Videos

Gross Profit

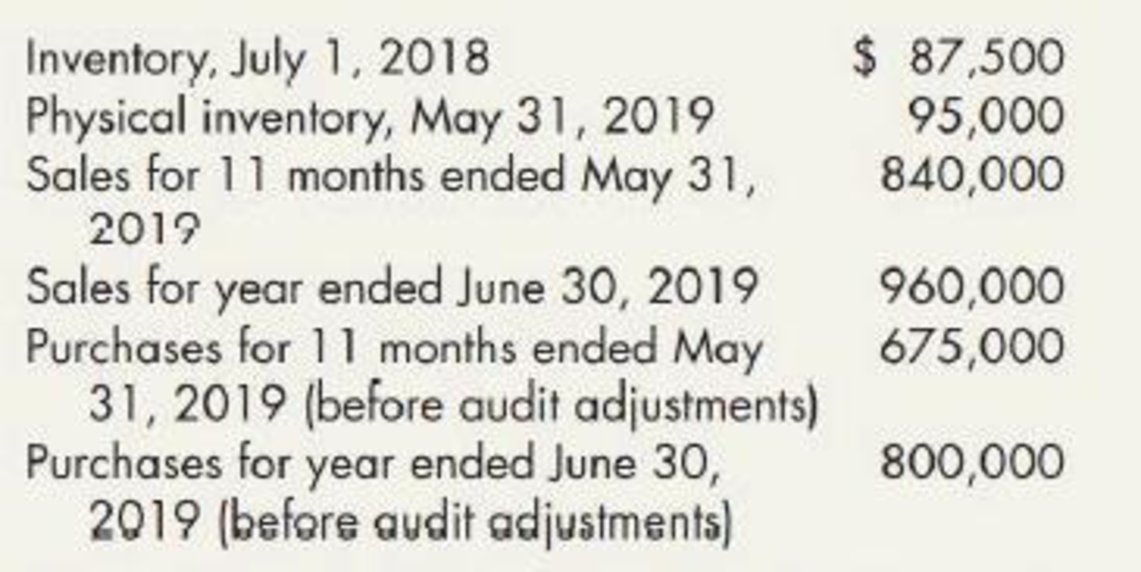

Shelly Corporation is an importer and wholesaler. Its merchandise is purchased from several suppliers and is warehoused by Shelly until sold to consumers. In conducting her audit for the year ended June 30, 2019, the corporation’s CPA determined that the system of internal control was good. Accordingly, she observed the physical inventory at an interim date, May 31, 2019, instead of at year-end.

The CPA obtained the following information from the general ledger:

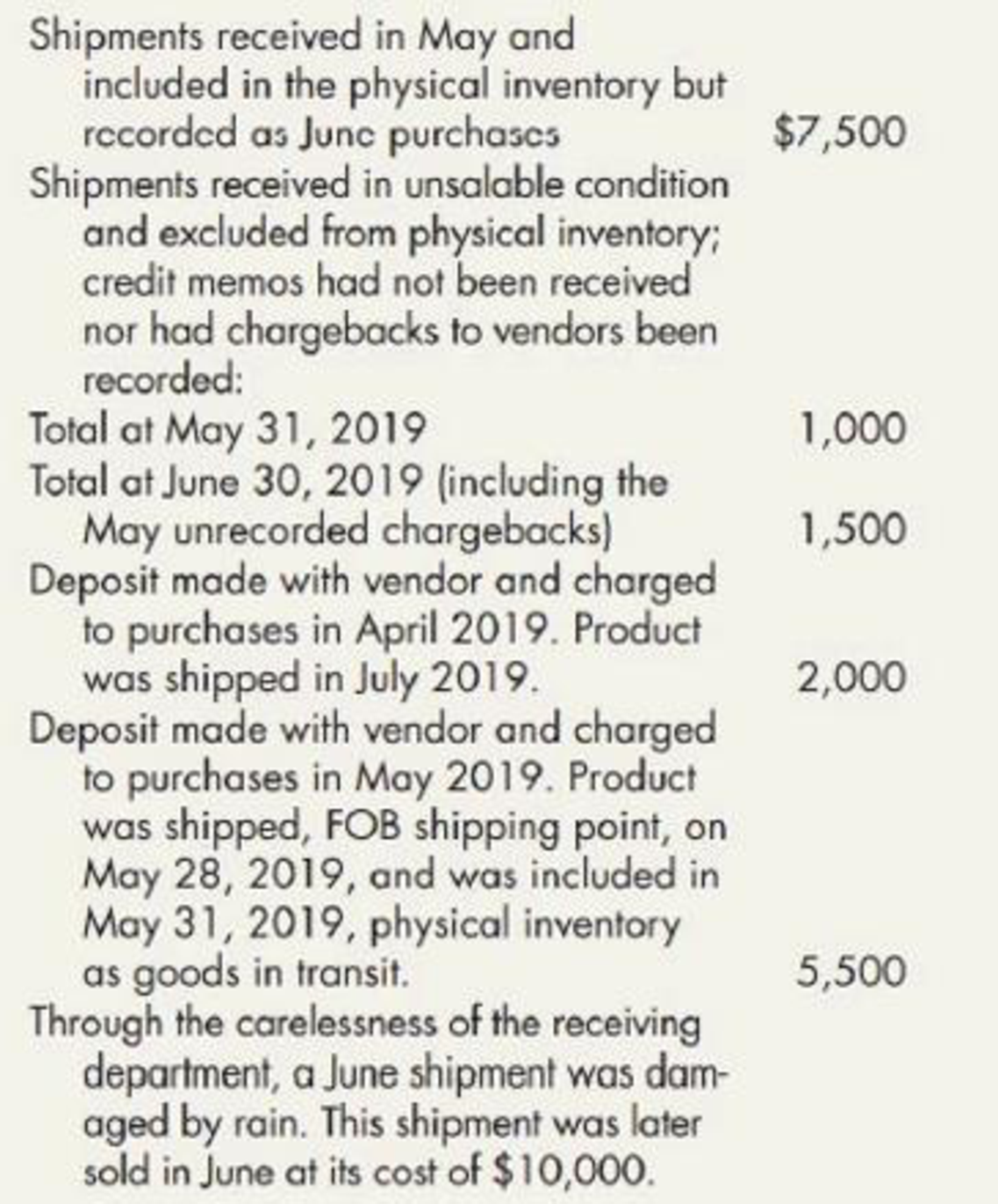

The CPA’s audit disclosed the following information:

Required:

In audit engagements in which interim physical inventories are observed, a frequently used

- 1. Computation of the gross profit ratio for 11 months ended May 31, 2019

- 2. Computation by the gross profit ratio method of cost of goods sold during June 2019

- 3. Computation by the gross profit ratio method of June 30, 2019 inventory

Trending nowThis is a popular solution!

Chapter 8 Solutions

Intermediate Accounting: Reporting And Analysis

- Inventory Valuation You are engaged in an audit of Roche Mfg. Company for the year ended December 31, 2019. To reduce the workload at year-end, Roche took its annual physical inventory under your observation on November 30, 2019. Roches inventory account, which includes raw materials and work in process, is on a perpetual basis, and it uses the first-in, first-out method of pricing. It has no finished goods inventory. The companys physical inventory revealed that the book inventory of 60,570 was understated by 3,000. To avoid distorting the interim financial statements, Roche decided not to adjust the book inventory until year-end except for obsolete inventory items. Your audit revealed this information about the November 30 inventory: Pricing tests showed that the physical inventory was overpriced by 2,200. Footing and extension errors resulted in a 150 understatement of the physical inventory. Direct labor included in the physical inventory amounted to 10,000. Overhead was included at the rate of 200% of direct labor. You determined that the amount of direct labor was correct and the overhead rate was proper. The physical inventory included obsolete materials recorded at 250. During December, these materials were removed from the inventory account by a charge to cost of sales. Your audit also disclosed the following information about the December 31, 2019, inventory. Total debits to certain accounts during December are: The cost of sales of 68,600 included direct labor of 13,800. Normal scrap loss on established product lines is negligible. However, a special order started and completed during December had excessive scrap loss of 800 which was charged to Manufacturing Overhead Expense. Required: 1. Compute the correct amount of the physical inventory at November 30, 2019. 2. Without prejudice to your solution to Requirement 1, assume that the correct amount of the inventory at November 30, 2019, was 57,700. Compute the amount of the inventory at December 31,2019.arrow_forwardConsider each of the following independent situations. Should a company report the goods in its inventory? (a) Goods purchased by the company with shipping terms FOB shipping point that are in transit at the end of the year (b) Goods received by the company on consignment (c) An estimate of the amount of goods sold by the company that it expects the buyer to return (d) Goods required to be purchased by the company under an unconditional purchase obligationarrow_forwardErrors As controller of Lerner Company, which uses a periodic inventory system, you discover the following errors in the current year: 1. Merchandise with a cost of 17,500 was properly included in the final inventory, but the purchase was not recorded until the following year. 2. Merchandise purchases are in transit under terms of FOB shipping point. They have been excluded from the inventory, but the purchase was recorded in the current year on the receipt of the invoice of 4,300. 3. Goods out on consignment have been excluded from inventory. 4. Merchandise purchases under terms FOB shipping point have been omitted from the purchases account and the ending inventory. The purchases were recorded in the following year. 5. Goods held on consignment from Talbert Supply Co. were included in the inventory. Required: For each error, indicate the effect on the ending inventory and the net income for the current year and on the net income for the following year.arrow_forward

- The following data were extracted from the accounting records of Harkins Company for the year ended April 30, 2019: a. Prepare the cost of merchandise sold section of the income statement for the year ended April 30, 2019, using the periodic inventory system. b. Determine the gross profit to be reported on the income statement for the year ended April 30, 2019. c. Would gross profit be different if the perpetual inventory system was used instead of the periodic inventory system?arrow_forwardUnder the periodic inventory system, what account is debited when an estimate is made for sales made this year, but expected to be returned next year? (a) Sales Returns and Allowances (b) Merchandise Inventory (c) Customer Refunds Payable (d) Salesarrow_forwardGrimstad Company uses FIFO for internal reporting purposes and LIFO for financial reporting and income tax purposes. At the end of 2019, the following information was obtained from the inventory records: Required: 1. Prepare the necessary adjusting journal entry assuming that Grimstad converts the accounts to LIFO at the end of 2019. 2. Indicate how Grimstad would disclose the inventory value on its comparative balance sheets prepared at the end of 2019. 3. Next Level By how much would Grimstads cost of goods sold differ in 2019 if it used FIFO for external reporting?arrow_forward

- Under the periodic inventory system, what account is credited when an estimate is made for sales made this year, but expected to be returned next year? (a) Merchandise Inventory (b) Customer Refunds Payable (c) Sales (d) Sales Returns and Allowancesarrow_forwardPalisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardKoopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Koopman had cash of 10,000, inventory of 24,000, other assets of 70,800, accounts payable of 4,500, and income taxes payable of 6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forward

- Selected data on merchandise inventory, purchases, and sales for Jaffe Co. and Coronado Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Jaffe Co. on February 28 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Coronado Co. on October 31 by the gross profit method, presenting details of the computations. b. Assume that Coronado Co. took a physical inventory on October 31 and discovered that 366,500 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during May through October?arrow_forwardSelected data on merchandise inventory, purchases, and sales for Celebrity Tan Co. and Ranchworks Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Celebrity Tan Co. on August 31 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Ranchworks Co. on November 30 by the gross profit method, presenting details of the computations. b. Assume that Ranchworks Co. took a physical inventory on November 30 and discovered that 369,750 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during March through November?arrow_forwardUnder the periodic inventory system, what account is debited when an estimate is made for the cost of merchandise inventory sold this year, but expected to be returned next year? (a) Estimated Returns Inventory (b) Sales Returns and Allowances (c) Merchandise Inventory (d) Customer Refunds Payablearrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning  Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning