Concept explainers

a.

1.

To explain: The reason for Treasury bill’s return is independent of the state of the economy and whether treasury bills give a completely risk-free return.

Risk and Return:

The risk and return are two closely related terms. The risk is the uncertainty attached to an event. In case of any investment, there is some amount of risk attached to it as there can be either gain or loss. While return in the financial term is that percentage which represents the profit in an investment. Higher risk is related to higher return and lower risk has a probability of lower return. The investor has to face a tradeoff between risk and return in terms of an investment.

Treasury bills:

The treasury bills are those short-term bonds or securities which have maturity period of less than one year. These are issued by the government for a shorter period and when the government needs to raise funds immediately.

a.

1.

Answer to Problem 23IC

- The 5.5% Treasury bill does not depend on the state of the economy because the treasury must and will redeem the bills at par apart from the state of the economy.

- The treasury bills are risk-free return completely as the 5.5% return will be realized in all the possible economic states.

- The treasury bills cannot give a completely risk-free return as a security cannot be totally risk-free.

- Only the tax-exempt bonds or the inflation-indexed bonds would be riskless.

Explanation of Solution

- The treasury bills are the return which is composed of real risk-free rate, in which 5.5% is risk-free rate.

- There is uncertainty about inflation, so it is not possible that the expected realized

rate of return would be 5.5%. - If the average of the inflation is 6% over the year, then the realized rate of return will be 4.5%, not the expected 5.5%.

- In terms of the

purchasing power , the Treasury-bills are riskless. - When the rates decline after an investment in a portfolio of treasury bills, the nominal income would also fall.

- The treasury bills are exposed to reinvestment rate risk.

Thus, the Treasury-bills will not depend on the state of the economy as the treasury bills must and will redeem at par. All securities are exposed to some type of risk, so treasury bills cannot give a completely risk-free return.

2.

To explain: The reason for H’s returns expected to move with the economy and C’s returns expected to move counter to the economy.

2.

Answer to Problem 23IC

- The H’s returns are positively correlated with the economy, as the sales of the firm and its profits will experience the same kind of fluctuations as will the economy.

- The C Company is considered by many investors as a hedge against both bad times and high inflation, so in case the stock crashes the investors will do relatively well.

Explanation of Solution

- There are two kinds of correlation one is positive correlation and other is a negative correlation.

- When return is correlated positively, they will move with the economy and when they are correlated negatively, they move counter the economy.

Thus, as H’s return is positively correlated, it will move with the economy and as C’s returns are negatively correlated, it will move counter the economy.

b.

To determine: The expected rate of return for each alternative.

The Expected Return on the Stock:

The expected return on stock refers to the weighted average of expected

b.

Explanation of Solution

The formula to calculate the expected rate of return:

Where,

- N is the number of states.

Calculate the expected rate of return for H.

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the probability and (27%), (7%), 15%, 30% and 45% for rates,

The expected rate of return is 12.4%.

Calculate the expected rate of return for T-bills.

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the probability and 5.5% for all rates,

The expected rate of return is 5.5%.

The value filled in the table is as:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 5.5% | (27%) | 27% | 6.0% | (17%) | (0.0%) |

| Below average | 0.2 | 5.5% | (7%) | 13% | (14%) | (3%) | |

| Average | 0.4 | 5.5% | 15% | (11)% | 3% | 10% | 7.5% |

| Above average | 0.2 | 5.5% | 30% | (21%) | 41% | 25% | |

| Boom | 0.1 | 5.5% | 45% | (20.0%) | 26% | 38% | 12% |

|

|

5.5% | 12.4% | 1.0% | 9.8% | 10.5% | ||

|

|

0.0 | 13.2 | 18.8 | 15.2 | 3.4 | ||

| CV | 13.2 | 1.9 | 1.4 | 0.5 | |||

| b | -0.87 | 0.88 |

Table (1)

Thus, the expected rate of return for H and T-bills is 12.4% and 5.5%.

c.

1.

To determine: The standard deviation of returns.

Standard Deviation:

The standard deviation refers to the stand-alone risk associated with the securities. It measures how much a data is dispersed with its standard value. The Greek letter sigma represents the standard deviation.

c.

1.

Explanation of Solution

The formula to calculate the standard deviation:

Where,

- N is the number of states.

Calculation of standard deviation for H,

The standard deviation for H is 20.036%.

The value of

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 5.5% | (27%) | 27% | 6.0% | (17%) | (0.0%) |

| Below average | 0.2 | 5.5% | (7%) | 13% | (14%) | (3%) | |

| Average | 0.4 | 5.5% | 15% | (11)% | 3% | 10% | 7.5% |

| Above average | 0.2 | 5.5% | 30% | (21%) | 41% | 25% | |

| Boom | 0.1 | 5.5% | 45% | (20.0%) | 26% | 38% | 12% |

|

|

5.5% | 12.4% | 1.0% | 9.8% | 10.5% | ||

|

|

0.0 | 20.036% | 13.2 | 18.8 | 15.2 | 3.4 | |

| CV | 13.2 | 1.9 | 1.4 | 0.5 | |||

| b | -0.87 | 0.88 |

Table (2)

The standard deviation for H is 20.036%.

2.

To explain: The type of risk measured by the standard deviation.

2.

Answer to Problem 23IC

The stand-alone risk of a portfolio is measured by the standard deviation.

Explanation of Solution

- The standard deviation is a measure of the risk of a security.

- The larger is the standard deviation, the higher is the probability that actual returns will be below the expected return.

- It also shows that there will be losses rather than profits.

Thus, the stand-alone risk is measured by the standard deviation.

3.

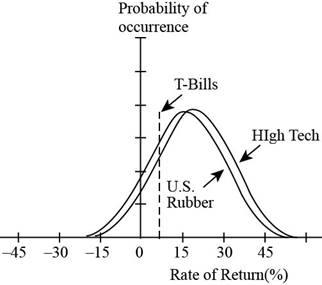

To prepare: A graph showing the probability distribution for H, U, and T.

3.

Answer to Problem 23IC

The graph showing the probability distribution is:

Fig (1)

Explanation of Solution

- The graph shows the probability distribution for the given companies.

- The X-axis shows the rate of return in percentage.

- The Y-axis shows the occurrence.

- On the basis of the graph, the H is the riskiest investment.

- The T has the less risky investment.

Thus, the graph for a probability distribution is as mentioned above and according to the graph, H is the riskiest investment andT is the least risky investment.

d.

To determine: The missing values of coefficient of variation and comparison of risk rankings of the coefficient of variation with the standard deviation.

The Coefficient of Variation:

The coefficient of variation is a tool to determine the risk. It determines the risk per unit of return. It is used for measurement when the expected returns are same for two data.

d.

Explanation of Solution

Given,

For T-bills,

The standard deviation is 0.0%.

The expected rate of return is 5.5%.

For H,

The standard deviation is 20.036%.

The expected rate of return is 12.4%.

The formula to calculate the coefficient of variation is,

Calculate coefficient of variation for T-bills.

Substitute 0.0% for the standard deviation and 5.5% for the expected rate of return in the above formula.

The coefficient of variation for T-bills is 0.0.

Calculate coefficient of variation for H.

Substitute 20.036% for the standard deviation and 12.4% for the expected rate of return in the above formula.

The coefficient of variation for H is 1.61.

The table with the missing values is as:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 5.5% | (27%) | 27% | 6.0% | (17%) | (0.0%) |

| Below average | 0.2 | 5.5% | (7%) | 13% | (14%) | (3%) | |

| Average | 0.4 | 5.5% | 15% | (11)% | 3% | 10% | 7.5% |

| Above average | 0.2 | 5.5% | 30% | (21%) | 41% | 25% | |

| Boom | 0.1 | 5.5% | 45% | (20.0%) | 26% | 38% | 12% |

|

|

5.5% | 12.4% | 1.0% | 9.8% | 10.5% | ||

|

|

0.0 | 20.036% | 13.2 | 18.8 | 15.2 | 3.4 | |

| CV | 0.0 | 1.61 | 13.2 | 1.9 | 1.4 | 0.5 | |

| b | -0.87 | 0.88 |

Table (3)

The coefficient of variation for T-bills is 0.0 and for H is 1.61.

e.

1.

The Expected Return on the Stock:

The expected return on stock refers to the weighted average of expected returns on those assets which are held in the portfolio.

Standard Deviation:

The standard deviation refers to the stand-alone risk associated with the securities. It measures how much a data is dispersed with its standard value. The Greek letter sigma represents the standard deviation.

The Coefficient of Variation:

The coefficient of variation is a tool to determine the risk. It determines the risk per unit of return. It is used for measurement when the expected returns are same for two data.

e.

1.

Explanation of Solution

Given,

A 2-stock portfolio is created.

The investment in H is $50,000.

The investment in C is $50,000.

The formula to calculate the expected rate of return:

Where,

Calculate the expected rate of return for recession,

Substitute 0.5 for the weight and 12.4% and 1.0% for the rates,

The expected rate of return is 6.7%.

Calculate the standard deviation for the 2-stock portfolio,

The formula to calculate the standard deviation:

Where,

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the different

The standard deviation is 5.93%.

Calculate the coefficient of variation for the 2-stock portfolio,

Calculated,

The expected rate of return is 6.7%.

The standard deviation is 5.93%.

The formula to calculate the coefficient of variation:

Substitute 6.7% for the standard deviation and 5.93% for the expected rate of return,

The coefficient of variation is 1.129.

The table showing the missing values is:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 5.5% | (27%) | 27% | 6.0% | (17%) | (0.0%) |

| Below average | 0.2 | 5.5% | (7%) | 13% | (14%) | (3%) | 3% |

| Average | 0.4 | 5.5% | 15% | (11)% | 3% | 10% | 7.5% |

| Above average | 0.2 | 5.5% | 30% | (21%) | 41% | 25% | 9.5% |

| Boom | 0.1 | 5.5% | 45% | (20.0%) | 26% | 38% | 12% |

|

|

5.5% | 12.4% | 1.0% | 9.8% | 10.5% | 6.7% | |

|

|

0.0 | 20.036% | 13.2 | 18.8 | 15.2 | 3.4 | |

| CV | 0.0 | 1.61 | 13.2 | 1.9 | 1.4 | 0.5 | |

| b | -0.87 | 0.88 |

Table (4)

Working note:

Calculate the portfolio returns for each state of the economy.

The formula to calculate the portfolio return:

Calculate the portfolio return for below average.

Substitute 0.5 for weights and

The portfolio return is 3%.

Calculate the portfolio return for above average.

Substitute 0.5 for weights and 30% for the rate of H and

The portfolio return is 9.5%.

The table of the economy states and their portfolio return is:

| State | Portfolio |

| Recession | (0.0%) |

| Below average | 3% |

| Average | 7.5% |

| Above average | 9.5% |

| Boom | 12% |

Table (5)

The expected rate of return, standard deviation, and coefficient of variation for the 2-stock portfolio is 6.7%, 5.93% and 1.129 respectively.

2.

To explain: The comparison of the riskiness of the 2-stock portfolios with the riskiness of the individual stock.

2.

Answer to Problem 23IC

The comparison of the riskiness of the 2-stock portfolio with the riskiness of the individual stock is explained below:

- The stand-alone risk of the portfolio is significantly less than the stand-alone risk of the individual stocks.

- The stocks are negatively correlated.

- If the stocks were held in isolation, the combination of the two stocks diversifies the inherent risks.

Explanation of Solution

- The stand-alone risk is measured by the standard deviation and coefficient of variation.

- The negative correlation of the stocks means that when one company is doing bad the other is doing well and vice-versa.

- The isolation of the stocks means that there is a one-stock portfolio.

Thus, if held in isolation, the 2-stock portfolio is less risky compared to the individual stocks.

f.

1.

To explain: The effect on riskiness and to the expected return of the portfolio.

f.

1.

Answer to Problem 23IC

Given,

The investor starts with a portfolio consisting of one randomly selected stock.

- The stocks are positively correlated with one another if the economy does well, and so is the effect on general stocks and vice-versa.

- When the additional stocks are added to the portfolio, the portfolio’s standard deviation decreases because the added stocks are not perfectly positively correlated.

- As more and more stocks are added, each new stock has a less of a risk-reducing impact, and eventually, the addition of the stocks has virtually no effect on the portfolio’s risk which is measured by the standard deviation.

Explanation of Solution

- The correlation coefficient between the stocks generally ranges in +0.35. A single stock selected at random would have a standard deviation of about 35%.

- The addition of additional shares to the portfolio decreases the standard deviation of the portfolio.

- When the combination of the stocks is made into well-diversified portfolios, the standard deviation stabilizes.

- The standard deviation stabilizes at about 21% when 40 or more randomly selected stocks are added.

Thus, the risk will reduce when the stocks are randomly added.

2.

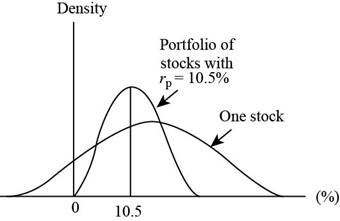

To explain: The implication for investors and the graph of the two portfolios.

2.

Answer to Problem 23IC

The graph showing the two portfolios is:

Fig (2)

The implication on the investors is that the investors should hold well-diversified portfolios of stocks rather than the individual stocks.

Explanation of Solution

- The graph represents the portfolio of one stock and the portfolio of the added stocks.

- The X-axis represents the percentage of the portfolio.

- The Y-axis represents the density of the portfolio.

- The standard deviation gets smaller as more stocks are combined in the portfolio when the return on the portfolio remains constant.

- The return on the portfolio is 10.5% and the value is constant.

- When stocks are added to the portfolio, the risk gets reduced.

Thus, the graph of the two portfolios is shown above and the implication for investors is that the investors should hold well-diversified portfolios rather than holding the individual stocks.

g.

1.

To explain: The impact of the portfolio on the thinking of the investors.

g.

1.

Answer to Problem 23IC

- The diversification of the portfolio affects the investor’s view towards risk.

- The standard deviation and coefficient of variation may be important to the undiversified investor but is not relevant to a well-diversified investor.

- A rational, risk-averse investor is more interested in the effect that the stock has on the riskiness of the portfolio than the stand-alone risk of the stock.

Explanation of Solution

- The diversification of a portfolio has a lot affect on the investor’s view of risk.

- The stand-alone risk is measured by the standard deviation and the coefficient of variation.

- The stand-alone risk is composed of diversifiable risk, which can be eliminated by holding a stock in a well-diversified portfolio.

Thus, the risk called as market risk is present when the entire market portfolio is held.

2.

To explain: The possibilities of earning a risk premium and the compensation of the risk.

2.

Answer to Problem 23IC

- When a person holds a one-stock portfolio, the person or the investor is exposed to a higher degree of risk and that risk will not be compensated.

- If the returns are high enough for the compensation of higher risk, the bargain would be more rational for the diversified investors.

- So, the possibility of earning a risk premium is not easy and the compensation will not be done for the higher risk.

Explanation of Solution

- If the returns are that high that the high risk can be compensated, that would be a bargain for a rational and more diversified investor.

- The investors would start buying the portfolio and this increase in orders would drive the price up and the return down.

Thus, it is difficult to find the stocks in the market with returns high enough to compensate for the diversifiable risk of the stock.

h.

1.

To determine: The beta coefficient and the use of beta for the risk analysis.

h.

1.

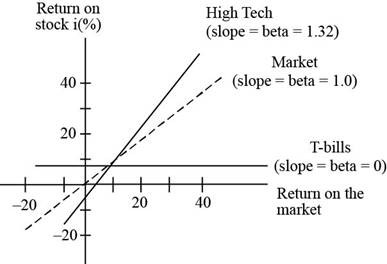

Answer to Problem 23IC

- The average beta of the stock is 1.0. Most stocks have a beta in range of 0.5 to 1.5.

- The beta value can be theoretically negative but they are generally positive in the real world.

This is shown in the graph below:

Fig (3)

Explanation of Solution

- The graph represents the calculation of the value of the beta.

- The X-axis represents the return on the market.

- The Y-axis represents the return on the stock.

- The average stock moves with the market.

- The value of the beta is calculated as the slope of the regression line which shows the relationship between the given stock and the general stock market.

- The slopes should be estimated and the slope should be used to calculate the value of beta.

Thus, the average beta of the stock would be 1.0.

2.

To explain: The relation of the expected return to each alternative market risk.

2.

Answer to Problem 23IC

- The expected returns are related to each alternative’s market risk.

- This means that higher is the alternative’s rate of return, higher is the beta.

- The treasury bills have zero risks.

Explanation of Solution

- The expected returns are the return which is expected to be earned minimum on a portfolio.

- The market risk refers to that risk which the investor can experience when the overall market performance is influenced.

- The expected returns are related to the market risk as the factors affecting the market influence the minimum return rate to be earned.

Thus, the expected returns are related to each alternative market risk.

3.

To explain: The graph showing the calculation of the beta coefficient and the measure of the betas and use of them in the risk analysis.

3.

Answer to Problem 23IC

The graph showing the calculation of the beta coefficient is:

Fig (4)

- No, it is not possible to choose among the alternatives on the basis of the information which is developed so far.

- The required rates of return are needed on these alternatives and then a comparison of them with their expected returns is needed.

Explanation of Solution

- The graph shows the calculation of the beta coefficient for the given data.

- The X-axis represents the return on the market.

- The Y-axis represents the return on the stock.

- The points are plotted on the graph for the market on a

- The points are then connected, and the slope is made.

- By the help of the slope, the value of beta is calculated as 1.0

Thus, the calculation of the beta coefficient is shown by the graph above and the required rate of return is needed to compare the alternatives with the expected return.

i.

1.

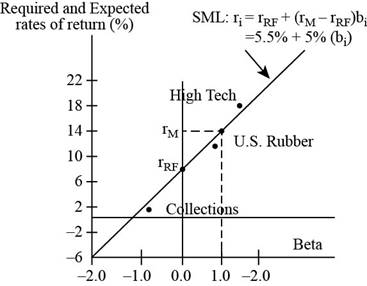

To determine: The security-market line equation, the calculation of the required rate of return on each alternative and the graph showing the relationship between the expected and required rates of return.

i.

1.

Answer to Problem 23IC

Given,

The long-term Treasury bonds have a 5.5% yield.

The assumed risk-free rate is 5.5%.

The security market line equation is,

Where,

The risk-free rate is 5.5%.

The market return rate is 10.5%.

The market risk premium is 5%

Calculate the required rate of return for H.

Substitute 5.5% for

The required rate of return is 12.1%.

Calculate the required rate of return for M.

Substitute 5.5% for

The required rate of return is 10.5%.

Calculate the required rate of return for U.

Substitute 5.5% for

The required rate of return is 9.9%.

Calculate the required rate of return for T-bills.

Substitute 5.5% for

The required rate of return is 5.5%.

Calculate the required rate of return for C.

Substitute 5.5% for

The required rate of return is 1.15%.

The graph showing the relationship between expected return and required rate of return is:

Fig (5)

Explanation of Solution

- The graph shows the relationship between the required rate and expected return.

- The X-axis shows the value of beta.

- The Y-axis shows the required and expected rates of return.

- The slope shows the security market line equation.

- The X-axis is extended to the left of zero. This shows that there is a negative beta stock and the required return is less than the risk-free rate.

Thus, the security market line equation and the graph showing the relationship is described above and the required rate of return calculated for H, M, U, T-bills, and C is 12.1%, 10.5%, 9.9%, 5.5% and 1.15%.

2.

To determine: The comparison between the expected rates of return and the required rate of return.

2.

Explanation of Solution

The relationship between the expected rate of return and the required return is shown in the following table:

| Security |

Expected return |

Required return |

Condition |

| H | 12.4% | 12.1% | Undervalued as

|

| M | 10.5% | 10.5% | Fairly valued as

|

| U | 9.8% | 9.9% | Overvalued as

|

| T-bills | 5.5% | 5.5% | Fairly valued as

|

| C | 1.0% | 1.15% | Overvalued as

|

Table (6)

Thus, the comparison is shown in the table above.

3.

To explain: The sense of the fact that C has an expected returns less than T-bills.

3.

Answer to Problem 23IC

- The C has a negative beta value which indicates that there is a negative market risk.

- The inclusion of the stock of C in a normal portfolio will lower the risk of the portfolio.

- The C has an expected return less than T-bills have a sense that the stock C will affect the normal portfolio more than T-bills.

Explanation of Solution

- The C has a stock which is very interesting.

- This stock has a negative beta.

- This means that C is a valuable security to rational, well-diversified investors.

- The example is a fire insurance policy or life insurance policy.

- These policies have a negative expected return because of commissions and insurance company profits.

- A stock having negative beta is similar to an insurance policy.

Thus, the stock C having a less expected return than T-bills makes the effect different on the stock.

4.

To determine: The market risk and the required return of a 50-50 portfolio of H and C and of H and U.

4.

Explanation of Solution

Given,

The risk-free rate is 5.5%.

The market return is 10.5%.

Calculate the required return on the 50-50 portfolio of H and C.

The formula to calculate the required rate of return is,

Where,

Substitute 5.5% for

The required rate of return is 6.625%.

Calculate the required return on the 50-50 portfolio of H and U.

The formula to calculate the required rate of return is,

Where,

Substitute 5.5% for

The required rate of return is 11%.

Working note:

Calculation of beta for 50-50 portfolio of H and C,

The value of beta is 0.225.

Calculation of beta for 50-50 portfolio of H and U,

The value of beta is 1.1.

Thus, the required return for 50-50 portfolio of H and C and for H and U is 6.625% and 11% respectively.

j.

1.

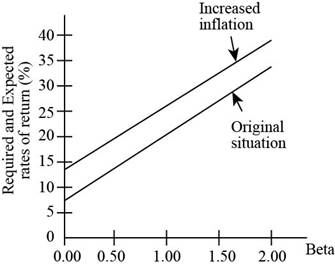

To determine: The effect of the higher inflation on the security market line and on the returns required on high and low-risk securities.

j.

1.

Answer to Problem 23IC

The graph shows the effect on the security market line:

Fig (6)

Explanation of Solution

- The graph shows the effect of higher inflation on the security market line.

- The X-axis shows the value of the beta.

- The Y-axis shows the required and expected rates of return.

- The line of the original situation is the ‘security market line’ in normal conditions.

- When the inflation is increased by 5.5% over current estimates, the ‘increased inflation line’ shows the slope of the security market line.

- The risk-free rate is 5.5% and the market return is 10.5%.

- With the increase, the risk-free rate becomes 6% and the market return becomes 11%.

- The market risk premium remains 5%.

Thus, the effect of the higher inflation is shown by the graph above and the required return will rise sharply on high-risk stocks but not much on low beta securities.

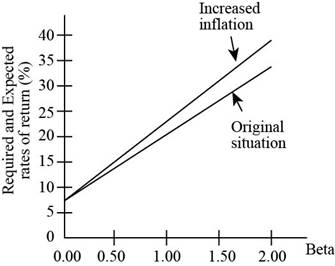

2.

To determine: The effect of the higher market risk premium on the security market line and on the returns required on high and low-risk securities.

2.

Answer to Problem 23IC

The graph shows the effect on the security market line:

Fig (7)

Explanation of Solution

- The graph shows the effect of risk aversion on the security market line.

- The X-axis shows the value of the beta.

- The Y-axis shows the required and expected rates of return.

- The line of the original situation is the ‘security market line’ in normal conditions.

- When the market risk premium is increased by 5.5% over current estimates, the ‘increased risk aversion’ line shows the slope of the security market line.

- The risk-free rate is 5.5% and the market return is 10.5%.

- With the increase, the security market line rotates upward about the Y-intercept.

- The risk-free remains constant at 5.5%.

- The market risk premium increases to 11%.

Thus, the effect of the increase in the market risk premium is shown in the graph above and the required return will rise sharply on high-risk stocks but not much on low beta securities.

Want to see more full solutions like this?

Chapter 8 Solutions

Fundamentals of Financial Management (MindTap Course List)

- Consider the following thoughts of a manager at the end of the companys third quarter: If I can increase my reported profit by 2 million, the actual earnings per share will exceed analysts expectations, and stock prices will increase. The stock options that I am holding will become more valuable. The extra income will also make me eligible to receive a significant bonus. With a son headed to college, it would be good if I could cash in some of these options to help pay his expenses. However, my vice president of finance indicates that such an increase is unlikely. The projected profit for the fourth quarter will just about meet the expected earnings per share. There may be ways, though, that I can achieve the desired outcome. First, I can instruct all divisional managers that their preventive maintenance budgets are reduced by 25 percent for the fourth quarter. That should reduce maintenance expenses by approximately 1 million. Second, I can increase the estimated life of the existing equipment, producing a reduction of depreciation by another 500,000. Third, I can reduce the salary increases for those being promoted by 50 percent. And that should easily put us over the needed increase of 2 million. Required: Comment on the ethical content of the earnings management being considered by the manager. Is there an ethical dilemma? What is the right choice for the manager to make? Is there any way to redesign the accounting reporting system to discourage the type of behavior the manager is contemplating?arrow_forwardYou are evaluating the potential purchase of a small business currently generating $ 42,500 of after-tax cashflow. On the basis of a review of similar risk investment opportunities, you must earn 15% rate of return on the proposed purchase. Because you are relatively uncertain about future cash flows, you decide to estimate the firm’s value using several assumptions about the growth rate of cash flows. What is the firm’s value if cash flows are expected to grow at an annual rate 12% for the first 2 years, followed by a constant rate of 9% from year 3 to infinity?arrow_forwardFormulate a system of equations for the situation below and solve. A private investment club has $600,000 earmarked for investment in stocks. To arrive at an acceptable overall level of risk, the stocks that management is considering have been classified into three categories: high-risk, medium-risk, and low-risk. Management estimates that high-risk stocks will have a rate of return of 15%/year; medium-risk stocks, 10%/year; and low-risk stocks, 6%/year. The members have decided that the investment in low-risk stocks should be equal to the sum of the investments in the stocks of the other two categories. Determine how much the club should invest in each type of stock if the investment goal is to have a return of $60,000/year on the total investment. (Assume that all the money available for investment is invested.) high-risk stocks$ medium-risk stocks$ low-risk stocks$arrow_forward

- Identify information used in an investment decision Look forward to the daywhen you will have accumulated $5,000, and assume that you have decided to investthat hard-earned money in the common stock of a publicly owned corporation. Whatdata about that company will you be most interested in, and how will you arrangethose data so they are most meaningful to you? What information about the company will you want on a weekly basis, on a quarterly basis, and on an annual basis?How will you decide whether to sell, hold, or buy some more of the firm’s stock?arrow_forwardYou have invested in a business that proudly reports that it is profitable. Your investment of $4000 has produced a profit of $201. The managers think that if you leave your $4500 levested with them, they should be able to generate $291 per year in profits for you in perpetuity. Evaluating other investment opportunites, you note that other long-term investments of similar risk offer an expected return of 7.9%. Should you remain invested in this fr ? The expected ratus of your envestment is__? (Round to one decimal)arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning