Concept explainers

Videos

Accounting for Accounts and Notes Receivable Transactions

Web Wizard, Inc., has provided information technology services for several years. The company uses the percentage of credit sales method to estimate

- a. During January, the company provided services for $40,000 on credit.

- b. On January 31, the company estimated bad debts using 1 percent of credit sales.

- c. On February 4, the company collected $20,000 of accounts receivable.

- d. On February 15, the company wrote off a $100 account receivable.

- e. During February, the company provided services for $30,000 on credit.

- f. On February 28, the company estimated bad debts using 1 percent of credit sales.

- g. On March 1, the company loaned $2,400 to an employee who signed a 6% note, due in 6 months.

- h. On March 15, the company collected $100 on the account written off one month earlier.

- i. On March 31, the company accrued interest earned on the note.

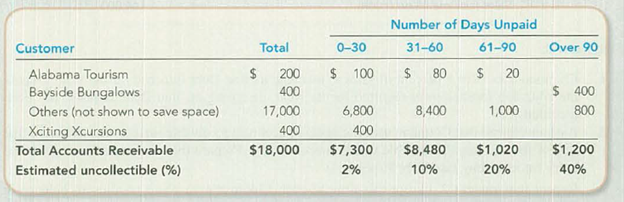

- j. On March 31, the company adjusted for uncollectible accounts, based on an aging analysis (below). Allowance for Doubtful Accounts has an unadjusted credit balance of $1,200.

Required:

- 1. For items (a)–(j), analyze the amount and direction (+ or −) of effects on specific financial statement accounts and the overall

accounting equation. - 2. Prepare

journal entries for items (a)–(j). - 3. Show how Accounts Receivable. Notes Receivable, and their related accounts would be reported in the current assets section of a classified balance sheet.

- 4. Sales Revenue and Service Revenue are two income statement accounts that relate to Accounts Receivable. Name two other accounts related to Accounts Receivable and Notes Receivable that would be reported on the income statement and indicate whether each would appear before, or after, Income from Operations.

1.

To indicate: The amount and direction of effects of each transaction from (a)-(j) on the financial statement accounts and on the overall accounting equation.

Explanation of Solution

Bad debt expense:

Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Allowance method:

It is a method for accounting bad debt expense, where amount of uncollectible accounts receivables are estimated and recorded at the end of particular period. Under this method, bad debts expenses are estimated and recorded prior to the occurrence of actual bad debt, in compliance with matching principle by using the allowance for doubtful account.

Write-off:

Write-off refers to the deduction of a certain amount from accounts receivable, when it is decided that the amount would be uncollectible forever.

Accounting equation: Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

Indicate the amount and direction of effects each transactions on the financial statement accounts and on the overall accounting equation.

a.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$40,000 | Service revenue (+R) | +$40,000 |

Table (1)

b.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$400 | Bad debt expense (+E) | –$400 |

Table (2)

Working note:

Determine the amount of bad debt expense for the year.

c.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Cash | +$20,000 | |||||

| Accounts receivable | –$20,000 |

Table (3)

d.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | –$100 | |||||

| Allowance for doubtful accounts (–xA) | +$100 |

Table (4)

e.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$30,000 | Service revenue (+R) | +30,000 |

Table (5)

f.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$300 | Bad debt expense (+E) | –$300 |

Table (6)

g.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Cash | –$2,400 | |||||

| Note receivable | +$2,400 |

Table (7)

h.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$100 | |||||

| Allowance for doubtful accounts (+xA) | –$100 | |||||

| Cash | +$100 | |||||

| Accounts receivable | –$100 |

Table (8)

i.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Interest receivable | +$12 | Interest revenue (+R) | +$12 |

Table (9)

Working note:

Calculate the amount of interest revenue earned on note, as on March 31.

j.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$478 | Bad debt expense (+E) | –$478 |

Table (10)

Working note:

Estimate the amount of uncollectible under on the basis of aging analysis method.

| Number of days unpaid | |||||

| Total | 0–30 | 31–60 | 61–90 | Over 90 | |

| Total Accounts Receivable | $ 18,000 | $7,300 | $8,480 | $1,020 | $1,200 |

| Estimated Uncollectible (%) | |||||

| Estimated Uncollectible ($) | $ 1,678 | $146 | $848 | $204 | $480 |

Table (11)

Aging of receivables method:

A method of determining the estimated uncollectible receivables based on the age of individual accounts receivable is known as aging of receivables method. Amount of accounts receivables of different age and its respective uncollectible percentage are multiplied, to determine the estimated uncollectible receivables for each age group of receivable.

It is given that the unadjusted balance of allowance for doubtful accounts is a credit balance of $1,200. It is calculated that the estimated uncollectible is $1,678. Under aging of receivables method, estimated uncollectible would be treated as desired ending balance of allowance for doubtful accounts. To bring the balance of allowance for doubtful accounts from a credit balance of $1,200 to a credit of $1,678, allowance for doubtful accounts must be adjusted (by debiting (increasing) bad debts expenses and by crediting (increasing) allowance for doubtful accounts). So, now calculate the amount needed to be adjusted for uncollectible accounts.

Calculate the amount needed to be adjusted for uncollectible accounts.

Thus, the amount needed to be adjusted for uncollectible accounts is $478.

Note:

xA denotes contra asset account

R denotes revenue account

E denotes expenses account

2.

To prepare: Journal entries for items from (a) to (j).

Explanation of Solution

Journal: Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Prepare journal entries for items from (a) to (j) as follows:

| Item | Date | Account Title and Explanation | Debit ($) | Credit ($) |

| a. | January | Accounts Receivable (+A) | 40,000 | |

| Service Revenue (+R) | 40,000 | |||

| (To record service rendered on credit) | ||||

| b. | January 31 | Bad debt expense (+E) | 400 | |

| Allowance for doubtful accounts (+xA) | 400 | |||

| (To record the estimated bad debt expense) | ||||

| c. | February 4 | Cash (+A) | 20,000 | |

| Accounts receivable (–A) | 20,000 | |||

| (To record the collection of cash on account) | ||||

| d. | February 15 | Allowance for doubtful accounts (–xA) | 100 | |

| Accounts receivable (–A) | 100 | |||

| (To record the write off of receivables) | ||||

| e. | February | Accounts Receivable (+A) | 30,000 | |

| Service Revenue (+R) | 30,000 | |||

| (To record service rendered on credit) | ||||

| f. | February 28 | Bad debt expense (+E) | 300 | |

| Allowance for doubtful accounts (+xA) | 300 | |||

| (To record the estimated bad debt expense) | ||||

| g. | March 1 | Note Receivable (+A) | 2,400 | |

| Cash (–A) | 2,400 | |||

| (To recordthe acceptance of note) | ||||

| h. | March 15 | Accounts Receivable (+A) | 100 | |

| Allowance for doubtful accounts (+xA) | 100 | |||

| (To reverse the written off receivables) | ||||

| March 15 | Cash (+A) | 100 | ||

| Accounts receivable (–A) | 100 | |||

| (To record the collection of cash on account) | ||||

| i. | March 31 | Interest Receivable (+A) | 12 | |

| Interest Revenue (+R) | 12 | |||

| (To record accrued interest earned on note) | ||||

| j. | March 31 | Bad debt expense (+E) | 478 | |

| Allowance for doubtful accounts (+xA) | 478 | |||

| (To record the estimated bad debt expense) | ||||

Table (12)

Note:

A denotes asset account, xA denotes contra-asset account, R denotes revenue account, and E denotes expenses account.

3.

To show: How accounts receivable, notes receivable, and their related accounts would be reported in the current asset section of the classified balance sheet at the end of quarter on March 31.

Explanation of Solution

Prepare partial classified balance sheet at the end of quarter on March 31 as follows:

| Incorporation W | ||

| Classified balance sheet (Partial) | ||

| At the end of quarter on March 31 | ||

| Assets: | Amount in $ | Amount in $ |

| Current assets: | ||

| Accounts receivable | 18,000 | |

| Less: Allowance for doubtful accounts | (1,678) | |

| Accounts receivable, net of allowance | 16,322 | |

| Notes receivable | 2,400 | |

| Interest receivable | 12 | |

Table (13)

4.

To identify: Two accounts (apart from sales revenue and service revenue) that are related to accounts receivable and notes receivable that would be reported on the income statement.

Explanation of Solution

Bad debt expense:

Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Bad debt expense account is an account which is related to accounts receivables, which would be reported as bad debt expense on the income statement before income from operations.

Interest revenue account is an account which is related to notes receivables, which would be reported as interest revenue on the income statement after income from operations.

Want to see more full solutions like this?

Chapter 8 Solutions

Fundamentals Of Financial Accounting

- Casebolt Company wrote off the following accounts receivable as uncollectible for the first year of its operations ending December 31: a. Journalize the write-offs under the direct write-off method. b. Journalize the write-offs under the allowance method. Also, journalize the adjusting entry for uncollectible accounts. The company recorded 5,250,000 of credit sales during the year. Based on past history and industry averages, % of credit sales are expected to be uncollectible. c. How much higher (lower) would Casebolt Companys net income have been under the direct write-off method than under the allowance method?arrow_forwardDetermining Bad Debt Expense Using the Aging Method At the beginning of the year, Tennyson Auto Parts had an accounts receivable balance of $31,800 and a balance in the allowance for doubtful accounts of $2,980 (credit). During the year, Tennyson had credit sales of $624,300, collected accounts receivable in the amount of $602,700, wrote off $18,600 of accounts receivable, and had the following data for accounts receivable at the end of the period: Required: 1. Determine the desired post adjustment balance in allowance for doubtful accounts. 2. Determine the balance in allowance for doubtful accounts before the bad debt expense adjusting entry is posted. 3. Compute bad debt expense. 4. Prepare the adjusting entry to record bad debt expense.arrow_forwardAt the end of 20-3, Martel Co. had 410,000 in Accounts Receivable and a credit balance of 300 in Allowance for Doubtful Accounts. Martel has now been in business for three years and wants to base its estimate of uncollectible accounts on its own experience. Assume that Martel Co.s adjusting entry for uncollectible accounts on December 31, 20-2, was a debit to Bad Debt Expense and a credit to Allowance for Doubtful Accounts of 25,000. (a) Estimate Martels uncollectible accounts percentage based on its actual bad debt experience during the past two years. (b) Prepare the adjusting entry on December 31, 20-3, for Martel Co.s uncollectible accounts.arrow_forward

- Tonis Tech Shop has total credit sales for the year of 170,000 and estimates that 3% of its credit sales will be uncollectible. Allowance for Doubtful Accounts has a credit balance of 275. Prepare the adjusting entry at year-end for the estimated bad debt expense. (a) Based on an aging of its accounts receivable, Kyles Cyclery estimates that 3,200 of its year-end accounts receivable will be uncollectible. Allowance for Doubtful Accounts has a debit balance of 280 at year-end. Prepare the adjusting entry at year-end for the estimated uncollectible accounts.arrow_forwardNotes Receivable Transactions The following notes receivable transactions occurred for Harris Company during the last three months of the current year. (Assume all notes are dated the day the transaction occurred.) Required: 1. Prepare the journal entries to record the preceding note transactions and the necessary adjusting entries on December 31. (Assume that Harris does not normally sell its notes and uses a 360-day year for the purpose of computing interest. Round all calculations to the nearest penny.) 2. Show how Harris notes receivable would be disclosed on the December 31 balance sheet. (Assume these are the only note transactions encountered by Harris during the year.)arrow_forwardUNCOLLECTIBLE ACCOUNTSPERCENTAGE OF SALES AND PERCENTAGE OF RECEIVABLES At the completion of the current fiscal year ending December 31, the balance of Accounts Receivable for Yangs Gift Shop was 30,000. Credit sales for the year were 355,200. REQUIRED Make the necessary adjusting entry in general journal form under each of the following assumptions. Show calculations for the amount of each adjustment and the resulting net realizable value. 1. Allowance for Doubtful Accounts has a credit balance of 330. (a) The percentage of sales method is used and bad debt expense is estimated to be 2% of credit sales. (b) The percentage of receivables method is used and an analysis of the accounts produces an estimate of 6,950 in uncollectible accounts. 2. Allowance for Doubtful Accounts has a debit balance of 400. (a) The percentage of sales method is used and bad debt expense is estimated to be 1.5% of credit sales. (b) The percentage of receivables method is used and an analysis of the accounts produces an estimate of 5,685 in uncollectible accounts.arrow_forward

- Allowance Method for Accounting for Bad Debts At the beginning of 2016, Miyazaki Companys Accounts Receivable balance was $105,000, and the balance in Allowance for Doubtful Accounts was $1,950. Miyazakis sales in 2016 were $787,500, 80% of which were on credit. Collections on account during the year were $502,500. The company wrote off $3,000 of uncollectible accounts during the year. Required Prepare summary journal entries related to the sales, collections, and write-offs of accounts receivable during 2016. Prepare journal entries to recognize bad debts assuming that (a) bad debts expense is 3% of credit sales and (b) amounts expected to be uncollectible are 6% of the year-end accounts receivable. What is the net realizable value of accounts receivable on December 31, 2016, under each assumption in part (2)? What effect does the recognition of bad debts expense have on the net realizable value? What effect does the write-off of accounts have on the net realizable value?arrow_forwardAllowance Method for Accounting for Bad Debts At the beginning of 2016, EZ Tech Companys Accounts Receivable balance was $140,000, and the balance in Allowance for Doubtful Accounts was $2,350 (Cr.). EZ Techs sales in 2016 were $1,050,000, 80% of which were on credit. Collections on account during the year were $670,000. The company wrote off $4,000 of uncollectible accounts during the year. Required Prepare summary journal entries related to the sale, collections, and write-offs of accounts receivable during 2016. Prepare journal entries to recognize bad debts assuming that (a) bad debts expense is 3% of credit sales and (b) amounts expected to be uncollectible are 6% of the year-end accounts receivable. What is the net realizable value of accounts receivable on December 31, 2016, under each assumption in part (2)? What effect does the recognition of bad debts expense have on the net realizable value? What effect does the write-off of accounts have on the net realizable value?arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning