Videos

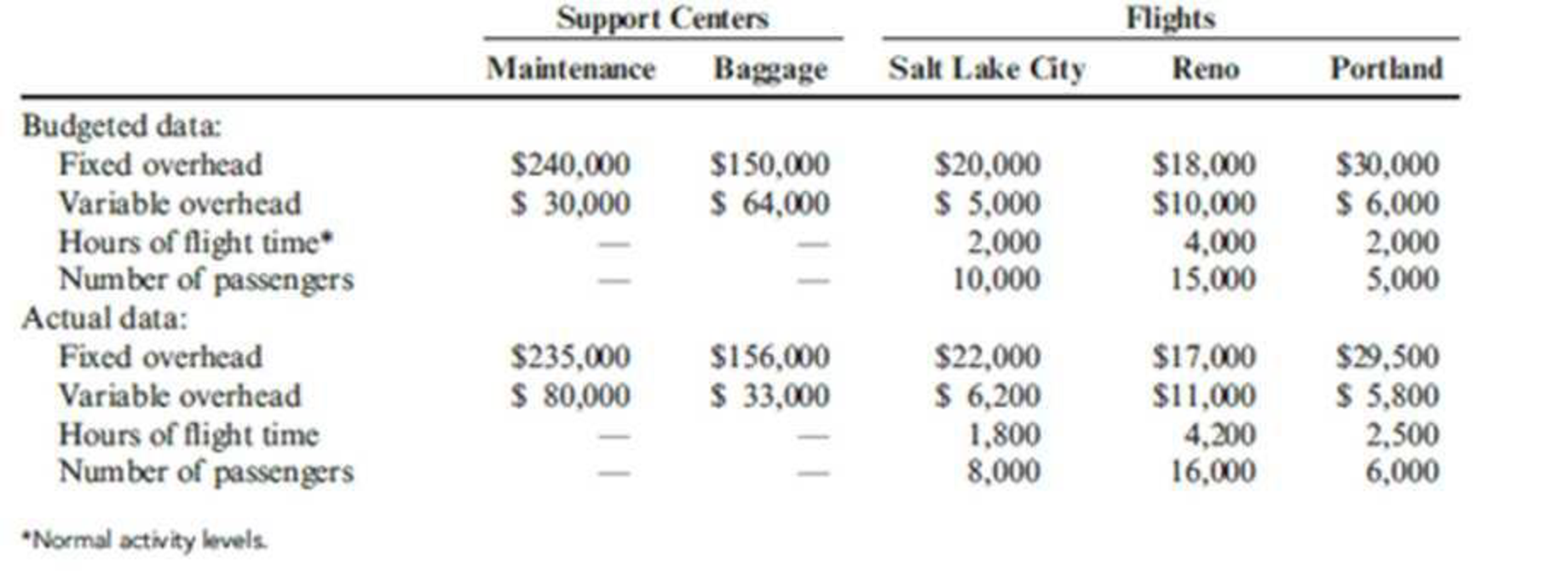

AirBorne is a small airline operating out of Boise, Idaho. Its three flights travel to Salt Lake City, Reno, and Portland. The owner of the airline wants to assess the full cost of operating each flight. As part of this assessment, the costs of two support departments (maintenance and baggage) must be allocated to the three flights. The two support departments that support all three flights are located in Boise (any maintenance or baggage costs at the destination airports are directly traceable to the individual flights). Budgeted and actual data for the year are as follows for the support departments and the three flights:

Round all allocation ratios and variable rates to four significant digits. Round all allocated amounts to the nearest dollar.

Required:

- 1. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to determine the cost of operating each flight.

- 2. Using the direct method, allocate the support service costs to each flight, assuming that the objective is to evaluate performance. Do any costs remain in the two support departments after the allocation? If so, how much? Explain.

Trending nowThis is a popular solution!

Chapter 7 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- The Blair Company’s three assembly plants are located in California, Georgia, and New Jersey. Previously, the company purchased a major subassembly, which becomes part of the final product, from an outside firm. Blair has decided to manufacture the subassemblies within the company and must now consider whether to rent one centrally located facility (e.g., in Missouri, where all the subassemblies would be manufactured) or to rent three separate facilities, each located near one of the assembly plants, where each facility would manufacture only the subassemblies needed for the nearby assembly plant. A single, centrally located facility, with a production capacity of 18,000 units per year, would have fixed costs of $900,000 per year and a variable cost of $250 per unit. Three separate decentralized facilities, with production capacities of 8,000, 6,000, and 4,000 units per year, would have fixed costs of $475,000, $425,000, and $400,000, respectively, and variable costs per unit of only…arrow_forwardBradbo owned two adjoining restaurants, the Pork Palace and the Chicken Hut. Each restaurant was treated as a profit center for performance evaluation purposes. Although the restaurants had separate kitchens, they shared a central baking facility. The principal costs of the baking area included materials, supplies, labor, and depreciation and maintenance on the equipment. Bradbo allocated the monthly costs of the baking facility to the two restaurants based on the number of tables served in each restaurant during the month using dual allocation and equal sharing of fixed costs. In April, the costs were $39,000, of which $20,500 were fixed. The Pork Palace served 3,830 tables, while the Chicken Hut served 5,745 tables. 1. The amount of the joint cost that should have been allocated to the Chicken Hut in April is calculated to be 2. The amount of joint cost that should have been allocated to the Pork Palace in April is calculated to bearrow_forwardSyracuse Beverages Inc. has three plants that make and bottle cola, lemon-lime, and miscellaneous flavored beverages, respectively. The raw materials, labor costs, and automated technology are comparable among the three plants. Top management has initiated an incentive compensation plan whereby the workers and managers of the plant with the lowest unit cost per bottle will receive a year-end bonus. The results, approved by the plant manager and reported by the plant controllers at each location, were as follows ITEM DEWITT FAYETTEVILLE MANLIUS Materials 200,000 450,000 325,000 Labor 170,000 375,000 250,000 Overhead 340,000 750,000 500,000 TOTAL 710,000 1575,000 1075,000 Equivalents Units of Production Completed 3500,000 6200,000 6450,000 Ending Work in process 100,000(50% complete) 400,000(25% complete Equivalent units 3550,000 6300,000 6450,000 Unit Cost $0.20 $0.25 $0.167 When provided copies of the results as a justification for distributing the…arrow_forward

- Solomon Condos Corporation is a small company owned by Dennis Hatch. It leases three condos of differing sizes to customers as vacation facilities. Labor costs for each condo consist of maid service and maintenance cost. Other direct operating costs consist of interest and depreciation. The direct operating costs for each condo follow. Direct Labor Other Direct Operating Costs Condo 1 $ 17,300 $ 39,800 Condo 2 18,300 43,000 Condo 3 28,500 62,500 Total $ 64,100 $ 145,300 Indirect operating expenses, which amounted to $43,590, are allocated to the condos in proportion to the amount of other direct operating costs incurred for each. Required Assuming that the amount of rent revenue from Condo 2 is $100,000, what amount of income did it earn? Note: Do not round intermediate calculations.arrow_forwardBasuras Waste Disposal Company has a long-term contract with several large cities to collect garbage and trash from residential customers. To facilitate the collection, Basuras places a large plastic container with each household. Because of wear and tear, growth, and other factors, Basuras places about 200,000 new containers each year (about 20% of the total households). Several years ago, Basuras decided to manufacture its own containers as a cost-saving measure. A strategically located plant involved in this type of manufacturing was acquired. To help ensure cost efficiency, a standard cost system was installed in the plant. The following standards have been established for the products variable inputs: During the first week in January, Basuras had the following actual results: The purchasing agent located a new source of slightly higher-quality plastic, and this material was used during the first week in January. Also, a new manufacturing process was implemented on a trial basis. The new process required a slightly higher level of skilled labor. The higher- quality material has no effect on labor utilization. However, the new manufacturing process was expected to reduce materials usage by 0.25 pound per container. Required: 1. CONCEPTUAL CONNECTION Compute the materials price and usage variances. Assume that the 0.25 pound per container reduction of materials occurred as expected and that the remaining effects are all attributable to the higher-quality material. Would you recommend that the purchasing agent continue to buy this quality, or should the usual quality be purchased? Assume that the quality of the end product is not affected significantly. 2. CONCEPTUAL CONNECTION Compute the labor rate and efficiency variances. Assuming that the labor variances are attributable to the new manufacturing process, should it be continued or discontinued? In answering, consider the new processs materials reduction effect as well. Explain. 3. CONCEPTUAL CONNECTION Refer to Requirement 2. Suppose that the industrial engineer argued that the new process should not be evaluated after only one week. His reasoning was that it would take at least a week for the workers to become efficient with the new approach. Suppose that the production is the same the second week and that the actual labor hours were 9,000 and the labor cost was 99,000. Should the new process be adopted? Assume the variances are attributable to the new process. Assuming production of 6,000 units per week, what would be the projected annual savings? (Include the materials reduction effect.)arrow_forwardCarrie Construction (CC) is a company specializing in building airport runways and major highways. As a part of its business, it receives supplies of aggregate (stone, sand, gravel, and so on) from two suppliers: Austin Aggregate and Granger Materials. The CC purchasing department has a preference for buying from Granger based on price but occasionally has to order from Austin when Granger cannot fill the order. Carrie Construction has recently had problems with the quality and the timeliness of deliveries. When a supplier delivers a load to CC, it goes through an initial inspection to assure it meets specification. If the load fails the initial inspection, it goes through a secondary inspection to determine the exact issue. Almost always, the issue can be resolved and the load can be used. The initial inspection costs $3,240 per load. A secondary inspection, which is more thorough, costs $16,200 per load. If a delivery is delayed, Carrie has to hire temporary workers or pay overtime…arrow_forward

- A large, downtown hotel allocated all of its restaurant labor costs on the basis of revenue dollars. This hotel had seven restaurant outlets that were vastly different, including banquet, room service, a bar, a 24-hour restaurant, and a fine dining facility. There are obvious differences in the way labor resources are consumed in these various outlets. However, the most glaring example was in the banquet operation. Since banquets were not regularly scheduled events, the banquet manager hired servers as contract laborers. These costs were not included in the restaurant labor pool. Suggest at least two steps the manager should take to ensure that all labor is factored into the profitability analysis. What level of variances should we apply level 1, 2 or 3. Suggest the variance analysis that would pinpoint the issue with the budget. Provide specific examples.arrow_forwardA large, downtown hotel allocated all of its restaurant labor costs on the basis of revenue dollars. This hotel had seven restaurant outlets that were vastly different, including banquet, room service, a bar, a 24-hour restaurant, and a fine dining facility. There are obvious differences in the way labor resources are consumed in these various outlets. However, the most glaring example was in the banquet operation. Since banquets were not regularly scheduled events, the banquet manager hired servers as contract laborers. These costs were not included in the restaurant labor pool. Suggest at least two steps the manager should take to ensure that all labor is factored into the profitability analysis. Suggest the variance analysis that would pinpoint the issue with the budget. Provide specific examples.arrow_forwardGordon Grimes, a self-employed consultant near Atlanta, received an invitation to visit a prospective client in Seattle. A few days later, he received an invitation to make a presentation to a prospective client in Denver. He decided to combine his visits, traveling from Atlanta to Seattle, Seattle to Denver, and Denver to Atlanta. Grimes received offers for his consulting services from both companies. Upon his return, he decided to accept the engagement in Denver. He is puzzled over how to allocate his travel costs between the two clients. He has collected the following data for regular round-trip fares with no stopovers: Atlanta to Seattle = $600 Atlanta to Denver = $400 Grimes paid $900 for his three-leg flight (Atlanta–Seattle, Seattle–Denver, Denver–Atlanta). In addition, he paid $45 each way ($90 total) for limousines from his home to Atlanta Airport and back when he returned. Q. How should Grimes allocate the $900 airfare between the clients in Seattle and Denver. Which method…arrow_forward

- Gordon Grimes, a self-employed consultant near Atlanta, received an invitation to visit a prospective client in Seattle. A few days later, he received an invitation to make a presentation to a prospective client in Denver. He decided to combine his visits, traveling from Atlanta to Seattle, Seattle to Denver, and Denver to Atlanta. Grimes received offers for his consulting services from both companies. Upon his return, he decided to accept the engagement in Denver. He is puzzled over how to allocate his travel costs between the two clients. He has collected the following data for regular round-trip fares with no stopovers: Atlanta to Seattle = $600 Atlanta to Denver = $400 Grimes paid $900 for his three-leg flight (Atlanta–Seattle, Seattle–Denver, Denver–Atlanta). In addition, he paid $45 each way ($90 total) for limousines from his home to Atlanta Airport and back when he returned. Q. How should Grimes allocate the $90 limousine charges between the clients in Seattle and Denver?arrow_forwardGordon Grimes, a self-employed consultant near Atlanta, received an invitation to visit a prospective client in Seattle. A few days later, he received an invitation to make a presentation to a prospective client in Denver. He decided to combine his visits, traveling from Atlanta to Seattle, Seattle to Denver, and Denver to Atlanta. Grimes received offers for his consulting services from both companies. Upon his return, he decided to accept the engagement in Denver. He is puzzled over how to allocate his travel costs between the two clients. He has collected the following data for regular round-trip fares with no stopovers: Atlanta to Seattle = $600 Atlanta to Denver = $400 Grimes paid $900 for his three-leg flight (Atlanta–Seattle, Seattle–Denver, Denver–Atlanta). In addition, he paid $45 each way ($90 total) for limousines from his home to Atlanta Airport and back when he returned. Q. How should Grimes allocate the $900 airfare between the clients in Seattle and Denver using (a) the…arrow_forwardKia Corporation has two departments, A and B. Central costs could be allocated to the two departments in various ways. Square footage of department A and B 6,000 and 18,000 square feet respectively, Number of employees of department A and B 1,500 and 500 respectively, and sales of department A and B $400,000 and $2,000,000 respectively. If total processing costs of $96,000 are allocated on the basis of number of employees, the amount allocated to Department B would be: a. $24,000 b. $28,800 c. $16,000 d. $67,200arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning