacturing expenses plus fixed cost per unit.

Due to the inclusion of fixed cost in inventory in absorption costing, following is the impact:

- Opening inventory is higher resulting in decrease in profit

- Closing inventory is higher resulting in increase in profit

Want to see more full solutions like this?

Chapter 7 Solutions

Introduction To Managerial Accounting

- Variable-Costing and Absorption-Costing Income Borques Company produces and sells wooden pallets that are used for moving and stacking materials. The operating costs for the past year were as follows: During the year, Borques produced 200,000 wooden pallets and sold 204,300 at 9 each. Borques had 8,200 pallets in beginning finished goods inventory; costs have not changed from last year to this year. An actual costing system is used for product costing. Required: 1. What is the per-unit inventory cost that is acceptable for reporting on Borquess balance sheet at the end of the year ? How many units are in ending inventory? What is the total cost of ending inventory? 2. Calculate absorption-costing operating income. 3. CONCEPTUAL CONNECTION What would the per-unit inventory cost be under variable costing? Does this differ from the unit cost computed in Requirement 1? Why? 4. Calculate variable-costing operating income. 5. Suppose that Borques Company had sold 196,700 pallets during the year. What would absorption-costing operating income have been? Variable-costing operating income?arrow_forwardEstimated income statements, using absorption and variable costing Prior to the first month of operations ending October 31, Marshall Inc. estimated the following operating results: The company is evaluating a proposal to manufacture 50,000 units instead of 40,000 units, thus creating an ending inventory of 10,000 units. Manufacturing the additional units will not change sales, unit variable factory overhead costs, total fixed factory overhead cost, or total selling and administrative expenses. a. Prepare an estimated income statement, comparing operating results if 40,000 and 50,000 units are manufactured in (1) the absorption costing format and (2) the variable costing format. b. What is the reason for the difference in operating income reported for the two levels of production by the absorption costing income statement?arrow_forwardCost Classification, Income Statement Gateway Construction Company, run by Jack Gateway, employs 25 to 30 people as subcontractors for laying gas, water, and sewage pipelines. Most of Gateways work comes from contracts with city and state agencies in Nebraska. The companys sales volume averages 3 million, and profits vary between 0 and 10% of sales. Sales and profits have been somewhat below average for the past 3 years due to a recession and intense competition. Because of this competition, Jack constantly reviews the prices that other companies bid for jobs. When a bid is lost, he analyzes the reasons for the differences between his bid and that of his competitors and uses this information to increase the competitiveness of future bids. Jack believes that Gateways current accounting system is deficient. Currently, all expenses are simply deducted from revenues to arrive at operating income. No effort is made to distinguish among the costs of laying pipe, obtaining contracts, and administering the company. Yet all bids are based on the costs of laying pipe. With these thoughts in mind, Jack looked more carefully at the income statement for the previous year (see below). First, he noted that jobs were priced on the basis of equipment hours, with an average price of 165 per equipment hour. However, when it came to classifying and assigning costs, he needed some help. One thing that really puzzled him was how to classify his own 114,000 salary. About half of his time was spent in bidding and securing contracts, and the other half was spent in general administrative matters. Required: 1. Classify the costs in the income statement as (1) costs of laying pipe (production costs), (2) costs of securing contracts (selling costs), or (3) costs of general administration. For production costs, identify direct materials, direct labor, and overhead costs. The company never has significant work in process (most jobs are started and completed within a day). 2. Assume that a significant driver is equipment hours. Identify the expenses that would likely be traced to jobs using this driver. Explain why you feel these costs are traceable using equipment hours. What is the cost per equipment hour for these traceable costs?arrow_forward

- Inventory effects under absorption costing BendOR, Inc., manufactures control panels for the electronics industry and has just completed its first year of operations. The following discussion took place between the controller, Gordon Merrick, and the company president, Matt McCray: Matt: Ive been looking over our first years performance by quarters. Our earnings have been increasing each quarter, even though our sales have been flat and our prices and costs have not changed. Why is this? Gordon: Our actual sales have stayed even throughout the year, but weve been increasing the utilization of our factory every quarter. By keeping our factory utilization high, we will keep our costs down by allocating the fixed plant costs over a greater number of units. Naturally, this causes our cost per unit to be lower than it would be otherwise. Matt: Yes, but what good is this if we are unable to sell everything that we make? Our inventory is also increasing. Gordon: This is true. However, our unit costs are lower because of the additional production. When these lower costs are matched against sales, it has a positive impact on our earnings. Matt: Are you saying that we are able to create additional earnings merely by building inventory? Can this be true? Gordon: Well, Ive never thought about it quite that way. . . but I guess so. Matt: And another thing. What will happen if we begin to reduce our production in order to liquidate the inventory? Dont tell me our earnings will go down even though our production effort drops! Gordon: Well. . . Matt: There must be a better way. Id like our quarterly income statements to reflect whats really going on. I dont want our income reports to reward building inventory and penalize reducing inventory. Gordon: Im not sure what I can dowe have to follow generally accepted accounting principles. In teams: a. Discuss why reporting income under generally accepted accounting principles rewards building inventory and penalizes reducing inventory. b. Discuss what advice you would give to Gordon in responding to Matts concern about the present method of accounting. Be prepared to discuss your answers in class.arrow_forwardCVP analysis—effects of changes in cost structure; breakeven Riveria Co.makes and sells a single product. The current selling price is $32 per unit. Variable expenses are $20 per unit, and fixed expenses total $43,200 per month. Sales volume for May totaled 4,100 units.Required:a. Calculate operating income for May.b. Calculate the break-even point in terms of units sold and total revenues.c. Management is considering installing automated equipment to reduce direct labor cost. If this were done, variable expenses would drop to $14 per unit, but fixed expenses would increase to $67,800 per month.1. Calculate operating income at a volume of 4,100 units per month with the new cost structure.2. Calculate the break-even point in units with the new cost structure. (Round your answer.)3. Why would you suggest that management seriously consider investing in the automated equipment and accept the new cost structure?4. Why might management not accept your recommendation but decide instead to…arrow_forwardActivity-Based Management, Non-Value-Added Costs, Target Costs, Kaizen Costing Joseph Hansen, president of Electronica, Inc., was concerned about the end-of-the-year marketing report that he had just received. According to Asha Kumar, marketing manager, a price decrease for the coming year was again needed to maintain the company's annual sales volume of integrated circuit boards (CBs). This would make a bad situation worse. The current selling price of $27 per unit was producing a $3-per-unit profit—half the customary $6-per-unit profit. Foreign competitors keep reducing their prices. To match the latest reduction would reduce the price from $27 to $21. This would put the price below the cost to produce and sell it. How could the foreign firms sell for such a low price? Determined to find out if there were problems with the company's operations, Joseph decided to hire Ahmed Kumar, a well-known consultant and brother of Asha, who specializes in methods of continuous improvement. Ahmed…arrow_forward

- Activity-Based Management, Nonvalue-Added CostsDanna Martin, president of Mays Electronics, was concerned about the end-of-the year marketingreport that she had just received. According to Larry Savage, marketing manager, a price decreasefor the coming year was again needed to maintain the company’s annual sales volume of integratedcircuit boards (CBs). This would make a bad situation worse. The current selling price of $18 perunit was producing a $2-per-unit profit—half the customary $4-per-unit profit. Foreign competitors kept reducing their prices. To match the latest reduction would reduce the price from $18 to$14. This would put the price below the cost to produce and sell it. How could these firms sell forsuch a low price? Determined to find out if there were problems with the company’s operations,Danna decided to hire a consultant to evaluate the way in which the CBs were produced and sold.After two weeks, the consultant had identified the following activities and costs:Setting…arrow_forwardPlease help me thouroughluy answer this question. Please include calculaions and how you got to the answer. Thank you! Case 7-65. Cost-Volume-Profit with Multiple Products, Sales Mix Changes, Changes in Fixed and Variable CostsObjective 1, 4 Artistic Woodcrafting Inc. began several years ago as a one-person, cabinet-making operation. Employees were added as the business expanded. Last year, sales volume totaled $850,000. Volume for the first five months of the current year totaled $600,000, and sales were expected to be $1.6 million for the entire year. Unfortunately, the cabinet business in the region where Artistic is located is highly competitive. More than 200 cabinet shops are all competing for the same business. Artistic currently offers two different quality grades of cabinets: Grade I and Grade II, with Grade I being the higher quality. The average unit selling prices, unit variable costs, and direct fixed costs are as follows: Unit Price Unit Variable Cost Direct Fixed…arrow_forwardCase 1 Name: Madison Gladney Cost Formulas, Single and Multiple Cost Drivers For the past 5 years, Garner Company has had a policy of producing to meet customer demand. As a result, finished goods inventory is minimal, and for the most part, units produced equal units sold. Recently, Garner's industry entered a recession, and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that at least cover its variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Toward that end, the president of Garner Company implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. To help implement the policy, Garner's controller developed the following cost formulas: Direct…arrow_forward

- 1.Weston Corporation manufactures a product that is available in both a deluxe and a regularmodel. The company has made the regular model for years; the deluxe model was introducedseveral years ago to tap a new segment of the market. Since introduction of the deluxe model, thecompany’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly.Overhead is applied to products on the basis of direct labor-hours. At the beginning of the currentyear, management estimated that $3,080,000 in overhead costs would be incurred and thecompany would produce and sell 10,000 units of the deluxe model and 50,000 units of the regularmodel. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular modelrequires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct materials cost per unit $50.00 $30.00 Direct labor cost per unit $30.00 $15.00 Required:a. Compute the predetermined…arrow_forward1.Weston Corporation manufactures a product that is available in both a deluxe and a regularmodel. The company has made the regular model for years; the deluxe model was introducedseveral years ago to tap a new segment of the market. Since introduction of the deluxe model, thecompany’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly.Overhead is applied to products on the basis of direct labor-hours. At the beginning of the currentyear, management estimated that $3,080,000 in overhead costs would be incurred and thecompany would produce and sell 10,000 units of the deluxe model and 50,000 units of the regularmodel. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular modelrequires 1.0 hours. Materials and labor costs per unit are given below: Deluxe Regular Direct materials cost per unit $50.00 $30.00 Direct labor cost per unit $30.00 $15.00 These cost pools and their associated…arrow_forward1. Weston Corporation manufactures a product that is available in both a deluxe and a regularmodel. The company has made the regular model for years; the deluxe model was introducedseveral years ago to tap a new segment of the market. Since introduction of the deluxe model, thecompany’s profits have steadily declined. Sales of the deluxe model have been increasing rapidly.Overhead is applied to products on the basis of direct labor-hours. At the beginning of the currentyear, management estimated that $3,080,000 in overhead costs would be incurred and the company would produce and sell 10,000 units of the deluxe model and 50,000 units of the regularmodel. The deluxe model requires 2.0 hours of direct labor time per unit, and the regular modelrequires 1.0 hours. Materials and labor costs per unit are given below:Deluxe RegularDirect materials cost per unit $50.00 $30.00Direct labor cost per unit $30.00 $15.00Required:a. Compute the predetermined overhead rate using direct labor-hours as…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,